HELOC vs. Credit Card: Cost Comparison

At first glance, comparing a HELOC to a credit card seems almost unfair. One is a mortgage product requiring a home, equity, an appraisal, and weeks of underwriting. The other is a piece of plastic you can use in five seconds at any checkout counter.

But the comparison matters — and it matters a lot — because millions of American homeowners routinely use credit cards to fund expenses that a HELOC could handle at a fraction of the cost. Home improvements charged to a rewards card. Emergency expenses put on a high-interest card because it was convenient. Renovation costs that ballooned beyond what savings could cover.

This article gives you a clear, honest cost comparison between HELOCs and credit cards — with real numbers that show exactly what the convenience of a credit card costs you relative to the structured, lower-cost borrowing of a HELOC.

The Fundamental Difference

A HELOC is secured debt backed by your home. Because the lender has collateral, they charge a lower interest rate. You go through an underwriting process, your home is appraised, and you receive a credit line at a rate typically between 7.75% and 10.50% in 2026.

A credit card is unsecured revolving debt with no collateral. The lender has no claim on any asset if you default, so they price that risk into the interest rate — which is why credit card APRs average 21% to 28% in 2026 for most cardholders and can exceed 30% for those with less-than-perfect credit.

The difference in rates is not marginal. It is the difference between borrowing at roughly 9% and borrowing at roughly 24%. That gap compounds aggressively over time and produces dramatically different outcomes for the same amount of spending.

Interest Rates: The Core of the Comparison

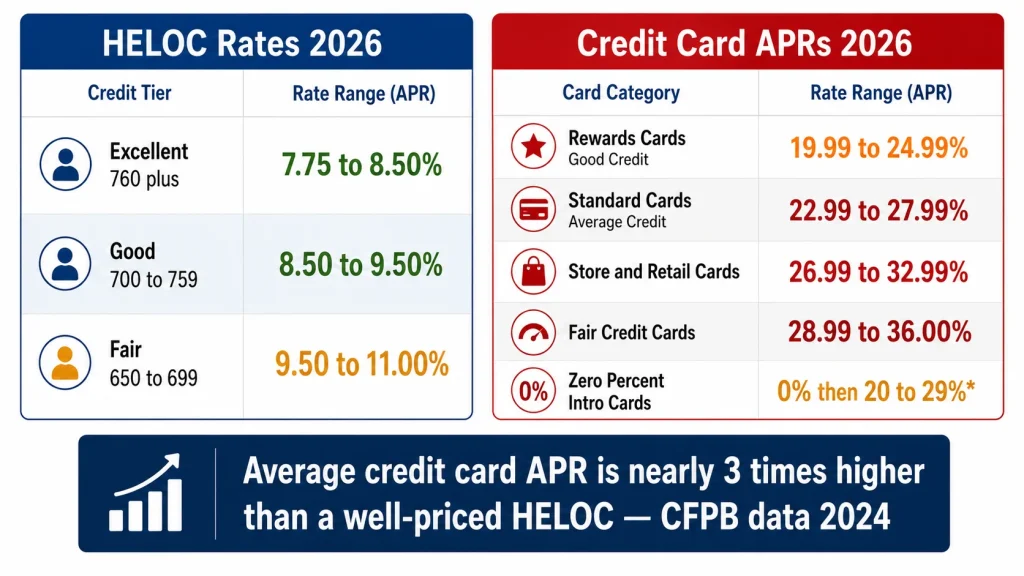

HELOC Rates in 2026

| Credit Profile | Typical HELOC Rate |

|---|---|

| Excellent (760+) | 7.75% – 8.50% |

| Good (700–759) | 8.50% – 9.50% |

| Fair (650–699) | 9.50% – 11.00% |

Credit Card APRs in 2026

| Card Type | Typical APR Range |

|---|---|

| Rewards cards (good credit) | 19.99% – 24.99% |

| Standard cards (average credit) | 22.99% – 27.99% |

| Store and retail cards | 26.99% – 32.99% |

| Cards for fair/building credit | 28.99% – 36.00% |

| 0% introductory APR cards | 0% for 12–21 months, then 20%–29% |

The average credit card APR in the United States crossed 21% in 2023 and has remained elevated. According to the Consumer Financial Protection Bureau (CFPB), the average APR charged on accounts that assessed interest was 22.77% as of late 2024 — nearly three times the rate of a well-priced HELOC.

The Real Cost: Side-by-Side Dollar Comparisons

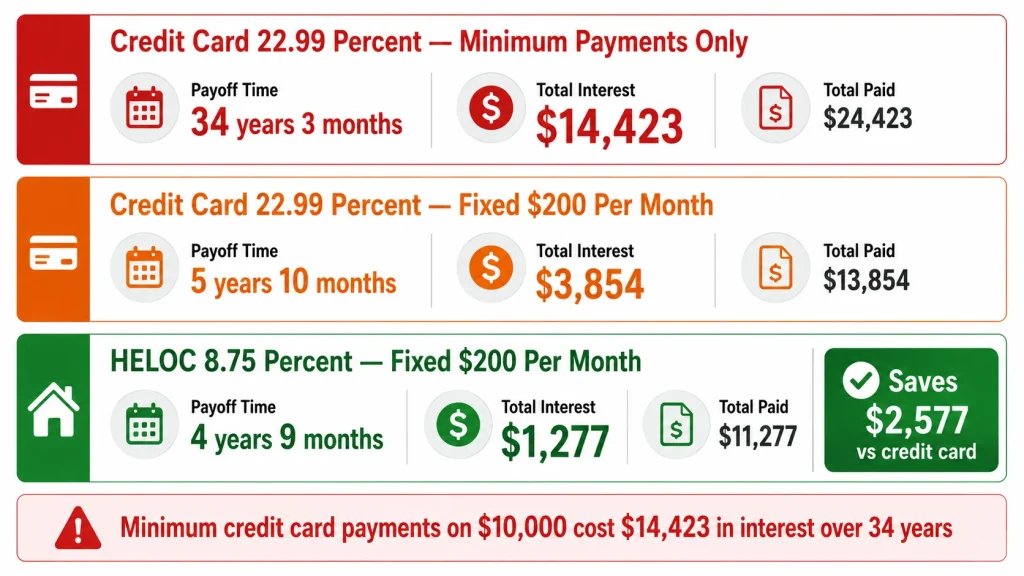

Scenario 1: $10,000 Balance

Credit Card at 22.99% — Minimum Payments Only

| Amount | |

|---|---|

| Time to pay off | 34 years 3 months |

| Total interest paid | $14,423 |

| Total paid | $24,423 |

Credit Card at 22.99% — Fixed $200/Month

| Amount | |

|---|---|

| Time to pay off | 5 years 10 months |

| Total interest paid | $3,854 |

| Total paid | $13,854 |

HELOC at 8.75% — Fixed $200/Month

| Amount | |

|---|---|

| Time to pay off | 4 years 9 months |

| Total interest paid | $1,277 |

| Total paid | $11,277 |

The $200/month comparison at $10,000:

| Product | Monthly Payment | Payoff Time | Total Interest | Total Paid |

|---|---|---|---|---|

| Credit card minimum | ~$200 declining | 34+ years | $14,423 | $24,423 |

| Credit card $200/month | $200 fixed | 5 yrs 10 mos | $3,854 | $13,854 |

| HELOC $200/month | $200 fixed | 4 yrs 9 mos | $1,277 | $11,277 |

At a fixed $200/month, a HELOC saves $2,577 in interest versus the credit card on just $10,000.

Scenario 2: $25,000 Balance

Credit Card at 22.99% — Fixed $400/Month

| Amount | |

|---|---|

| Time to pay off | 8 years 5 months |

| Total interest paid | $15,313 |

| Total paid | $40,313 |

HELOC at 8.75% — Fixed $400/Month

| Amount | |

|---|---|

| Time to pay off | 6 years 6 months |

| Total interest paid | $6,177 |

| Total paid | $31,177 |

Interest saved with HELOC: $9,136

Scenario 3: $50,000 Balance

Credit Card at 22.99% — Fixed $800/Month

| Amount | |

|---|---|

| Time to pay off | 9 years 2 months |

| Total interest paid | $38,267 |

| Total paid | $88,267 |

HELOC at 8.75% — Fixed $800/Month

| Amount | |

|---|---|

| Time to pay off | 6 years 10 months |

| Total interest paid | $15,621 |

| Total paid | $65,621 |

Interest saved with HELOC: $22,646

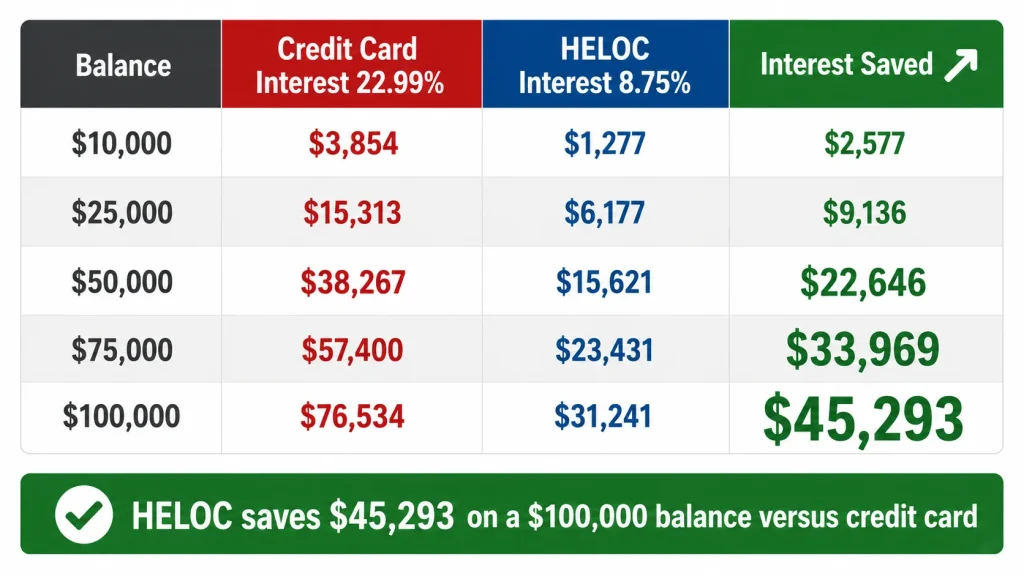

Full Comparison Summary

| Balance | Credit Card Interest (22.99%) | HELOC Interest (8.75%) | Interest Saved |

|---|---|---|---|

| $10,000 | $3,854 | $1,277 | $2,577 |

| $25,000 | $15,313 | $6,177 | $9,136 |

| $50,000 | $38,267 | $15,621 | $22,646 |

| $75,000 | $57,400 | $23,431 | $33,969 |

| $100,000 | $76,534 | $31,241 | $45,293 |

Use our HELOC Payment Calculator to model your specific balance and see your exact HELOC payment and total interest cost.

Using a HELOC to Pay Off Credit Card Debt

One of the most financially impactful uses of a HELOC is consolidating existing high-interest credit card debt into a lower-rate HELOC balance.

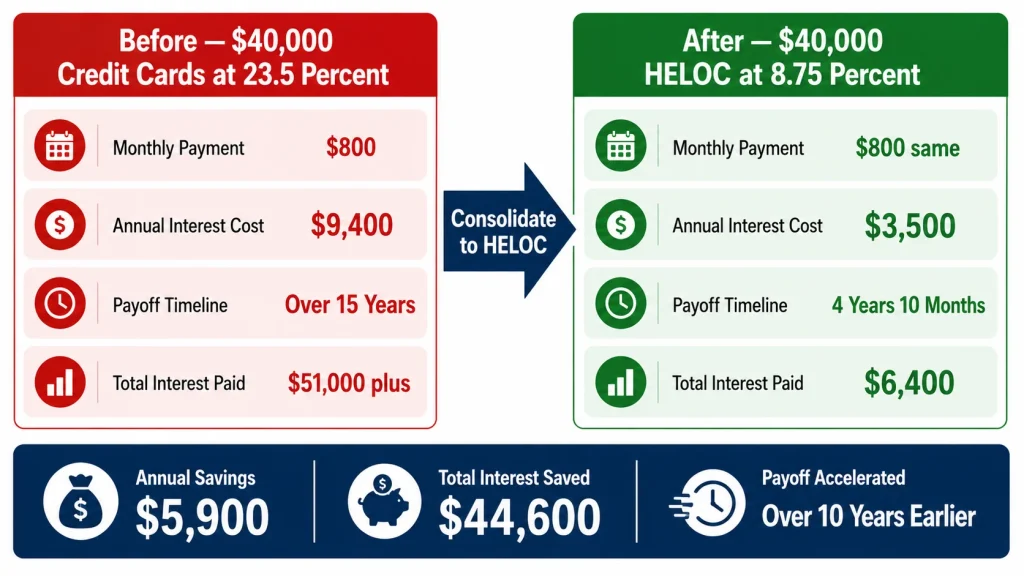

Here is what the math looks like for a homeowner carrying $40,000 in credit card debt at an average 23.5% APR:

Current situation — $40,000 on credit cards at 23.5%:

- Minimum monthly payment: approximately $800

- Annual interest cost: $9,400

- Time to pay off at $800/month: Over 15 years

- Total interest paid: $51,000+

After consolidating to a HELOC at 8.75%:

- Monthly payment at $800/month: Same $800

- Annual interest cost: $3,500

- Time to pay off at $800/month: 4 years 10 months

- Total interest paid: $6,400

Annual interest savings: $5,900 Total interest savings: $44,600 Payoff accelerated by: Over 10 years

The same $800/month payment eliminates the debt in under 5 years on a HELOC versus 15+ years on credit cards.

The Critical Warning: Secured vs. Unsecured Debt

Before reaching for a HELOC to pay off credit cards, one risk deserves full honest attention.

Credit card debt is unsecured. If you fail to pay, the issuer damages your credit and can pursue legal action — but cannot take your home.

HELOC debt is secured by your home. If you fail to pay, your lender can foreclose.

When you consolidate credit card debt into a HELOC, you are converting unsecured debt into debt that puts your home at risk. For financially disciplined borrowers with stable income, this is a sound trade. For borrowers whose credit card debt reflects chronic overspending, this conversion is dangerous.

The most common failure pattern: homeowner consolidates $40,000 in credit card debt into HELOC, feels relief, then gradually runs the credit cards back up — now carrying both the HELOC balance and the new credit card balance. This is a documented behavioral pattern financial counselors see regularly.

Before consolidating, ask yourself honestly:

- What caused the credit card debt in the first place?

- Has that underlying issue been resolved?

- Can I commit to not using those cards for non-emergency spending after consolidation?

The 0% Introductory APR Card: A Genuine Alternative for Short-Term Needs

One scenario where a credit card legitimately beats a HELOC: 0% introductory APR cards.

Many major issuers — including Chase, Citi, Bank of America, and Discover — offer 0% APR for 12 to 21 months on purchases or balance transfers. If you can pay off the balance within the promotional period, you borrow at zero cost.

Example: $8,000 for a bathroom renovation, paid off in 15 months.

- 0% APR card: Total interest = $0

- HELOC at 8.75%: Total interest over 15 months = $490

The 0% card wins — but only if you pay off the full balance before the promotional period expires. One missed payoff converts the full remaining balance to the regular APR of 20%–29% instantly.

The 0% card makes sense when:

- The amount is under $10,000–$15,000

- You have a specific funding source to pay it off within the promo window

- You are disciplined enough to actually pay it off in time

Rewards Points: Are They Worth the Higher Rate?

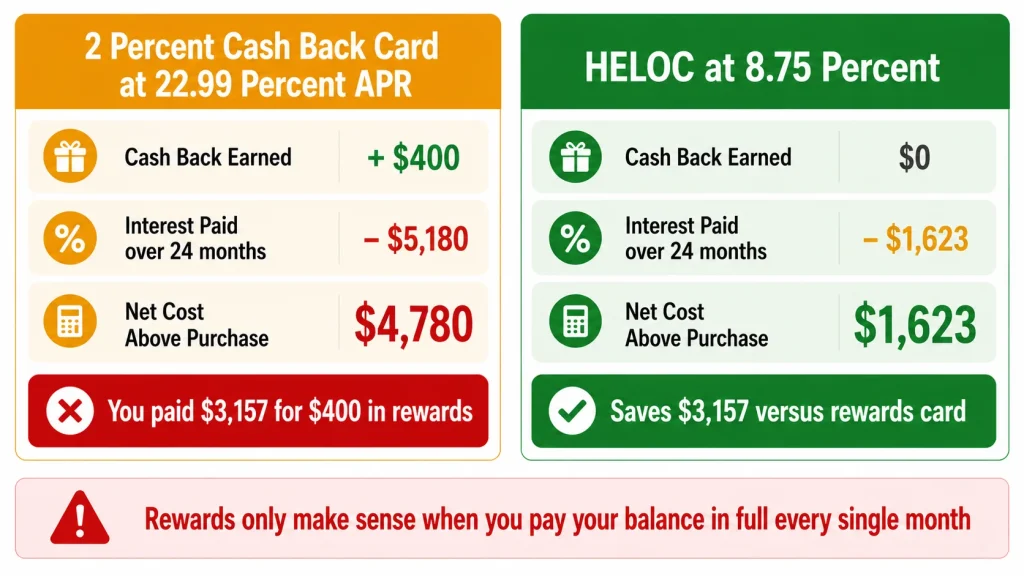

A common rationalization for using a credit card over a HELOC: “I get 2% cash back — it is basically free money.”

The honest math on a $20,000 renovation charged to a 2% cash back card at 22.99%, paid off over 24 months vs. HELOC at 8.75%:

Credit card with 2% cash back:

- Cash back earned: $400

- Interest paid over 24 months: $5,180

- Net cost above purchase: $4,780

HELOC at 8.75%:

- Cash back earned: $0

- Interest paid over 24 months: $1,623

- Net cost above purchase: $1,623

The 2% cash back card costs $3,157 more than the HELOC — even after the $400 in rewards. You paid $3,157 for $400 in rewards. That is a deeply negative return.

Rewards only make financial sense when you pay your balance in full every month. The moment you carry a balance, any rewards card becomes one of the most expensive forms of credit available.

When Credit Cards Still Make Sense Over a HELOC

Despite the cost difference, there are specific situations where using a credit card is the right call.

Purchases under $1,000–$2,000 paid off next month. For routine purchases paid in full monthly, a rewards card costs nothing in interest and earns rewards. No role for a HELOC here.

Emergency expenses when HELOC transfer takes 1–2 days. Credit cards provide instant purchasing power for genuine emergencies.

Purchases with buyer protections. Credit cards offer fraud protection, purchase protection, extended warranties, and dispute resolution rights that HELOCs do not. For significant purchases where these protections matter — electronics, appliances, contractors — the card is genuinely valuable when paid off immediately.

Travel and specific category rewards paid in full. Travel cards, hotel cards, and airline cards provide genuine value for expenses paid in full every cycle.

When you do not have a HELOC and need money immediately. Use the card to bridge the gap, then open a HELOC and pay off the card balance.

The Discipline Factor: HELOC vs. Credit Card Psychology

A credit card makes spending frictionless. Tap, swipe, done. This low friction is by design — issuers profit from impulse spending.

A HELOC introduces meaningful friction for new draws. Log in, initiate a transfer, wait 1–2 business days. For large planned expenses, this friction is irrelevant. For impulsive spending, it is a genuine guardrail.

For borrowers who have struggled with credit card overspending, a HELOC’s slower access to funds is a practical behavioral advantage — not just a financial one.

Side-by-Side Comparison Summary

| Factor | HELOC | Credit Card |

|---|---|---|

| Typical interest rate 2026 | 8.25% – 10.50% | 19.99% – 32.99% |

| Secured or unsecured | Secured — home as collateral | Unsecured |

| Home ownership required | Yes — with equity | No |

| Approval timeline | 3–6 weeks | Minutes to days |

| Interest on $25,000 balance | ~$6,177 | ~$15,313 |

| Tax deductible interest | Potentially | Never |

| Rewards or cash back | No | Yes — only valuable if paid in full |

| Buyer protections | No | Yes |

| Home foreclosure risk | Yes | No |

| Best for | Large planned expenses | Small purchases paid monthly |

The Bottom Line

The cost difference between a HELOC and a credit card is enormous. For any balance carried longer than one billing cycle, credit card rates of 20%–30% make them among the most expensive forms of credit available. A HELOC at 8.75% on the same balance costs less than half as much in interest and can save tens of thousands of dollars on large balances.

The right framework:

Use credit cards for: Purchases under $1,000–$2,000 paid in full every month, purchases requiring buyer protections, and 0% promo periods where you can guarantee payoff before the rate resets.

Use a HELOC for: Any significant expense that will carry a balance for more than one month, particularly amounts above $5,000, and for consolidating existing high-interest credit card debt.

The single biggest financial mistake homeowners with available HELOC equity make is funding large renovations or carrying high-interest credit card debt when a HELOC could cut their interest cost by 60% to 75%.

Use our HELOC Payment Calculator to see exactly what your expense would cost on a HELOC — then compare it to the interest you are currently paying on your credit card balance.