HELOC for Emergency Fund: Smart or Risky?

The idea sounds appealing on paper. Why park $25,000 in a savings account earning 4.5% when you could keep that money invested — earning potentially higher returns — and use your HELOC as a backup for emergencies instead?

It is a strategy financial writers discuss, some advisors recommend, and plenty of homeowners have quietly adopted. And it has genuine merit — under the right conditions.

It also has real, specific risks that the people recommending it often gloss over. A HELOC is not a savings account. It is debt you activate against your home. The moment you draw it, the interest clock starts, your home is collateral, and your financial position has changed in ways that a cash emergency fund simply does not produce.

This article gives you the complete, honest picture — what the strategy gets right, what it gets dangerously wrong, and how to think about it for your specific financial situation.

What the Strategy Actually Is

The HELOC-as-emergency-fund strategy works like this: instead of maintaining a traditional cash emergency fund of 3 to 6 months of living expenses in a savings account, you keep a HELOC open with a zero balance — or a low balance — and treat the available credit as your emergency reserve.

If a true emergency hits — job loss, major medical expense, urgent home repair — you draw from the HELOC to cover it rather than from cash savings. In the meantime, the money that would have sat in a savings account is deployed elsewhere — invested in the stock market, used to pay down other debt, or kept for specific planned expenses.

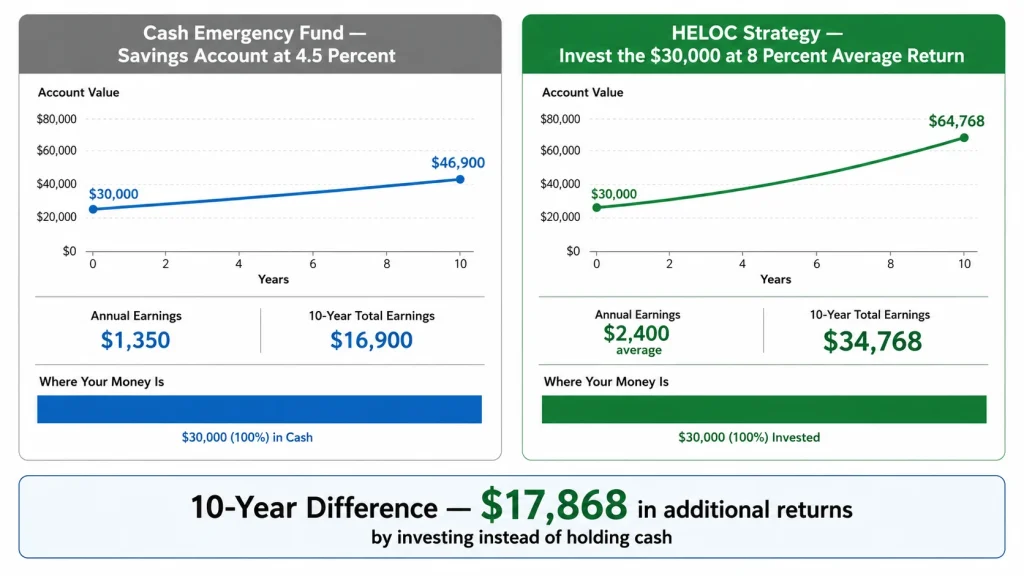

The appeal is real. A $30,000 emergency fund sitting in a high-yield savings account at 4.5% earns $1,350/year. That same $30,000 invested in a diversified index fund has historically averaged 7–10% annual returns — a $2,100 to $3,000 annual difference, before taxes.

Over 10 years, the difference between holding cash and investing that cash compounds significantly. Proponents argue that a HELOC gives you emergency liquidity without sacrificing investment returns — having it both ways.

What the Strategy Gets Right

Before examining the risks, the genuine strengths of this approach deserve honest acknowledgment.

A Zero-Balance HELOC Costs Almost Nothing to Maintain

An open HELOC with no balance typically costs $0 to $100 per year in annual fees — sometimes nothing at all. You are paying for optionality. The credit line exists, available immediately if needed, at essentially no carrying cost until you actually draw from it.

Compare this to the opportunity cost of holding 3–6 months of expenses in cash. At current savings rates and with a $30,000 emergency fund, you are choosing a near-certain 4.5% return over a potentially higher return from investing. The HELOC strategy attempts to capture the difference.

A HELOC Can Cover Larger Emergencies Than Most Cash Funds

A $30,000 cash emergency fund handles most emergencies. But a $150,000 HELOC credit line handles almost any emergency — a catastrophic medical bill, a major structural home repair, a sudden business crisis. The sheer size of available credit from a large HELOC can provide a level of financial security that even a well-funded cash emergency fund cannot match.

A HELOC Has Immediate Draw Capability

HELOC funds are typically available within 1 to 2 business days of initiating a draw — sometimes same-day depending on your bank and account setup. For most emergencies, this is fast enough. The lag is not practically different from liquidating investments or wiring money from a brokerage account.

For Disciplined Investors, the Math Can Work

If you have strong investment discipline, a stable job, high income relative to your monthly expenses, and a genuine ability to repay a HELOC draw quickly if needed — the strategy can produce real financial benefit over time. The numbers are not wrong; the question is whether the assumptions behind them hold in your specific situation.

What the Strategy Gets Wrong: The Real Risks

Here is where the honest analysis diverges from the optimistic version of this strategy.

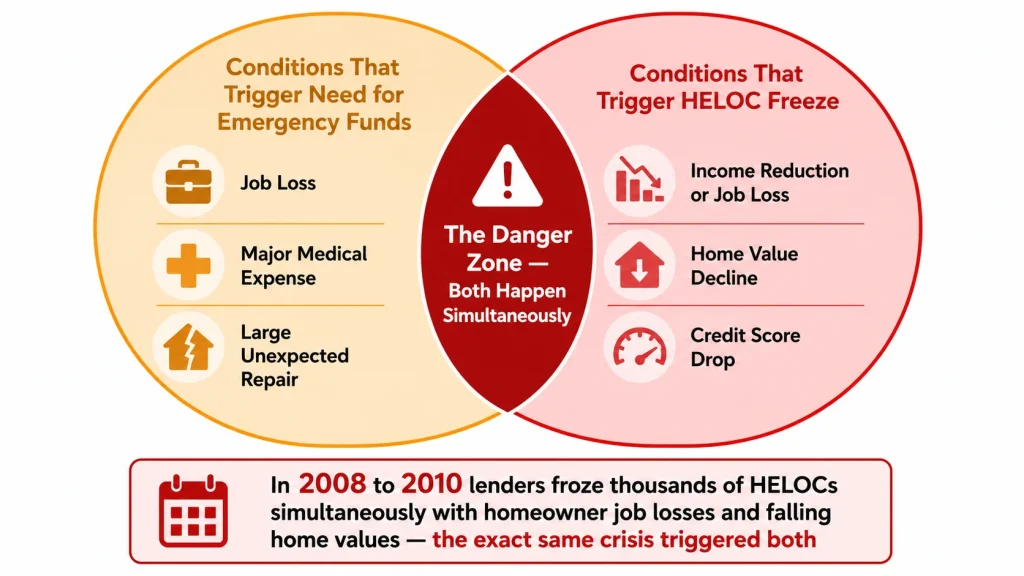

Risk 1: Emergencies and Financial Crises Often Arrive Together

The most dangerous flaw in the HELOC-as-emergency-fund logic is an assumption about timing: that emergencies happen in isolation and that your financial situation is otherwise stable when they do.

In reality, the biggest emergencies tend to cluster with financial stress. Job loss — one of the most common emergency fund scenarios — typically reduces or eliminates income precisely when you need to draw on reserves. And that is exactly when a lender can freeze or reduce your HELOC.

Lenders have the legal right to freeze, reduce, or cancel a HELOC credit line if:

- Your home’s value declines significantly

- Your credit score drops materially

- Your income situation changes (job loss, income reduction)

- The lender experiences liquidity problems of their own

This happened on a massive scale during 2008–2010. Homeowners who had planned to use their HELOCs as emergency backup found the credit lines frozen or canceled just when they needed them most — simultaneously with job losses, falling home values, and tightening credit conditions.

A lender can freeze a $150,000 HELOC and reduce it to zero available credit with 45 days notice. Your cash savings account cannot be frozen by anyone but you.

Risk 2: Emergencies Convert to Secured Debt

Every dollar you draw from a HELOC in an emergency becomes secured debt against your home. You have not just borrowed money — you have pledged your home as collateral for the emergency expense.

If the emergency was a job loss and the drawn balance cannot be repaid quickly, you are now carrying home-secured debt with a monthly interest obligation during the period when your income is lowest. The minimum payment on a $30,000 HELOC draw at 8.75% is $219/month — a manageable number if you have income, but a real additional burden if you are already income-stressed.

A cash emergency fund draws from your own assets with no ongoing obligation and no collateral risk. A HELOC draw creates a new obligation secured by your home.

Risk 3: The HELOC May Not Be There When You Need It

This is not just a historical risk from 2008. In 2026, several conditions can still trigger HELOC freezes or reductions:

Declining home value: If real estate prices in your area fall 15–20%, bringing your home’s value closer to your combined mortgage and HELOC balance, lenders can reduce your available credit to maintain their LTV requirements.

Credit score decline: A job loss itself can trigger credit score drops if you miss any payments during a stressful period. A lower credit score gives lenders grounds to reduce the line.

Lender financial health: During the 2023 regional banking stress, several lenders temporarily tightened HELOC availability. This can happen again.

The fundamental problem: the conditions that most commonly trigger the need for an emergency fund are the same conditions that make a HELOC less reliable.

Risk 4: Variable Rate Risk During an Emergency

A HELOC carries a variable interest rate. If you draw $30,000 during a financial emergency and hold that balance for 18 months while recovering, your interest cost during that period depends on where rates are — which you cannot control.

If the Federal Reserve is raising rates during your recovery period (as occurred aggressively in 2022–2023), your interest cost on the emergency draw rises every quarter. A cash emergency fund’s “cost” does not change regardless of what rates do.

Risk 5: The Behavioral Risk of Easy Credit Access

A HELOC with a large available credit line and easy draw access can blur the line between emergencies and non-emergencies over time. What starts as a disciplined emergency-only reserve can gradually become a line of credit that gets used for semi-emergencies, then for planned expenses, then for things that are simply convenient to pay for with the available credit.

This is not a failure of the strategy — it is a failure of the human implementing it. But financial strategies that require perfect behavioral discipline to work are riskier in practice than their theory suggests.

The Hybrid Approach: HELOC as a Supplement, Not a Replacement

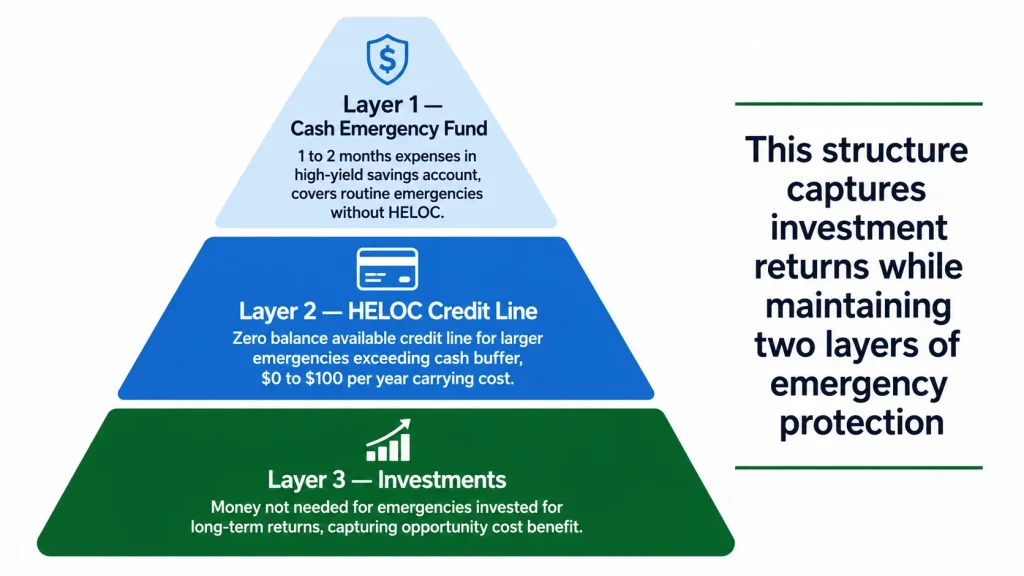

The most financially sound approach for most homeowners is not to choose between a cash emergency fund and a HELOC — it is to use both in a layered system.

Layer 1: Cash emergency fund (1–2 months of expenses) Keep a smaller cash buffer — enough to handle most short-term disruptions — in a high-yield savings account. This covers car repairs, medical copays, appliance replacements, and most common emergencies without touching your HELOC or triggering any debt.

At 4.5% on $10,000, the opportunity cost of this cash buffer is $450/year. That is reasonable insurance against the risks the HELOC carries.

Layer 2: HELOC credit line (zero balance, available for larger emergencies) Your HELOC handles the events that exceed your cash buffer — a major medical crisis, a large home repair, an extended period of reduced income. It is not your first line of defense, but it is available for larger situations.

Layer 3: Investments (for long-term wealth building) The money you do not need to hold in a larger cash emergency fund gets invested for long-term returns. You capture most of the investment opportunity cost benefit of the HELOC strategy while retaining the security of a cash buffer for routine emergencies.

This layered structure gives you the benefits of both approaches while limiting the specific risks of relying entirely on a HELOC.

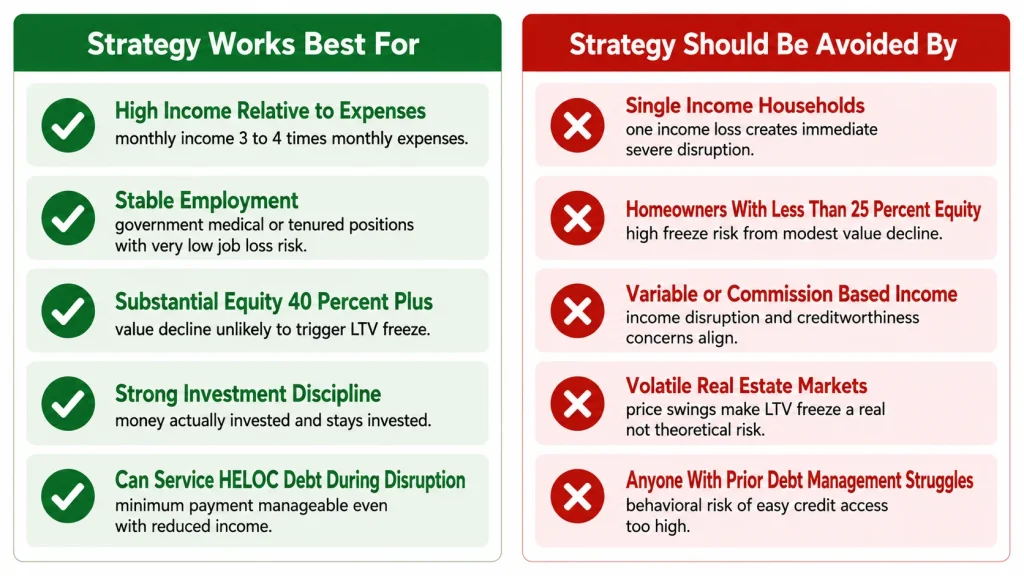

Who This Strategy Works Best For

If you are going to use a HELOC as part of your emergency planning — either as a supplement or as a primary emergency reserve — here is the profile where it works most reliably.

High income relative to expenses. If your monthly income is 3 to 4 times your monthly expenses, a financial disruption is less likely to create a multi-month crisis. You can repay a HELOC draw from normal income relatively quickly after an emergency resolves.

Job stability. Government employees, tenured professors, medical professionals in stable practices, and others with very low job loss risk face less correlation between “need emergency funds” and “HELOC gets frozen due to income loss.” The more stable your employment, the more reliable this strategy becomes.

Significant equity cushion. If your home has 40%+ equity, a meaningful property value decline would not trigger an LTV-based credit freeze. A homeowner with 85% CLTV is much more vulnerable to a freeze than one with 60% CLTV.

Strong investment discipline. The strategy only produces the promised benefit if the money that would have been in a cash emergency fund is actually invested — and stays invested through market volatility without being spent on non-emergencies.

Ability to service HELOC debt during income disruption. If you drew $25,000 from your HELOC during an emergency and lost your job simultaneously, could you still make the minimum HELOC payment ($182/month at 8.75%) without significant stress? If yes, the strategy is viable. If no, the risk is real.

Who Should NOT Use This Strategy

Single-income households. If one person’s income supports the entire household and that income disappears suddenly, the financial disruption is immediate and severe. A cash emergency fund is far safer than a potentially-frozen HELOC in this scenario.

Homeowners with less than 25% equity. The freeze risk from declining home values is meaningfully higher for homeowners with thin equity positions. A 15% home value decline could bring a 20% equity position to 5%, triggering an LTV-based freeze.

Variable or commission-based income earners. Income disruption risk is higher, and that same income variability can trigger lender concerns about creditworthiness — increasing the freeze risk precisely when you need the line.

Homeowners in volatile real estate markets. If your local market has shown significant price swings in recent cycles, the home value freeze trigger is a real risk, not a theoretical one.

Anyone who has struggled with debt management. The behavioral risk of easy credit access is highest for borrowers who have previously accumulated consumer debt. A HELOC is not a savings account — treating it as one requires the discipline to use it only for genuine emergencies.

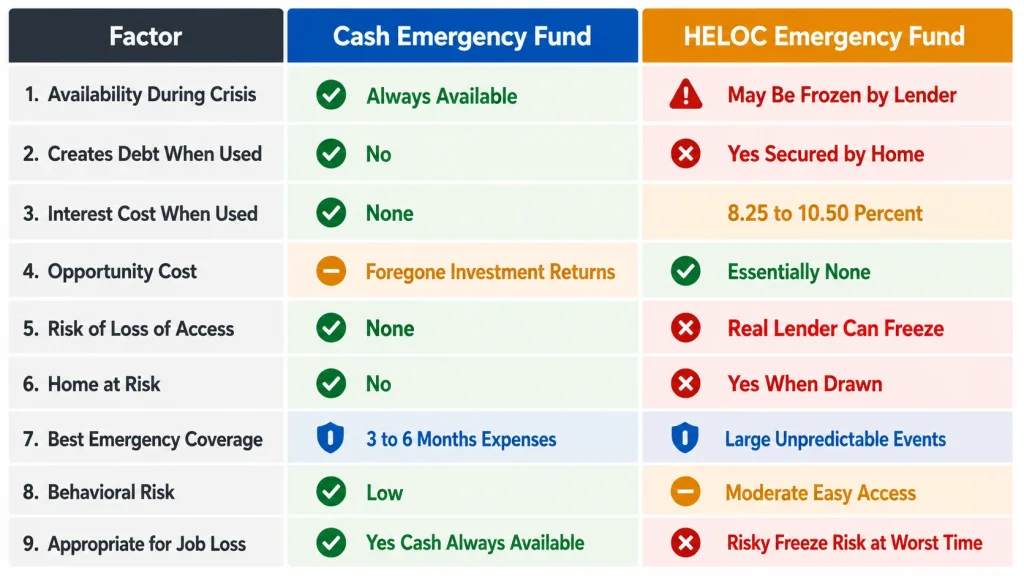

Comparing the Two Approaches: Full Cost and Risk Analysis

| Factor | Cash Emergency Fund | HELOC Emergency Fund |

|---|---|---|

| Availability during crisis | Always available | May be frozen by lender |

| Creates debt when used | No — draws from your assets | Yes — secured debt against home |

| Interest cost when used | None | 8.25%–10.50% variable |

| Opportunity cost | Foregone investment returns | Essentially none (zero balance) |

| Risk of loss of access | None | Real — lender can freeze |

| Home at risk | No | Yes — when drawn |

| Best emergency coverage | 3–6 months expenses | Large, unpredictable events |

| Behavioral risk | Low | Moderate — easy access |

| Appropriate for job loss | Yes — cash is available | Risky — freeze risk at worst time |

The Honest Bottom Line

A HELOC can be a smart component of an emergency preparedness strategy — but it is not a reliable replacement for a cash emergency fund.

The strategy works well for homeowners with stable high income, substantial equity, strong investment discipline, and the financial resilience to service HELOC debt even during a disruption. For these borrowers, a hybrid approach — small cash buffer plus HELOC plus investments — captures most of the financial benefit while managing the risks.

The strategy fails — sometimes seriously — for homeowners who use the HELOC as their only emergency reserve, who have thin equity positions, who have variable income, or who live in markets with volatile home values. For these borrowers, the conditions most likely to trigger the need for emergency funds are the same conditions most likely to make the HELOC unavailable.

The question to ask yourself honestly: If I lost my job tomorrow and my home’s value dropped 15% at the same time, would my HELOC still be available and could I service the debt if I drew from it?

If the answer is confidently yes — the strategy is viable for you. If the answer is uncertain or no — maintain a cash emergency fund as your primary safety net.

Use our HELOC Payment Calculator to understand exactly what a HELOC draw would cost you in monthly payments and total interest — so you know what you are taking on if you ever need to use it as emergency backup.