HELOC Early Payoff: Is It Worth It?

You have a HELOC balance sitting on your books. Maybe you have had it for a few years, maybe you are deep into the repayment period. Either way, the question has crossed your mind: should I just pay this thing off early?

It seems like an obvious yes. Eliminating debt feels good. Freeing up that monthly payment feels better. But the real answer — as with most personal finance decisions — depends on your specific numbers, your interest rate, what else you would do with that money, and a few costs most borrowers do not think about until it is too late.

This article gives you a complete, honest framework for deciding whether HELOC early payoff is worth it in your specific situation — including the math, the hidden costs, the opportunity cost question, and a step-by-step decision process to arrive at the right answer for you.

The Core Question: What Does Early Payoff Actually Save You?

Before anything else, you need to know your actual savings number. Early payoff is worth it or not based primarily on how much interest you avoid paying by eliminating the debt ahead of schedule.

The interest you save equals every future interest payment you would have made under the minimum payment schedule — from today until your original payoff date.

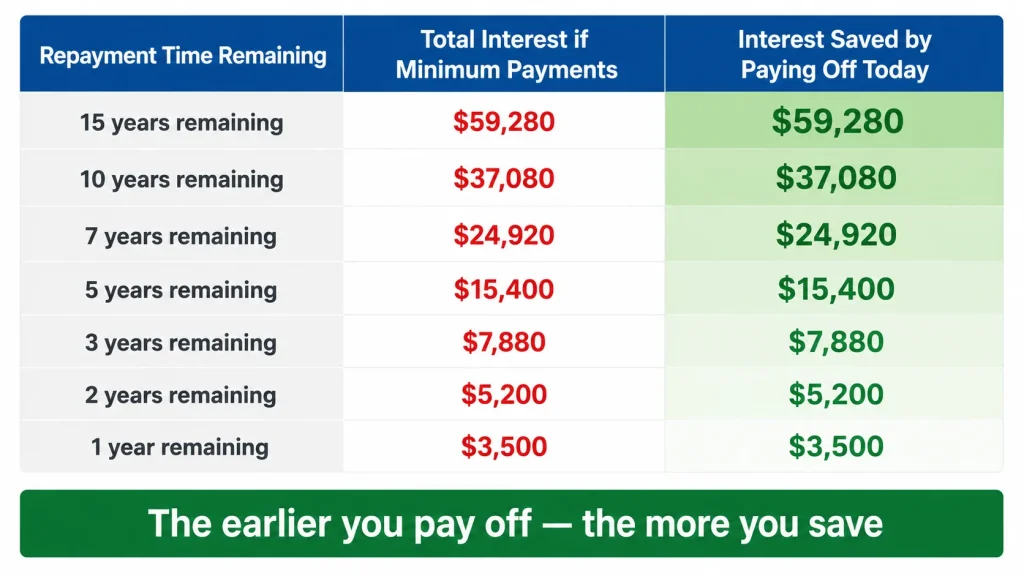

Here is what early payoff saves on a $75,000 HELOC balance at 8.75% depending on how far ahead of schedule you pay it off:

| Current Repayment Term Remaining | Total Interest if You Pay Minimums | Interest if You Pay Off Today | Interest Saved |

|---|---|---|---|

| 15 years remaining | $59,280 | $0 | $59,280 |

| 12 years remaining | $46,800 | $0 | $46,800 |

| 10 years remaining | $38,600 | $0 | $38,600 |

| 7 years remaining | $26,400 | $0 | $26,400 |

| 5 years remaining | $18,200 | $0 | $18,200 |

| 3 years remaining | $10,600 | $0 | $10,600 |

| 1 year remaining | $3,500 | $0 | $3,500 |

The further you are from your payoff date, the more valuable early payoff becomes. Paying off a HELOC with 15 years remaining saves nearly $60,000 in interest on a $75,000 balance. Paying it off with one year remaining saves $3,500 — meaningful, but far less impactful relative to the effort and liquidity required.

This savings number is your starting point. Everything else in the early payoff decision is measured against it.

Use our HELOC Payment Calculator to calculate your exact remaining interest under the minimum payment schedule — that is your maximum possible savings from early payoff.

The Hidden Cost: Early Termination Fees

Before you write a payoff check, check your loan agreement for an early termination fee.

Many lenders — particularly those who offered no-closing-cost HELOCs or promotional rate discounts — include an early termination clause that charges a fee if you close the HELOC within a specified period, typically the first 2 to 3 years after opening.

Common early termination fee structures:

| Lender Type | Typical Early Termination Fee | Window |

|---|---|---|

| Large national banks | $300 – $500 flat fee | First 24–36 months |

| Credit unions | $0 – $250 | First 12–24 months |

| Online lenders | $200 – $500 | First 24–36 months |

| No-closing-cost HELOCs | $500 – $750 | First 36 months |

This fee is triggered by closing the account — not by paying off the balance. This distinction is critical and often misunderstood.

If you are within the early termination window, you have two options:

Option A: Pay off the balance and close the account, paying the early termination fee. This makes sense if your interest savings from payoff far exceed the fee — which is almost always true if you have a meaningful balance and more than 2 years remaining in your repayment period.

Option B: Pay off the balance and leave the account open with a zero balance. You avoid the early termination fee entirely, retain the credit line as a financial safety net, and pay zero interest since there is no outstanding balance. This is the strategy most financial advisors recommend if you are within the termination window and your lender charges an annual fee of $100 or less.

The Opportunity Cost Question

This is the part of the early payoff decision that most borrowers skip — and it is the most important analytical step.

When you use money to pay off your HELOC early, you are making an implicit choice not to do something else with that money. The relevant question is: what is the best alternative use of those funds?

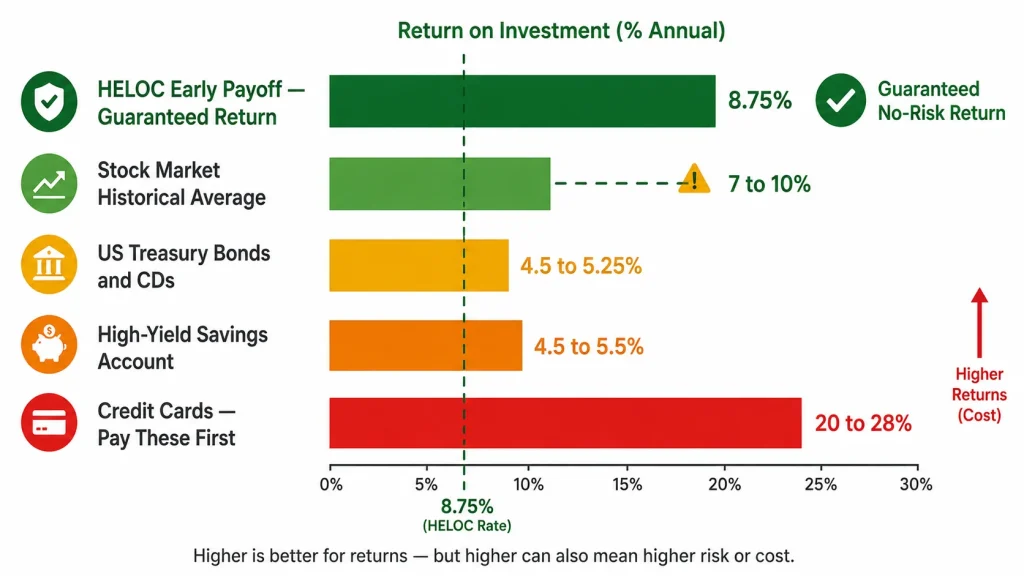

Your HELOC interest rate is your guaranteed, risk-free return on every dollar you put toward early payoff. In 2026, most HELOCs carry rates between 7.5% and 10%. Paying down an 8.75% HELOC delivers an 8.75% guaranteed return — because every dollar of principal you eliminate stops accruing 8.75% annual interest forever.

Now compare that to your alternatives:

High-yield savings accounts and money market funds are currently yielding 4.5% to 5.5% in 2026. Paying off your 8.75% HELOC beats keeping money in savings by roughly 3 to 4 percentage points annually. Early payoff wins clearly here.

US Treasury bonds and CDs are yielding approximately 4.5% to 5.25% for most terms in 2026. Again, your HELOC rate likely exceeds this. Early payoff wins.

Stock market investments have historically returned an average of 7% to 10% annually over long periods — though with significant volatility and no guarantee. If your HELOC rate is 8.75%, the stock market’s historical average return is roughly equivalent, but stock returns are not guaranteed while your HELOC interest savings are. This is a genuine toss-up that depends on your risk tolerance and investment timeline.

Paying off higher-interest debt — credit cards at 20%+, personal loans at 12%+. If you carry any of these, paying them off delivers a higher guaranteed return than paying off your HELOC. Pay the higher-rate debt first.

Investing in your home — if a home improvement investment would increase your home’s value by more than the cost of the project, this may outperform HELOC early payoff from a net worth perspective. However, home value appreciation is not guaranteed.

The Simple Rule

If your HELOC interest rate is higher than the after-tax return you can reliably earn elsewhere, early payoff is the better financial move. If your HELOC rate is lower than what you can reliably earn elsewhere, investing may outperform early payoff mathematically.

For most borrowers with HELOC rates above 8%, early payoff beats savings accounts and bonds clearly, and competes closely with long-term stock market returns when risk-adjusted.

Tax Considerations: Does HELOC Interest Deductibility Change the Math?

Before concluding that early payoff is always right for high-rate HELOCs, one more factor deserves consideration: tax deductibility.

Under current IRS rules, HELOC interest is tax deductible only if the funds were used to buy, build, or substantially improve the home securing the line of credit. If your HELOC funds were used for home renovation, the interest you pay may be deductible on Schedule A if you itemize deductions.

If your HELOC interest is deductible and you are in the 24% federal tax bracket, your effective after-tax HELOC rate is:

8.75% × (1 − 0.24) = 6.65% effective rate

At 6.65% effective cost, the opportunity cost calculation shifts. High-yield savings at 5.25% still loses to early payoff, but the margin narrows. Long-term stock market investments at 7–10% now clearly beat early payoff on a mathematical basis for many borrowers.

If your HELOC interest is not deductible — because you used the funds for debt consolidation, education, or other non-home purposes — this calculation does not apply and the full nominal rate is your true cost.

Always consult a tax professional to confirm whether your specific HELOC interest qualifies for deduction before factoring this into your payoff decision.

Early Payoff Scenarios: When It Clearly Makes Sense

There are situations where the early payoff decision is straightforward and the answer is clearly yes.

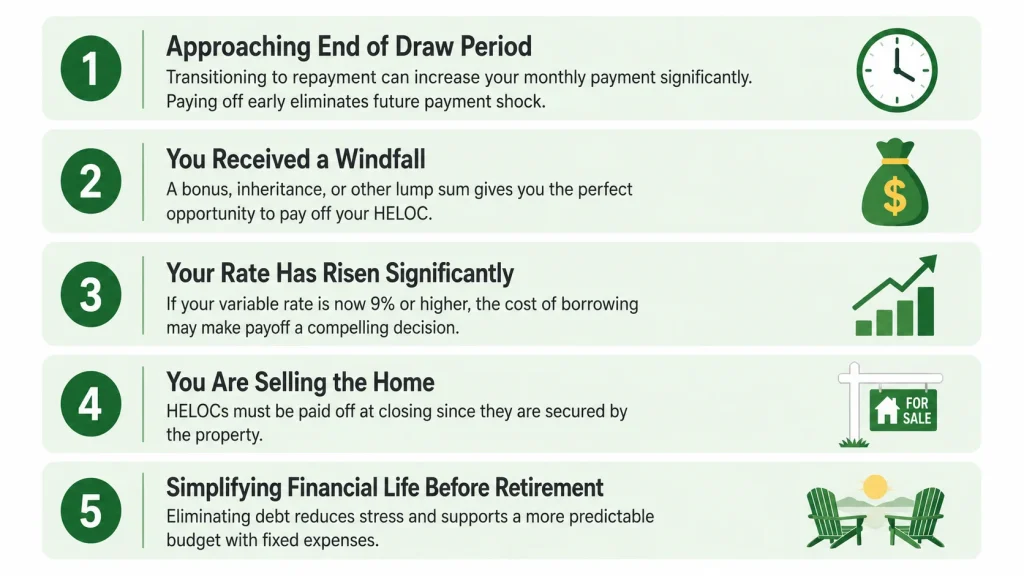

Scenario 1: You Are Approaching the End of Your Draw Period

If your draw period ends within 12 to 24 months and you are carrying a significant balance, paying it off before repayment begins eliminates payment shock entirely. You avoid the 35–37% minimum payment jump and the full remaining interest cost in one move.

A homeowner with a $80,000 balance, 18 months left in the draw period, and a 15-year repayment ahead of them would face $78,920 in interest if they let repayment run its course. Paying off the balance now eliminates that entire cost — minus the $10,350 in interest they will pay over the final 18 draw period months if they do not pay off immediately.

Net savings from paying off now vs. letting repayment run: approximately $68,500.

Scenario 2: You Received a Windfall

An inheritance, a business sale, a large bonus, or proceeds from a real estate transaction. When a lump sum arrives that exceeds your HELOC balance, the decision is usually simple: pay it off.

The guaranteed interest savings almost always outperform what you would earn keeping the windfall in a savings account or short-term investment, particularly for balances where meaningful repayment time remains.

Scenario 3: Your Rate Has Risen Significantly

If the Federal Reserve’s rate hikes since 2022 have pushed your HELOC rate from 5% to 9% or higher, your carrying cost has nearly doubled. At 9%+ HELOC rates, early payoff becomes extremely compelling — the guaranteed return exceeds most risk-free investment alternatives by 3 to 5 percentage points.

Scenario 4: You Are Selling the Home

If you are selling your home, your HELOC must be paid off at closing regardless — it is a lien on the property. In this case, early payoff is not a choice but a requirement. However, if you know you are selling within 6 to 12 months, it may make sense to pay off the HELOC now rather than waiting for closing, particularly if you have the funds available and want to simplify the transaction.

Scenario 5: Simplifying Your Financial Life

Sometimes the financial case for early payoff is not overwhelming but the psychological and lifestyle benefits are. Eliminating a monthly HELOC payment — even a modest one — reduces financial complexity, removes a variable payment from your budget, and eliminates a lien on your home.

For homeowners approaching retirement who want predictable, fixed expenses, early HELOC payoff can make sense even when the pure interest rate math is not conclusive.

Early Payoff Scenarios: When It May Not Make Sense

There are also clear situations where rushing to pay off a HELOC early is not the optimal financial move.

When You Carry Higher-Rate Debt

If you have credit card balances at 22%+, personal loans at 14%+, or other high-rate debt, every dollar you put toward your HELOC instead of those debts is costing you money. The debt avalanche principle is clear: eliminate the highest-rate debt first, regardless of which one feels most satisfying to pay off.

When Your Emergency Fund Is Insufficient

Using all available cash to pay off your HELOC and leaving yourself with no emergency fund is a dangerous trade. Financial advisors generally recommend maintaining 3 to 6 months of living expenses in liquid savings before aggressively paying down debt.

If paying off your HELOC would deplete your emergency fund below a comfortable level, consider a middle path: pay down as much as you comfortably can while preserving your safety net, rather than going all-in on payoff.

When Your HELOC Rate Is Low and Deductible

If you opened your HELOC several years ago at a rate below 5% and your interest is tax-deductible because you used the funds for home improvement, your effective after-tax rate may be as low as 3.5% to 4%. At that cost, long-term stock market investments, real estate, or even high-yield savings accounts may outperform early payoff mathematically.

This scenario is less common in 2026 given where variable rates sit, but borrowers with rate caps or legacy fixed-rate HELOC features may still be in this position.

When You Are Very Late in the Repayment Period

With only 1 to 2 years remaining on your HELOC, most of the interest has already been paid. The remaining interest cost on a $20,000 balance in year 14 of a 15-year repayment at 8.75% is roughly $1,500. If paying that off requires liquidating an investment account or incurring any cost, the math likely does not support aggressive acceleration at this late stage.

The Tax Implications of Early Payoff

Paying off your HELOC early is generally tax-neutral — you do not receive a tax benefit or incur a tax liability from payoff itself. However, there are two indirect tax considerations worth noting.

Loss of interest deduction. If your HELOC interest was tax-deductible and you itemize deductions, paying off the HELOC eliminates a future deduction. For borrowers in higher tax brackets who use home improvement proceeds, this is a real cost to factor into the decision.

Investment account liquidation. If you fund your HELOC payoff by selling investments in a taxable brokerage account, you may trigger capital gains taxes. A long-term capital gain at 15% to 20% tax rates is a real cost that reduces the effective benefit of the payoff. Always model the after-tax cost of liquidating investments before using them to pay off a HELOC.

For example, if you sell $75,000 in appreciated stock with a $30,000 cost basis, you may owe $6,750 in capital gains taxes at the 15% rate. That $6,750 tax bill reduces your effective payoff savings by the same amount and should factor into your decision.

Consult a tax advisor before liquidating significant investment positions to fund a HELOC payoff.

How to Pay Off Your HELOC Early: Practical Steps

Once you have decided early payoff makes sense, here is how to execute it cleanly.

Step 1: Request a payoff quote from your lender. Contact your lender and ask for a formal payoff statement showing the exact amount needed to pay off the balance in full, including any accrued interest through the payoff date. This number changes daily as interest accrues, so get the quote close to your intended payment date.

Step 2: Confirm the early termination fee situation. Ask your lender directly: “Is there an early termination fee if I close this account?” and “When does that window expire?” Get the answer in writing.

Step 3: Decide whether to close or keep open. If you are within the early termination window, decide whether to close the account and pay the fee or pay off the balance and leave it open. If your lender charges no annual fee, leaving it open is usually the smarter move.

Step 4: Submit the payoff amount. Wire the payoff amount or submit it through your lender’s online payment system. Specify clearly that this is a payoff payment, not a regular monthly payment. Some lenders require you to call or send a written payoff request to ensure proper processing.

Step 5: Confirm the lien release. After payoff, your lender is required to release their lien on your property by filing a lien release or deed of reconveyance with your county recorder’s office. This typically takes 30 to 90 days. Confirm it happened by checking your county property records online or requesting written confirmation from your lender.

Step 6: Redirect the payment. Once your HELOC payment disappears from your monthly budget, redirect that amount immediately to another financial goal — retirement contributions, emergency fund, mortgage paydown — before lifestyle inflation absorbs it.

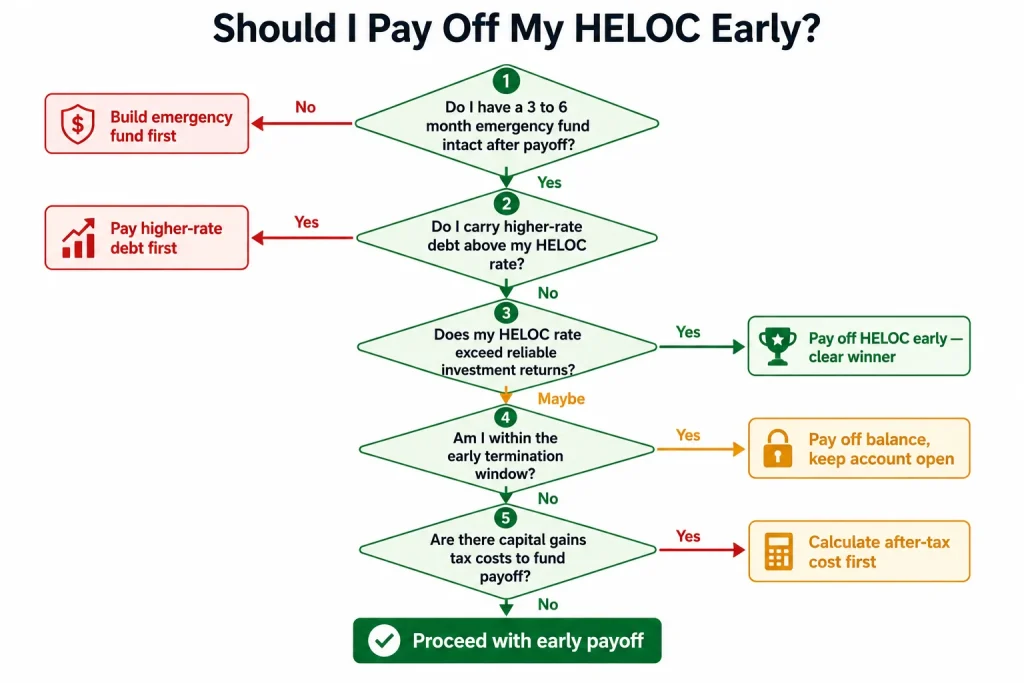

The Early Payoff Decision Framework: A Simple Yes/No Guide

Run through these five questions to arrive at your answer:

Question 1: Do I have an adequate emergency fund (3–6 months of expenses) that will remain intact after payoff?

- No → Build the emergency fund first. Partial paydown only.

- Yes → Continue to Question 2.

Question 2: Do I carry any higher-rate debt (credit cards, personal loans above my HELOC rate)?

- Yes → Pay off higher-rate debt first using the debt avalanche method.

- No → Continue to Question 3.

Question 3: What is my effective after-tax HELOC rate, and does it exceed what I can reliably earn elsewhere?

- HELOC rate exceeds alternatives → Early payoff is likely the right move.

- Alternatives clearly exceed HELOC rate → Invest instead, continue minimum payments.

- Rates are roughly equal → Personal preference and risk tolerance decide.

Question 4: Am I within the early termination window?

- Yes → Calculate whether payoff savings exceed the early termination fee. If yes, proceed with payoff. If no or close, pay off balance and keep account open.

- No → Proceed with payoff and close if desired.

Question 5: Are there tax consequences from liquidating assets to fund payoff?

- Yes → Calculate after-tax cost and factor into the savings comparison.

- No → Proceed with payoff.

If you reach the end of this framework with a clear answer, act on it. If the answer is genuinely borderline, the psychological benefit of debt elimination is a real, legitimate factor that can tip the scale.

The Bottom Line

HELOC early payoff is worth it for most borrowers, most of the time — particularly those with rates above 8%, significant time remaining in repayment, and available cash that would otherwise sit in lower-yield savings or bonds.

The cases where it is not worth it are specific: higher-rate debt exists elsewhere, the emergency fund would be depleted, the effective after-tax HELOC rate is genuinely low, or investment alternatives clearly outperform the guaranteed interest savings.

The right answer is always in your numbers. Calculate your remaining interest cost, compare it to your best alternative use of funds, account for any early termination fee, and make the decision with full information rather than gut feeling.

Use our HELOC Payment Calculator to find your exact remaining interest cost under the minimum payment schedule — that single number tells you exactly what is at stake and makes the early payoff decision straightforward.