How Long Does HELOC Approval Take?

The honest answer is somewhere between two weeks and six weeks — with a few lenders getting it done faster and a few situations stretching it longer. The range is real and it matters for planning.

A homeowner who needs $40,000 for a kitchen renovation starting in three weeks needs to know whether they are going to have access to those funds in time. A homeowner planning a project for next quarter has no urgency but wants to understand the process. The right answer depends on who you are applying with, what your property looks like, and how prepared your documents are.

This article breaks down the HELOC approval timeline stage by stage — what happens, how long each part actually takes, what slows things down, and what you can do to move faster.

The Overall Timeline: What to Expect

For most borrowers applying at a traditional bank or credit union in 2026, the total time from application submission to funded HELOC runs 3 to 6 weeks. Online lenders using automated technology can get it done in 10 to 21 days for qualifying applications.

Here is the full timeline broken down by stage:

| Stage | Traditional Lender | Online Lender |

|---|---|---|

| Application review | 2–5 business days | 1–2 business days |

| Appraisal scheduling | 5–10 business days | Same day (AVM) |

| Appraisal completion | 1–3 days after visit | Same day (AVM) |

| Underwriting review | 5–10 business days | 3–5 business days |

| Conditional approval items | 2–5 days (if needed) | 1–3 days |

| Title search | 5–10 business days | 3–5 business days |

| Clear to close | 1–2 business days | 1–2 business days |

| Closing and rescission | 4–5 business days | 4–5 business days |

| Total estimate | 3–6 weeks | 10–21 days |

These are realistic averages for a smooth application. Any stage can run longer if documents are missing, the appraisal comes in with issues, the title search finds problems, or the underwriter requests additional information.

Stage-by-Stage Breakdown

Application Review: 2–5 Business Days

After you submit your application, a loan processor at the lender reviews it to make sure everything is complete and the basic qualification criteria appear to be met. They check your credit, verify the basic income figures, and confirm the property information.

If your application is complete and your profile is straightforward, this stage moves quickly. If documents are missing or the initial credit check raises questions — an unexplained derogatory item, a DTI that is close to the limit — the processor will request additional information before moving forward.

What slows this stage: Incomplete applications. Missing documents. Credit issues that require explanation letters.

What speeds it up: Submitting a complete application with all documents attached from day one. If your credit report has any items that might need explanation — a late payment two years ago, a collection that was paid — write the explanation letter proactively and include it with the application.

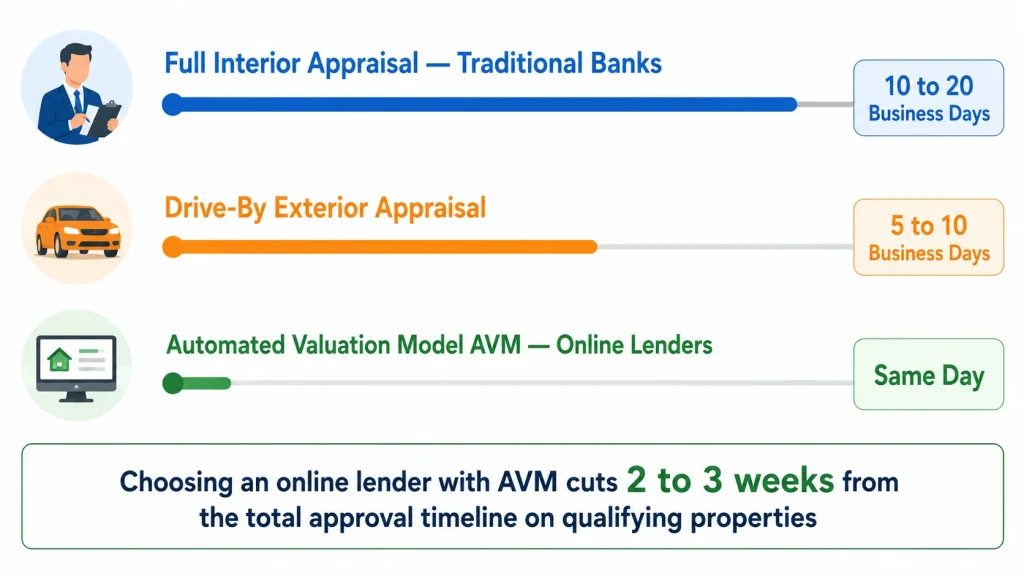

The Appraisal: The Biggest Variable in the Timeline

The appraisal is the stage with the most variability in the timeline and the most potential for surprises. It is also the one borrowers have the least control over once it is underway.

Full interior appraisal at a traditional lender:

The lender orders the appraisal after the initial application review is complete. Scheduling depends on appraiser availability in your market — in busy spring and summer markets, appraisers book out 7 to 14 days. Once the appointment is completed, the appraiser typically has 3 to 5 business days to deliver the report to the lender.

From order to delivery, a full appraisal typically takes 10 to 20 business days — the single longest stage in the traditional HELOC process.

Automated Valuation Model (AVM) at online lenders:

Online HELOC lenders like Figure, Spring EQ, and Aven often use AVMs for qualifying properties — a computer-generated estimate based on public records and comparable sales data. There is no scheduling, no appraiser visit, no waiting. The AVM result comes back in minutes.

This is why online lenders can close HELOCs in 10 to 21 days while traditional banks take 3 to 6 weeks. The appraisal stage goes from two to three weeks to essentially zero.

AVMs are not available for all properties. Complex homes, rural properties, properties with limited comparable sales, and situations where the estimated value is near the lender’s CLTV limit may require a full appraisal even at online lenders.

What can slow the appraisal:

Appraiser availability in your market. A property with limited comparable sales — unusual design, rural location, recent significant renovation — requires more research and time. A home with visible deferred maintenance or condition issues may lead to a required repairs addendum that must be addressed before the lender accepts the appraisal.

What speeds it up:

Choose a lender that uses AVMs if your property is a standard single-family home in a market with clear comparable sales data. If you need a full appraisal, have the property in good presentable condition before the appointment. Be flexible on scheduling — accepting the appraiser’s earliest available slot rather than waiting for a more convenient day can save a week.

Underwriting Review: 5–10 Business Days

Underwriting is where the lender’s underwriter reviews the complete file — income documentation, credit report, appraisal, title search (when available), and property insurance — and makes the formal credit decision.

For clean, well-documented applications, underwriting at a traditional lender takes 5 to 7 business days. For files with complexity — self-employed income, unusual property types, borderline DTI — it can stretch to 10 to 14 business days.

Conditional approval is the most common outcome at this stage rather than a clean approval. The underwriter approves the loan subject to specific conditions — usually additional documents or written explanations. Common conditions include:

- A letter of explanation for a credit inquiry or derogatory item

- Documentation of a large deposit in a bank account

- Clarification of a specific income item on a tax return

- Updated pay stub if a prior one is more than 60 days old

- Proof that a specific debt shown on the credit report has been paid

Receiving a conditional approval is normal — it is not a sign of trouble. It means the underwriter has done the work and needs one more thing before signing off. The key is responding within 24 hours. Every day a condition sits unanswered is a day added to the timeline.

What slows underwriting: Self-employed income that requires extensive documentation. Business tax returns with complex structures. Income that decreased between year one and year two of the provided tax returns. Properties in flood zones requiring additional insurance verification.

What speeds it up: Providing complete, well-organized documentation at the application stage. Responding immediately to every condition request. If you are self-employed, attaching a two-paragraph summary of your business and income structure to the application reduces the back-and-forth.

Title Search: 5–10 Business Days

The title search confirms that you legally own the property and that no undisclosed liens, claims, or encumbrances exist against it. A title company reviews public property records going back decades.

This stage typically runs concurrently with underwriting rather than sequentially — a lender that is efficient will order the title search while underwriting is in progress rather than waiting for underwriting to complete first. When this is done in parallel, it adds little to the overall timeline.

Title searches come back clean in the vast majority of cases. When they do not — an unreleased mechanic’s lien from a contractor, a boundary dispute, an old lien from a deceased co-owner — the timeline can extend significantly while the issue is resolved.

What slows it: A property with a complex ownership history. Prior construction work that was not properly paid or lien released. Inherited properties or properties transferred through divorce where documentation may be incomplete.

What speeds it up: If your property has had any contractor work in the past three years, confirm that all contractors filed lien releases after payment. This is something to handle before applying, not during the title search.

Closing and the Three-Day Rescission: 4–5 Business Days

Once underwriting clears and the title is clean, the lender schedules closing. For in-person closings, scheduling adds a day or two. For remote electronic closings with online notarization, it can happen within 24 to 48 hours of the clear-to-close.

After signing, federal law requires a mandatory three-business-day rescission period before the HELOC on a primary residence becomes active. This waiting period cannot be waived or shortened. The lender cannot disburse funds during this time.

Closing plus rescission adds a minimum of four to five business days to the tail end of every HELOC process regardless of how fast everything else went.

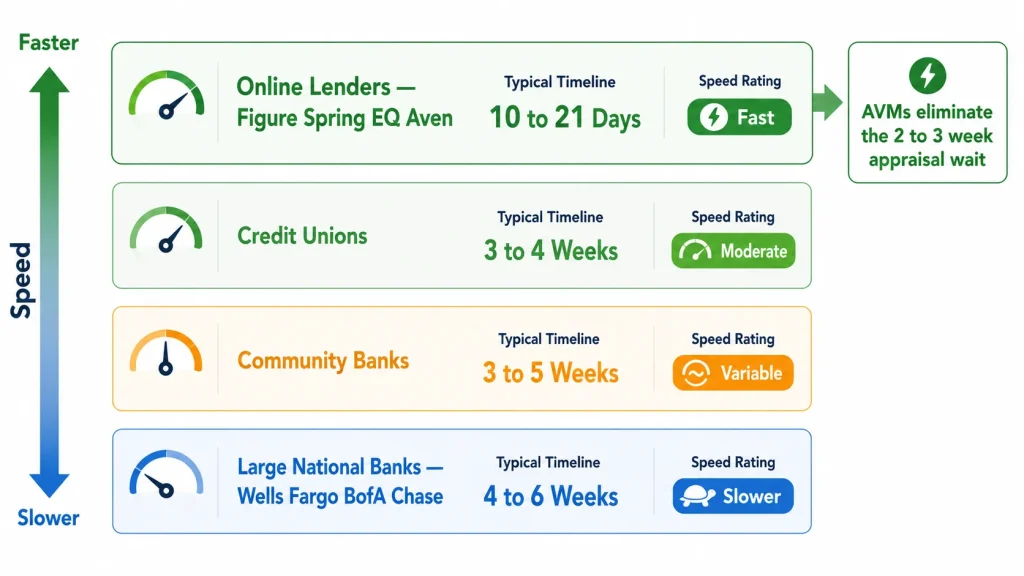

How Different Lender Types Compare on Speed

Not all lenders process at the same pace. Understanding which types of lenders move fastest — and why — helps you choose the right one for your timeline needs.

Online lenders (fastest):

Figure, Spring EQ, and Aven are the fastest HELOC lenders in the market. All-digital applications, AVM-based property valuations, and streamlined underwriting processes allow them to close qualifying applications in 10 to 14 days. Some advertise as fast as 5 days though that is rare in practice for standard applications.

The trade-off: less flexibility for unusual borrower situations, property types, or applications that fall outside their automated underwriting parameters. If your application is straightforward, online lenders are hard to beat on speed.

Credit unions (moderate speed):

Credit unions typically close HELOCs in 3 to 4 weeks — faster than large banks because of less bureaucratic overhead and more human-involved decision-making that can move quickly when the file is clean. The trade-off is that credit union capacity varies — a small credit union with two underwriters handles volume differently than a large one.

Large national banks (slowest):

Wells Fargo, Bank of America, Chase, and similar institutions typically run 4 to 6 weeks for HELOC approvals. Their processes are more standardized and have more review layers. The trade-off for the slower timeline is broad product availability, established customer relationships, and the ability to handle complex applications.

Community banks (variable):

Ranges from 3 to 6 weeks depending on the institution, their current loan pipeline, and appraiser availability in the local market. Best for unusual property types or borrower situations that benefit from human underwriting judgment.

What Causes Delays — The Real List

Beyond the stage-by-stage factors above, here are the specific situations that push timelines well beyond the typical range.

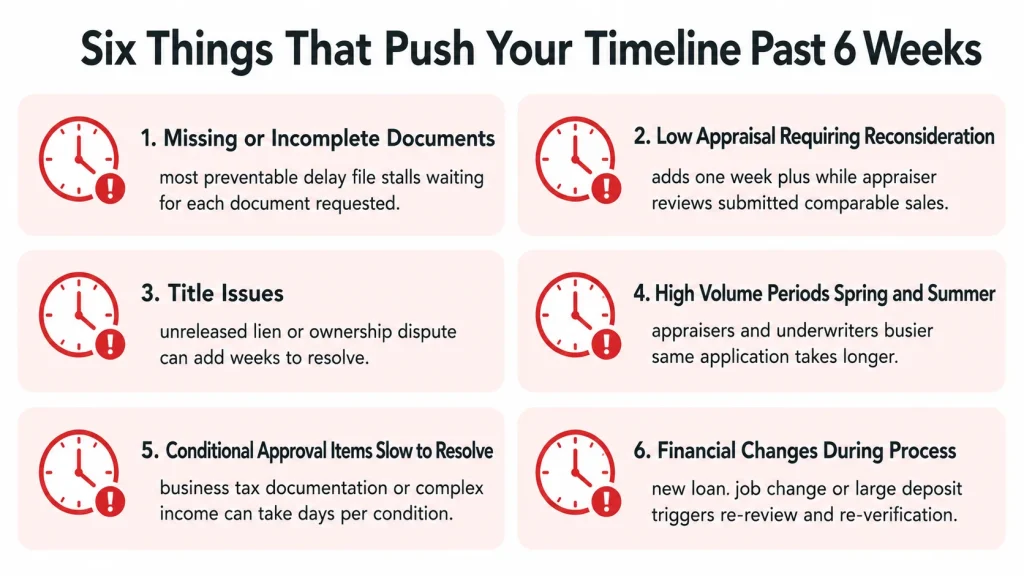

Missing or incomplete documents. The most preventable delay. Every time a lender has to ask for a document that should have been submitted at application, the file stalls while waiting for your response. Getting everything together before applying — not in response to individual requests — is the single most impactful thing you can do for timeline.

Low appraisal requiring reconsideration. If the appraisal comes in below the value needed to support your credit line request, you may need to request a reconsideration of value. This adds a week or more while the appraiser reviews your submitted comparable sales and produces a response.

Title issues. An unreleased lien or ownership dispute can add weeks while the issue is resolved. Not much you can do if this surfaces — but confirming your title is clean before applying, through a preliminary title search or a conversation with an attorney in states where that is common, can identify issues early.

Lender pipeline volume. In spring and early summer — the peak home equity borrowing season — lenders and appraisers are busier. The same application that takes four weeks in January might take six weeks in May simply because of volume. If you have flexibility on when you apply, fall and winter tend to be faster.

Conditional approval items that take time to resolve. Some conditions are quick — a letter of explanation takes an hour. Others are slow — documentation of a business asset or clarification of a complex tax situation can take days.

Changes to your financial profile during the process. A new car loan, a job change, a large unverified deposit — any of these discovered during underwriting triggers re-review and potentially re-verification of income or assets. The file does not move forward until everything is re-cleared.

How to Speed Up Your Approval

If your timeline is tight, here are the most effective ways to accelerate the process.

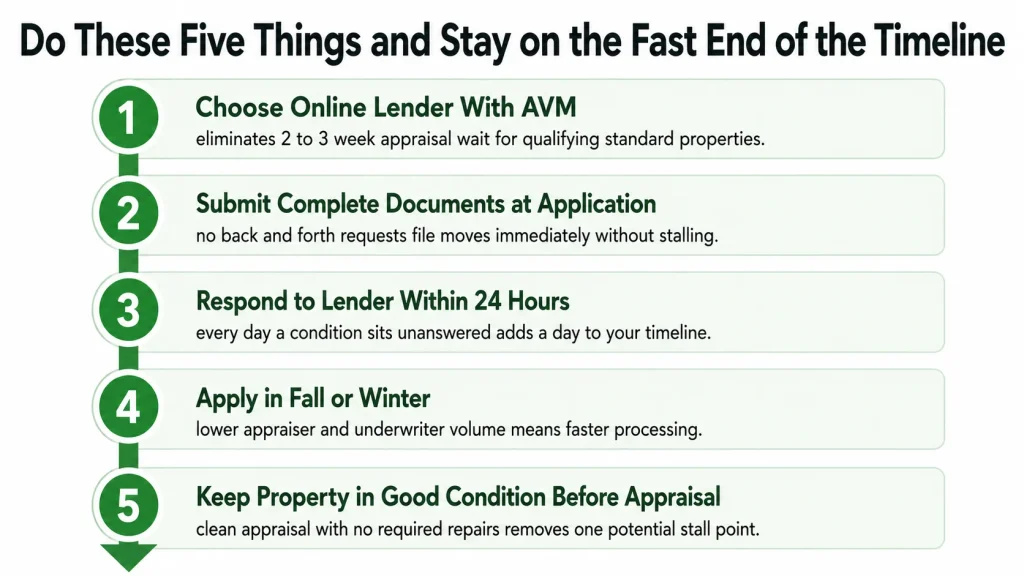

Choose an online lender with AVM-based valuations. If your property qualifies, this alone cuts two to three weeks from the typical timeline by eliminating the full appraisal scheduling and completion wait.

Submit a complete application with all documents attached. Do not wait for the lender to ask. Provide every document on the standard list with the initial application — tax returns, pay stubs, bank statements, insurance declarations page, mortgage statement. Files that arrive complete move immediately. Files that require document requests stall.

Respond to every lender communication within 24 hours. The clock stops ticking on your application whenever the lender is waiting for something from you. Same-day or next-morning responses on every request maintain momentum.

Apply during lower volume periods. Fall and winter applications face shorter appraiser queues and less underwriting backlog than spring and summer applications. If timing is flexible, November through February tends to move faster.

Have your property in good condition before the appraisal. Visible deferred maintenance, safety issues, or condition items that the appraiser flags can require corrective action before the lender accepts the report. A home in good condition produces a cleaner appraisal with no required repairs — one less potential stall.

Apply to your existing lender first if timeline is critical. Your primary bank or mortgage lender already has your account information on file, may have a pre-existing relationship with your income history, and sometimes offers expedited processing for existing customers.

If You Need Funds Faster Than a HELOC Can Deliver

Sometimes the timeline does not match the need. A contractor needs a deposit in ten days. An emergency repair cannot wait three weeks. If you need funds faster than a HELOC process allows, consider these bridge options:

Personal loan: Online personal lenders fund in 1 to 3 business days. The rate is higher than a HELOC — typically 10% to 20% depending on your credit — but for a short-term bridge while your HELOC application processes, the interest cost on a modest amount for a few weeks is manageable. Pay it off with the HELOC draw the moment your credit line is active.

0% APR credit card: For amounts under $10,000 to $15,000, a 0% introductory rate card can bridge the gap without interest if you pay it off within the promotional window. Apply for this before you need it — credit card approvals are instant but cards take 7 to 10 days to arrive.

Draw on existing HELOC: If you already have a HELOC open with available credit — even at a higher rate from years ago — use it for the immediate need. Once your new HELOC is funded, pay off the old one.

The Bottom Line

Plan for three to six weeks if you are going with a traditional bank or credit union. Plan for two to three weeks if you are using an online lender with automated valuations on a straightforward property. Plan for potentially longer if your property is unusual, your income documentation is complex, or you are applying during peak borrowing season.

The most reliable way to stay on the faster end of any range: gather all documents before applying, choose a lender whose technology matches your property type, and respond within 24 hours at every stage. Borrowers who do those three things consistently close faster than the averages suggest.

Use our HELOC Payment Calculator to model your projected payments while you wait for approval — so you arrive at closing with a clear picture of what you are committing to.