Can You Get a HELOC with Bad Credit?

The short answer is: sometimes. It depends on how bad your credit actually is, how much equity you have in your home, what your income looks like, and which lenders you approach.

A 580 credit score with 40% home equity and a stable W-2 income is a different conversation than a 580 credit score with 15% equity and variable self-employment income. Both are technically “bad credit” but they face completely different odds and different options.

This article gives you an honest picture of what is possible, what it costs, and what you can do to improve your position — whether you apply now or spend a few months preparing for a stronger application.

First: What “Bad Credit” Actually Means for a HELOC

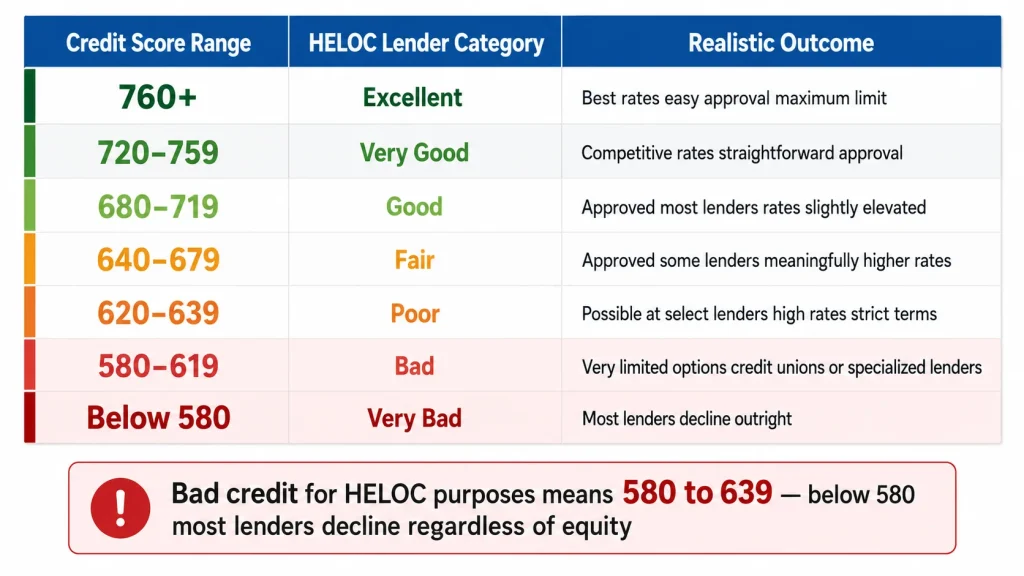

Credit score ranges mean different things in different lending contexts. For HELOCs specifically, here is how lenders categorize scores in 2026:

| Credit Score | HELOC Lender Category | Realistic Outcome |

|---|---|---|

| 760+ | Excellent | Best rates, easy approval, maximum credit limit |

| 720–759 | Very good | Competitive rates, straightforward approval |

| 680–719 | Good | Approved at most lenders, rates slightly elevated |

| 640–679 | Fair | Approved at some lenders, meaningfully higher rates |

| 620–639 | Poor | Possible at select lenders, high rates, strict terms |

| 580–619 | Bad | Very limited options, credit unions or specialized lenders |

| Below 580 | Very bad | Most lenders decline outright |

When people ask about getting a HELOC with “bad credit,” they are usually in the 580–639 range. Below 580 is a much harder situation that requires honest assessment of whether a HELOC is the right tool at all right now.

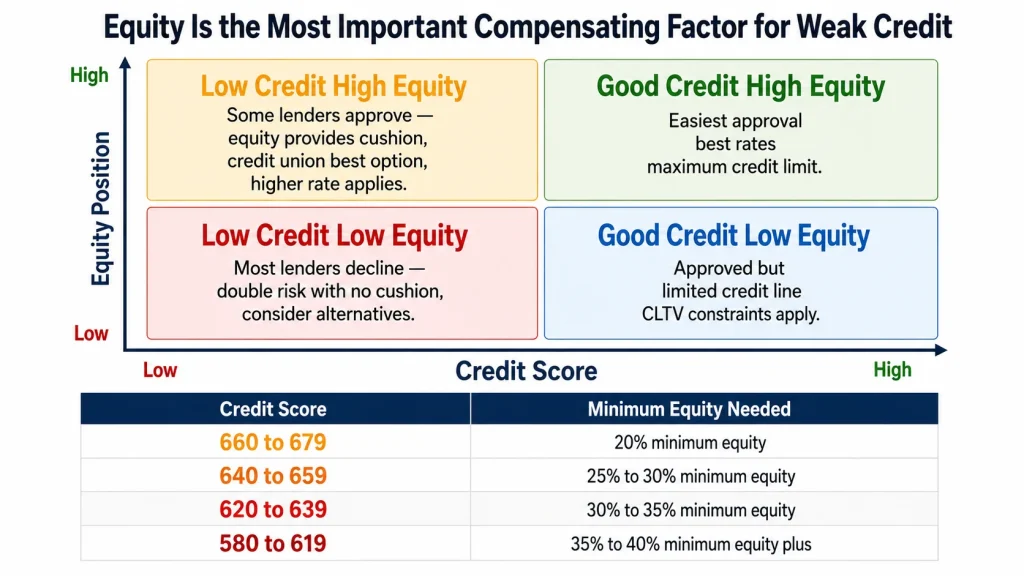

The Credit-Equity Trade-Off: What Lenders Actually Think About

HELOC underwriting is not purely about credit score. It is about the total risk picture — and a strong equity position can partially offset a weaker credit profile because it reduces the lender’s loss exposure if something goes wrong.

Think about it from the lender’s perspective. If you have 45% equity in your home and a 620 credit score, the lender is lending against a property with a large value cushion. Even if you default and the home has to be sold, there is substantial buffer before the lender takes a loss. That changes the risk calculation.

Compare that to a borrower with a 620 credit score and 18% equity. There is very little cushion. A modest property value decline combined with a default could result in the lender not recovering the full balance.

This is why equity position is the single most important compensating factor for borrowers with below-average credit. More equity genuinely changes what lenders will do.

Rough real-world guidelines for 2026:

| Credit Score | Minimum Equity Likely Needed | Notes |

|---|---|---|

| 660–679 | 20% | Standard requirement, some flexibility |

| 640–659 | 25–30% | Lenders want extra cushion |

| 620–639 | 30–35% | Most lenders require this before considering |

| 580–619 | 35–40%+ | Only select lenders, high equity required |

| Below 580 | Rarely approved regardless of equity | Hard limit for most institutions |

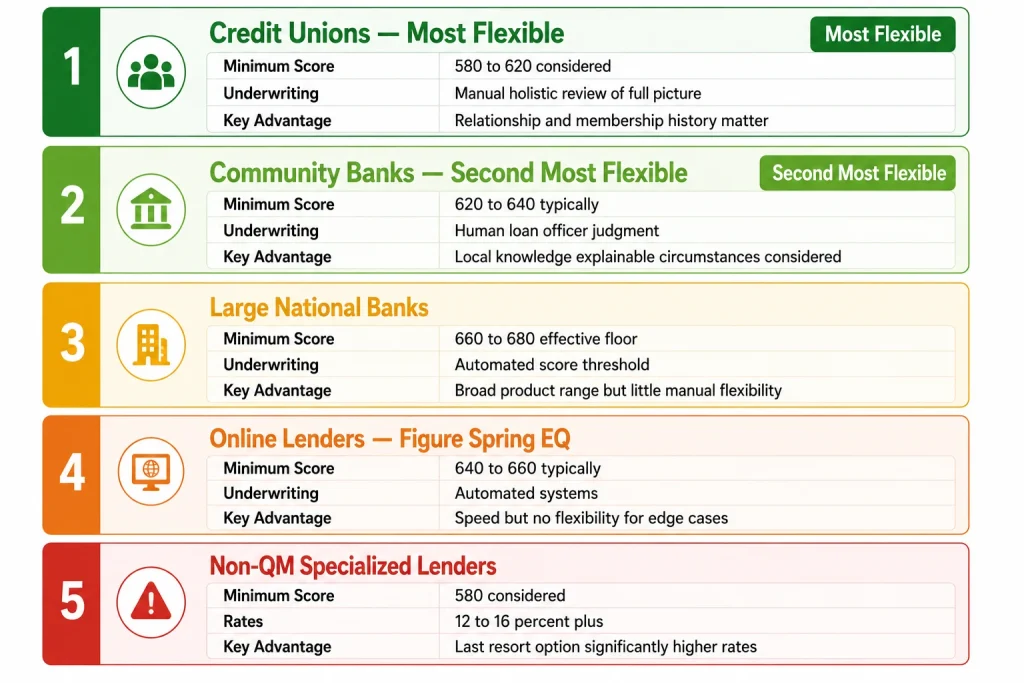

Which Lenders Will Actually Work With Bad Credit Borrowers

Not all lenders are equally willing to work with borrowers who have credit challenges. The type of lender matters as much as the score.

Credit Unions: The Most Flexible Option

Credit unions are the most practical option for borrowers with credit scores in the 580–640 range. As member-owned nonprofit institutions, credit unions tend to take a more holistic view of an application — considering the full picture of your financial situation rather than relying primarily on an automated credit score threshold.

Many credit unions will manually underwrite a HELOC application for a member with a lower credit score if the equity position is strong, the income is stable, and the credit issues have an explainable cause (medical hardship, divorce, a period of unemployment that has since resolved).

The key is the relationship. If you have been a member of a credit union for several years, have your checking and savings accounts there, and have a pattern of responsible account management — that history matters and they will often consider the full context.

If you are not currently a member of a credit union, research options in your area. Many credit unions have broad membership eligibility based on where you live, where you work, or professional associations. Joining takes 15 to 30 minutes and a small deposit.

Community Banks

Community banks with local loan officers who make manual underwriting decisions are the second most flexible option. A loan officer at a community bank who knows your local market and can review your file with human judgment — rather than handing it to an algorithm — is more likely to find a path forward for a borrower with credit challenges than a large national bank’s automated system.

Community banks are particularly valuable if your credit issues are explainable by a specific circumstance — a medical event, a business failure during COVID, a divorce — rather than a pattern of financial irresponsibility.

Large National Banks

Wells Fargo, Bank of America, Chase, and similar institutions use automated underwriting systems that apply consistent score thresholds. Most have effective minimums of 660 to 680 and will decline applications below that threshold without much room for manual override.

If your score is below 660, large national banks are unlikely to be the right starting point. Apply here only after you have been turned down at credit unions and community banks — or if your score is close to their threshold and your equity and income are very strong.

Online HELOC Lenders

Online lenders like Figure and Spring EQ are generally not flexible on credit scores. Their business model depends on standardized automated underwriting, and they tend to have minimum score requirements of 640 to 660. Below those thresholds, their systems simply decline.

Specialized or Non-QM Lenders

A small segment of lenders specialize in non-qualified mortgage products for borrowers who do not fit conventional underwriting boxes. These lenders will sometimes extend HELOCs or home equity loans to borrowers with credit in the 580–620 range — but at significantly higher rates and with stricter LTV requirements.

Rates for these products in 2026 typically run 12% to 16% or higher. The interest cost starts to resemble private lending more than conventional home equity borrowing. At these rates, carefully model the total cost before proceeding — the rate premium may make the loan less financially sensible than alternatives.

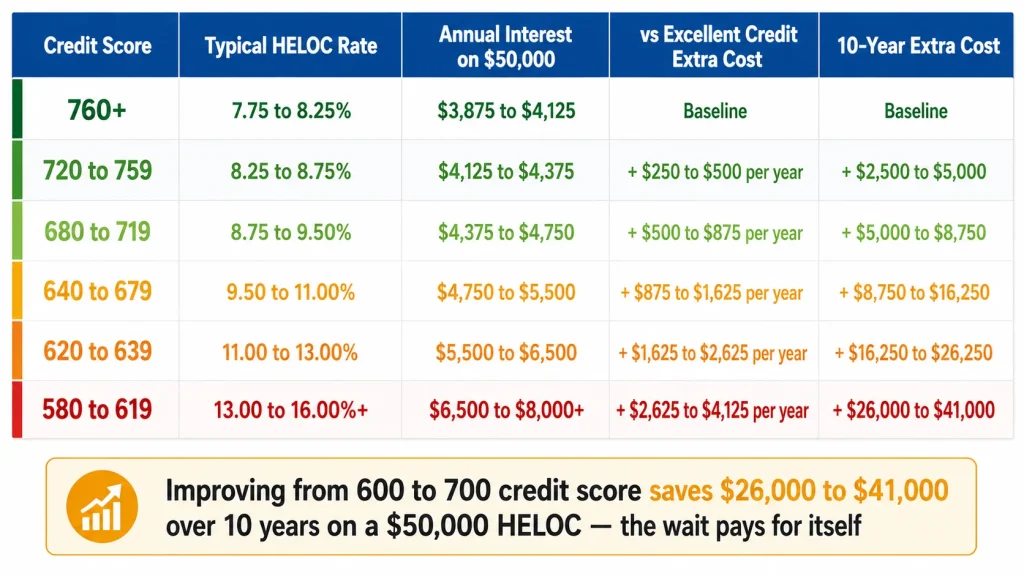

What Bad Credit HELOCs Actually Cost

If you do qualify for a HELOC with a below-average credit score, the interest rate you pay will be meaningfully higher than what well-qualified borrowers receive. Here is a realistic rate comparison in 2026:

| Credit Score | Typical HELOC Rate | Annual Interest on $50,000 | vs. Excellent Credit |

|---|---|---|---|

| 760+ | 7.75%–8.25% | $3,875–$4,125 | Baseline |

| 720–759 | 8.25%–8.75% | $4,125–$4,375 | +$250–$500/yr |

| 680–719 | 8.75%–9.50% | $4,375–$4,750 | +$500–$875/yr |

| 640–679 | 9.50%–11.00% | $4,750–$5,500 | +$875–$1,625/yr |

| 620–639 | 11.00%–13.00% | $5,500–$6,500 | +$1,625–$2,625/yr |

| 580–619 | 13.00%–16.00%+ | $6,500–$8,000+ | +$2,625–$4,125/yr |

On a $50,000 HELOC, a borrower with a 600 credit score might pay $3,000 to $4,000 more per year in interest than a borrower with a 760 score from the same lender. Over a 10-year draw period, that gap compounds to $30,000 to $40,000 in additional interest cost.

This is the financial argument for spending three to six months improving your credit score before applying — even if you qualify now at a lower rate, the total savings from a higher score can be substantial.

The Specific Credit Issues That Hurt Most and How Lenders View Them

Not all credit damage is equal in a lender’s eyes. Some issues are more disqualifying than others. Understanding how lenders view specific items helps you assess your realistic position.

Recent Late Payments (Last 12 Months)

This is the most damaging active credit issue for HELOC applications. A 30-day late payment in the past 12 months raises a direct question in the underwriter’s mind: if this borrower is having trouble paying current obligations now, how will they handle an additional HELOC payment?

Most lenders require a clean 12-month payment history. If you have a recent late, the most effective strategy is waiting — let the 12-month clean window develop before applying.

Collections and Charge-Offs

Unpaid collections and charge-offs hurt your score and concern lenders — but less so than recent late payments on active accounts. A collection from four years ago from a medical bill is viewed differently than a recent charge-off on a credit card.

Some lenders require all collections to be paid before approving a HELOC. Others will approve with unpaid collections if they are old and the current account history is clean. Ask specifically.

Bankruptcy

Chapter 7 bankruptcy: Most lenders require two to four years from discharge before considering a HELOC application. A few credit unions will consider applications two years post-discharge with strong equity and clean post-bankruptcy history.

Chapter 13 bankruptcy: More complex. You must typically receive court permission to take on new debt during an active Chapter 13 repayment plan. After discharge, lenders typically require one to two years of clean history.

Foreclosure

A prior foreclosure is one of the most disqualifying items for a home equity product. Most lenders require five to seven years from the foreclosure date before considering a HELOC. Some non-QM lenders will go back three years with substantial equity requirements.

High Credit Utilization

High utilization (above 60–70% of available revolving credit) drags your score but is also the most immediately fixable issue. Paying down credit card balances before applying can improve your score by 30 to 80 points within a single billing cycle depending on your specific utilization levels.

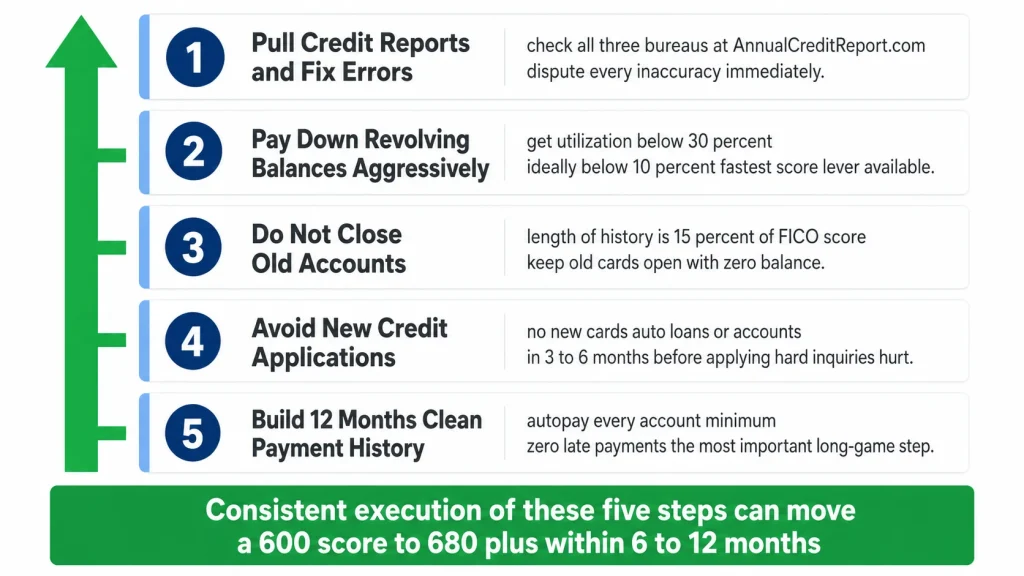

Five Steps to Improve Your HELOC Odds With Bad Credit

If you cannot qualify for a HELOC now — or can qualify but at a rate that makes the math difficult — here is a focused improvement plan.

Step 1: Pull Your Credit Reports and Fix Errors

Start at AnnualCreditReport.com and pull all three bureau reports. Look for accounts that are not yours, late payments that were reported incorrectly, collections that have been paid but still show as unpaid, and any other inaccuracies.

File disputes for every error with the relevant bureau. Errors take 30 to 45 days to resolve but the score improvement can be immediate and significant when legitimate errors are removed.

Step 2: Pay Down Revolving Balances Aggressively

Getting your total credit card utilization below 30% — ideally below 10% — is the fastest score improvement lever available. If you have $15,000 in available credit card limits and currently owe $9,000 (60% utilization), paying that down to $4,500 (30%) can add 40 to 60 points to your score in the first billing cycle after the lower balance reports.

This single step alone can move a 620 score to 660–680 for borrowers whose primary score drag is utilization rather than derogatory history.

Step 3: Do Not Close Old Accounts

Length of credit history is 15% of your FICO score. Closing an old credit card — even one you do not use — shortens your average account age and can hurt your score. Keep old accounts open with small balances or zero balances.

Step 4: Avoid New Credit Applications

Every hard inquiry lowers your score slightly and opens a new account that reduces your average account age. In the three to six months before applying for a HELOC, do not apply for any new credit — cards, auto loans, or anything else.

Step 5: Build 12 Months of Clean Payment History

This is the most important long-game step. Pay every bill on time, every month, without exception. A 12-month clean payment record carries significant weight with lenders — particularly for borrowers with prior credit issues — because it demonstrates that the past problems are behind you.

Set up autopay for every account minimum payment so a missed payment never happens due to oversight.

Alternatives If You Cannot Qualify for a HELOC Right Now

If your credit score is too low to qualify for a HELOC at terms that make financial sense, consider these alternatives while you work on improving your profile.

Personal loan: Unsecured personal loans are available to borrowers with credit scores as low as 580–600 from online lenders like Upstart, LendingPoint, and OneMain Financial. Rates are higher — 20% to 36% for poor credit — but no home equity is required and approval is fast. For smaller amounts ($5,000 to $15,000) needed urgently, this is sometimes the practical path.

FHA cash-out refinance: If you have at least 20% equity and an FHA-eligible property, an FHA cash-out refinance allows credit scores as low as 500 (with 20%+ equity) or 580 (with lower equity requirements at some lenders). This replaces your entire mortgage at current rates — which has significant cost implications — but it is a path to accessing equity that the conventional HELOC market may not offer at low credit scores.

Wait and improve: For many borrowers with scores in the 580–640 range, the most financially sound decision is to spend six to twelve months focused on credit repair — paying down utilization, resolving collections, building a clean payment history — and then apply for a HELOC from a position of strength. The rate difference between a 620 score and a 700 score is substantial enough over a decade that the waiting period pays for itself many times over.

A Realistic Self-Assessment Checklist

Before applying with bad credit, run through these questions honestly:

Do you have at least 25–30% equity? Below this level with bad credit, approval is very unlikely at any reasonable rate. If equity is below 25%, focus on building it before pursuing a HELOC.

Is your income stable and well-documented? Strong documented income partially compensates for a lower credit score. Variable or undocumented income combined with bad credit makes the application very difficult.

Is your current payment history clean for the past 12 months? If not, wait until you have built that 12-month window.

Are your credit issues explainable by a specific event? Medical hardship, divorce, or a pandemic-related job loss — issues with a clear cause that has since resolved — are viewed more favorably than a pattern of chronic financial mismanagement.

What is the rate you would actually receive? Model the real cost of a high-rate HELOC using our HELOC Payment Calculator. If the rate is 13% or higher, compare it carefully to alternatives before committing.

The Bottom Line

Getting a HELOC with bad credit is possible — particularly with strong equity, stable income, and a credit union relationship — but it comes with real trade-offs in rate, terms, and available credit limit.

The honest advice for most borrowers with credit in the 580–650 range: evaluate whether a few months of focused credit improvement would meaningfully change the rate and terms you qualify for. In many cases it will — and the long-term interest savings justify the wait.

If you genuinely need access to equity now and cannot wait, credit unions are the most likely path to approval with a workable rate. Apply there first. Be honest about your credit history. Bring strong documentation of income and equity.

And model the real numbers before you commit. Use our HELOC Payment Calculator to calculate what a HELOC at your likely rate will actually cost — so you can make the decision with full information rather than hope.