HELOC Closing Costs: What Fees to Expect in 2026

One of the most appealing things about a HELOC is the low cost to get started compared to other home financing options. But “low cost” does not mean free. Opening a HELOC comes with a set of fees that vary by lender, loan size, and your location — and if you do not know what to expect, you can easily be caught off guard at closing.

This guide gives you a complete, no-surprises breakdown of every HELOC fee you may encounter in 2026, what each one covers, what is negotiable, and how to evaluate whether a no-closing-cost HELOC is actually the deal it appears to be.

How Much Do HELOC Closing Costs Typically Cost?

Total HELOC closing costs in 2026 typically range from $200 to $2,000 for most borrowers. In some cases — particularly for large credit lines in states with higher recording fees and mandatory attorney involvement — costs can reach $3,500 or more.

This is significantly less than a cash-out refinance, which routinely costs $3,000 to $6,000 or more in closing costs, or a full mortgage refinance that can run even higher. It is one of the key financial advantages of a HELOC over refinancing when the goal is accessing home equity.

Here is a quick summary of all potential HELOC fees before we break each one down:

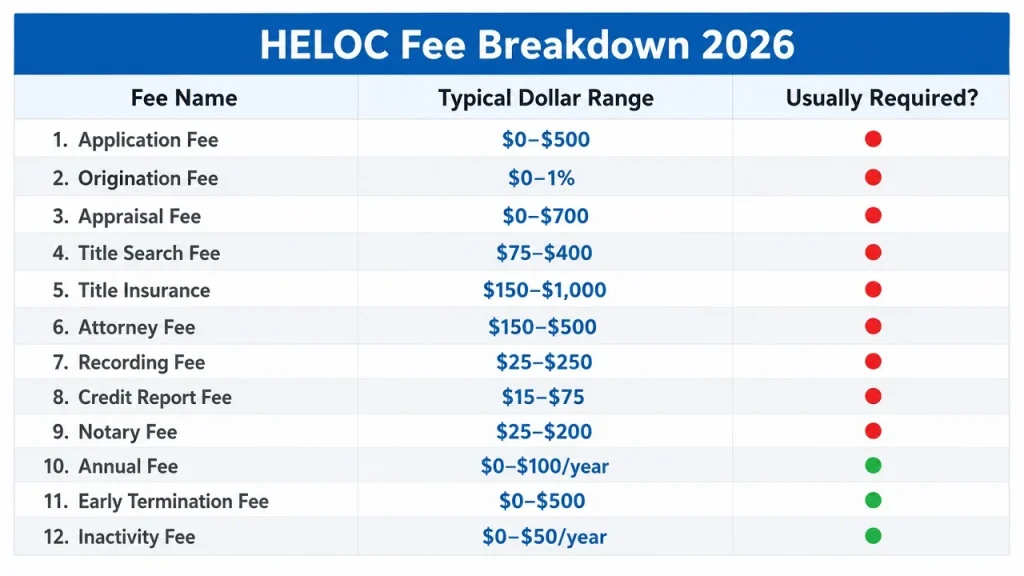

| Fee Type | Typical Range | Required? |

|---|---|---|

| Application fee | $0 – $500 | Sometimes |

| Origination fee | $0 – 1% of credit limit | Sometimes |

| Appraisal fee | $0 – $700 | Usually |

| Title search fee | $75 – $400 | Usually |

| Title insurance | $150 – $1,000 | Sometimes |

| Attorney fee | $150 – $500 | State dependent |

| Recording fee | $25 – $250 | Usually |

| Credit report fee | $15 – $75 | Usually |

| Notary fee | $25 – $200 | Sometimes |

| Annual fee | $0 – $100/year | Sometimes |

| Early termination fee | $0 – $500 | Sometimes |

| Inactivity fee | $0 – $50/year | Rare |

Not every borrower pays every fee on this list. The fees you encounter depend on your lender, your state, and the size of your credit line. Let us walk through each one in detail.

Breaking Down Every HELOC Fee

Application Fee

Typical range: $0 – $500

Some lenders charge an upfront application fee to cover the cost of processing your HELOC request — pulling your credit, reviewing your financials, and beginning the underwriting process. Many lenders, particularly credit unions and online lenders, charge no application fee at all.

If a lender charges an application fee, ask whether it is refundable if your application is denied or if you decide not to proceed. Some lenders apply it toward closing costs if you move forward; others keep it regardless of outcome.

Negotiable? Yes — particularly at smaller banks and credit unions. If you are an existing customer with a strong relationship, application fees are often waived.

Origination Fee

Typical range: $0 – 1% of your credit limit

The origination fee covers the lender’s cost of processing and underwriting your HELOC. It is typically expressed as a percentage of your approved credit limit rather than a flat dollar amount.

On a $100,000 HELOC, a 1% origination fee equals $1,000. On a $50,000 HELOC, it equals $500.

Many major banks — including Wells Fargo, Bank of America, and Chase — have moved toward no-origination-fee HELOCs in recent years to stay competitive, particularly for existing customers. Smaller community banks and mortgage companies are more likely to charge this fee.

Negotiable? Yes, especially if you have strong credit (720+), a large credit line, or existing accounts with the lender. Always ask.

Appraisal Fee

Typical range: $0 – $700

Your lender needs to verify your home’s current market value to determine how much equity you have and how large a credit line you qualify for. This typically requires a formal appraisal by a licensed appraiser.

The appraisal fee depends on your property type, size, and location. A standard single-family home in most markets runs $300–$500. Larger properties, rural locations, or complex homes (multi-family, unusual construction) can push the fee to $600–$700 or more.

Many lenders now use automated valuation models (AVMs) — computer-generated estimates based on comparable sales data — for HELOCs with lower loan-to-value ratios and straightforward properties. AVMs cost the lender far less and that savings is often passed to you as a waived or reduced appraisal fee.

Some lenders offer a drive-by appraisal or desktop appraisal as a middle ground — less thorough than a full interior appraisal but more accurate than a pure AVM. These typically cost $150–$300.

Negotiable? The fee itself is set by the appraiser, not the lender. However, if the lender uses an AVM or desktop appraisal for your property, you may pay nothing.

Title Search Fee

Typical range: $75 – $400

Before placing a lien on your property, your lender needs to confirm that you legally own the home and that no other undisclosed claims or liens exist against it. A title search reviews public property records to verify ownership history and identify any issues.

Title search fees vary significantly by state and county. States with large urban markets and complex ownership histories tend to have higher fees. Rural areas and simpler ownership chains are typically lower.

Negotiable? Limited. This fee goes to a third-party title company, not the lender. However, in some states you have the right to choose your own title company, which allows you to shop for a better price.

Title Insurance

Typical range: $150 – $1,000

Some lenders require a lender’s title insurance policy on a HELOC, which protects the lender (not you) if a title defect is discovered after closing. Unlike title search fees, title insurance is a one-time premium rather than a recurring cost.

Title insurance is more commonly required on larger HELOC credit lines and is more likely to be required by banks and mortgage companies than by credit unions. Many lenders waive title insurance on HELOCs below $100,000 or for borrowers with straightforward property histories.

Note that this is separate from owner’s title insurance, which protects you as the homeowner. You likely already purchased owner’s title insurance when you originally bought the home — it does not need to be repurchased for a HELOC.

Attorney Fee

Typical range: $150 – $500

Several states — including Connecticut, Delaware, Georgia, Massachusetts, New York, North Carolina, South Carolina, and West Virginia — require attorney involvement in real estate closings, including HELOCs. If you live in one of these states, an attorney fee is unavoidable.

In states where attorney involvement is optional, some lenders still use closing attorneys for larger or more complex HELOCs. The fee covers the attorney’s time to review documents, oversee the closing, and ensure the lien is properly recorded.

Negotiable? In states where it is not legally required, yes — you can ask whether a notary signing can replace a full attorney closing for straightforward cases.

Recording Fee

Typical range: $25 – $250

When your HELOC closes, the lender’s lien against your property is recorded with your county recorder’s office as a public document. The recording fee covers this government filing.

Recording fees are set by state and county governments, not by your lender, so they are not negotiable. The fee varies significantly by location — some counties charge a flat fee, others charge per page of documents recorded.

Credit Report Fee

Typical range: $15 – $75

Your lender pulls a tri-merge credit report (from all three major bureaus — Equifax, Experian, and TransUnion) as part of the underwriting process. The fee covers the cost of obtaining this report.

This is one of the smallest fees in the process and is rarely waived. Some lenders absorb it as a cost of doing business; others pass it through directly.

Notary Fee

Typical range: $25 – $200

If your closing does not require an attorney, a notary public may be used to witness and authenticate your signature on closing documents. Many lenders now offer remote online notarization (RON), which allows you to complete the notarization via video call — particularly convenient if you cannot attend an in-person closing.

Notary fees are typically at the low end of the closing cost spectrum and are sometimes waived by lenders who use digital closing platforms.

Ongoing HELOC Fees to Watch For

Beyond the one-time closing costs, several recurring fees can add to your total HELOC cost over time. These are often buried in the fine print of your loan agreement and overlooked at closing.

Annual Fee

Typical range: $0 – $100/year

Some lenders charge a flat annual fee simply for maintaining your HELOC — regardless of whether you have a balance or have drawn any funds. This fee is common among larger banks and is less common at credit unions.

On a 10-year draw period, a $75 annual fee adds $750 to your total HELOC cost. It is a small number in isolation but worth factoring in when comparing lenders — particularly if you are considering keeping your HELOC open with a zero balance as a financial safety net.

Many lenders waive the annual fee for the first year as a promotional incentive. Confirm whether the waiver is permanent or temporary.

Negotiable? Sometimes. Existing customers with multiple accounts at the same institution can often negotiate annual fee waivers.

Early Termination Fee

Typical range: $0 – $500

If you close your HELOC within the first 2–3 years — by either paying it off and requesting closure or refinancing into a different product — many lenders charge an early termination fee. This fee recoups the cost of waived closing costs or reduced-rate promotions the lender offered to win your business.

The early termination period and fee amount vary by lender. Common structures include:

- $300–$500 flat fee if closed within 24 months

- $200–$350 flat fee if closed within 36 months

- No fee after the early termination window expires

Critically, this fee is triggered by closing the account — not by paying off the balance. You can pay your HELOC balance to zero and leave the account open without triggering the fee. This is usually the smart move if you are within the early termination window.

Always read your loan agreement to understand exactly when and how this fee applies.

Inactivity Fee

Typical range: $0 – $50/year

A small number of lenders charge an inactivity fee if you maintain a HELOC with a zero balance and make no draws for an extended period — typically 12 months or more. The logic is that the lender is reserving capital against your credit line whether you use it or not.

Inactivity fees are uncommon at major banks but appear occasionally at smaller institutions. If you plan to keep your HELOC open as a safety net with a zero balance, specifically ask whether an inactivity fee applies.

No-Closing-Cost HELOCs: Are They Really Free?

Many lenders — including large national banks — advertise no-closing-cost HELOCs. The appeal is obvious: access to a credit line with none of the upfront fees described above.

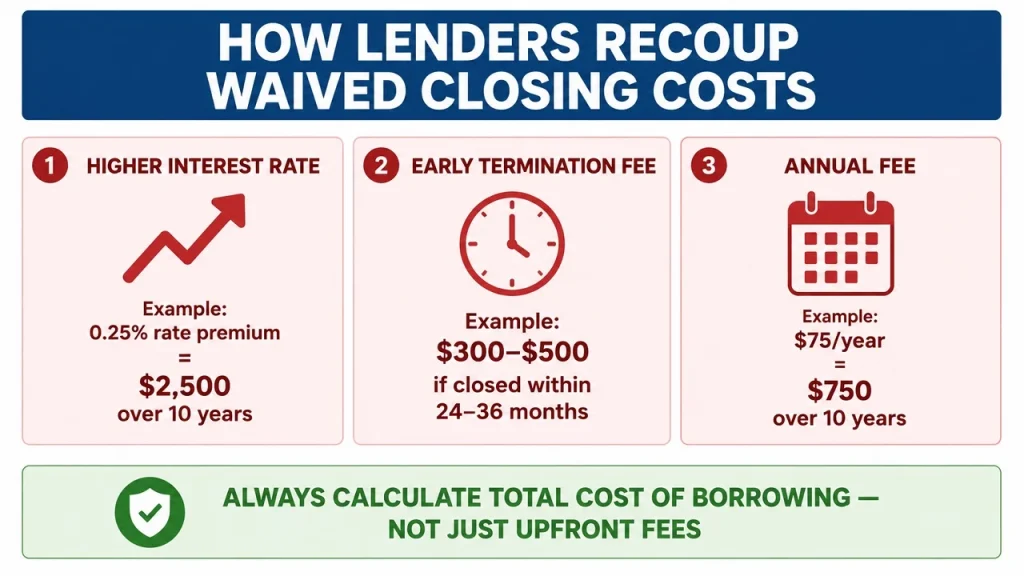

But nothing is actually free. Lenders who waive closing costs typically recoup those costs in one of three ways:

1. A slightly higher interest rate — Even a 0.25% rate premium on a $100,000 HELOC costs $250/year in additional interest. Over a 10-year draw period, that is $2,500 — more than most closing costs in the first place.

2. An early termination fee — Lenders who waive closing costs almost always impose an early termination fee if you close within 2–3 years, which is their insurance against losing money on customers who close quickly after receiving the fee waiver.

3. An annual fee — Some no-closing-cost HELOCs come with an annual maintenance fee that adds up over the life of the line.

When a no-closing-cost HELOC makes sense:

- You plan to keep the HELOC open for many years (the rate premium costs less than upfront fees if you hold it long enough — or it breaks even)

- You have limited cash available at closing

- You are comparing lenders and the no-closing-cost option has a competitive rate

When it does not make sense:

- You plan to pay off and close the HELOC quickly — the early termination fee erases the benefit

- The rate premium is larger than 0.25–0.375% compared to the standard-cost option

Always calculate the total cost of borrowing — not just upfront fees — when comparing a no-closing-cost HELOC against a standard one. Use our HELOC Payment Calculator to model the difference in total interest between two rate scenarios over your expected draw period.

HELOC Closing Costs vs. Other Home Equity Products

How does a HELOC compare to alternative ways of accessing home equity?

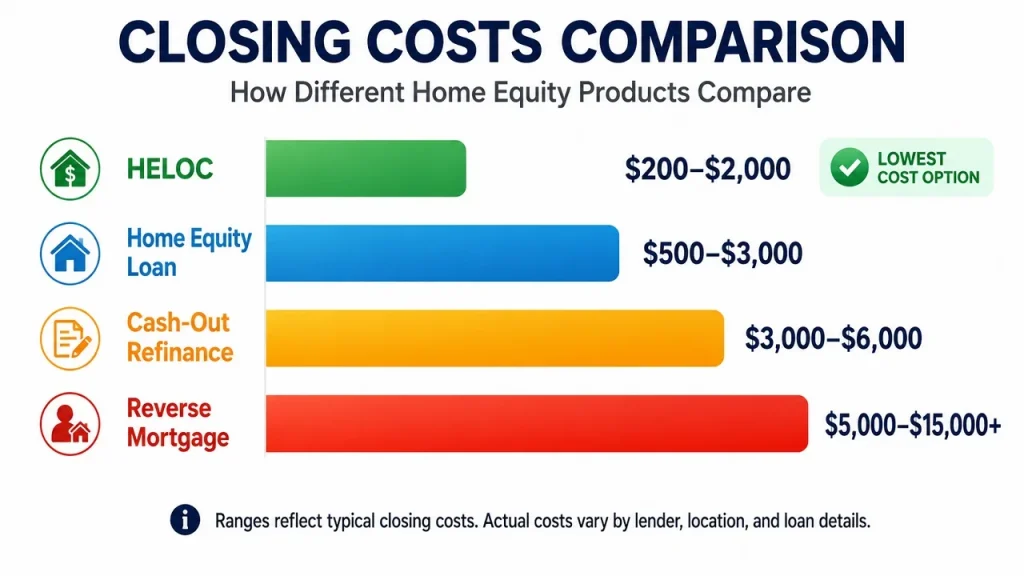

| Product | Typical Closing Costs | Rate Type | Best For |

|---|---|---|---|

| HELOC | $200 – $2,000 | Variable | Flexible, ongoing access |

| Home equity loan | $500 – $3,000 | Fixed | One-time lump sum need |

| Cash-out refinance | $3,000 – $6,000+ | Fixed or variable | Large amounts, rate improvement |

| Reverse mortgage | $5,000 – $15,000+ | Variable | Seniors 62+, no monthly payment |

A HELOC has the lowest closing costs of any home equity product. The gap versus a cash-out refinance is particularly significant — a homeowner accessing $75,000 in equity through a HELOC might pay $500–$1,200 in closing costs versus $4,000–$6,000 for a cash-out refinance on the same home.

This cost advantage makes a HELOC the right tool for most homeowners who need flexible access to equity without the expense of a full refinance.

How to Minimize Your HELOC Closing Costs

Here are practical steps to reduce what you pay to open a HELOC:

Shop at least three lenders. Closing costs vary significantly between institutions. Get a Loan Estimate from at least three lenders — a large bank, a credit union, and an online lender — and compare both rates and fees side by side.

Start with your existing bank or credit union. Existing customers frequently receive fee waivers on application fees, origination fees, and annual fees as a loyalty benefit. Your current mortgage lender is a natural first call.

Ask specifically what is waivable. Lenders rarely volunteer this information. Ask directly: “Which fees can be reduced or waived for a customer in my situation?” The answer may surprise you.

Consider a credit union. Credit unions are member-owned nonprofits and consistently offer lower fees and more competitive rates than large commercial banks on home equity products. If you are not already a member of a credit union, many have broad membership eligibility requirements.

Time your application strategically. Some lenders run promotional periods — particularly in spring and early summer when home equity borrowing picks up — with reduced or waived closing costs. It is worth asking whether any promotions are currently available.

Negotiate the annual fee. If the lender charges an annual fee, ask to have it waived, particularly if you are bringing significant assets or multiple accounts to the relationship.

What to Bring to Your HELOC Closing

When your HELOC is approved and ready to close, you will typically need:

- A government-issued photo ID

- Proof of homeowner’s insurance (your declarations page)

- Your most recent mortgage statement

- Any additional documents requested during underwriting (pay stubs, tax returns, bank statements)

- A cashier’s check or wire transfer authorization for closing costs, if not rolling them into the loan

Many lenders now offer e-closing — fully digital document signing with remote online notarization — which eliminates the need for an in-person appointment. If convenience matters to you, ask your lender whether e-closing is available.

The Bottom Line

HELOC closing costs are real but manageable. Most borrowers pay between $200 and $2,000 to open a line of credit — a fraction of what a cash-out refinance costs for the same equity access. The key is knowing what every fee covers, which ones are negotiable, and how to evaluate whether a no-closing-cost offer truly saves you money when the full borrowing cost is accounted for.

Before you choose a lender, get written Loan Estimates from at least three institutions, compare both the upfront fees and the interest rate, and calculate the total cost of borrowing over your expected draw period.

Use our HELOC Payment Calculator to model the total interest cost at different rates — so you can see exactly whether waiving closing costs in exchange for a higher rate saves or costs you money over your specific timeline.