Is HELOC Interest Tax Deductible in 2026?

Whether your HELOC interest is tax deductible in 2026 depends on one thing above everything else: what you used the money for.

This surprises many homeowners. The assumption is that HELOC interest is automatically deductible — after all, it is mortgage-related debt secured by your home. But the IRS does not care where the debt is secured. It cares where the money went.

Use your HELOC to renovate your home and the interest is likely deductible. Use it to pay off credit cards or take a vacation and it is not — even though the debt sits on the same loan secured by the same house.

This article explains the current IRS rules in plain English, which uses qualify, which do not, how to calculate your actual tax savings, and what you need to document to claim the deduction without trouble.

What the Law Currently Says

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly changed the rules around home equity interest deductibility. Before 2018, HELOC interest was generally deductible regardless of how the funds were used, up to $100,000 in loan balance. The TCJA eliminated that blanket deductibility.

Under the rules currently in effect through at least the end of 2025 — and extended through 2026 under current legislative status — HELOC interest is deductible only when the funds are used to buy, build, or substantially improve the home that secures the loan.

The IRS codified this in Publication 936 and clarified it further in Notice 2018-32. The key language from the IRS guidance:

The deduction applies to interest on a home equity loan or line of credit that is used to buy, build, or substantially improve the taxpayer’s home that secures the loan. Interest on home equity debt used for any other purpose is not deductible as mortgage interest.

This is the rule in 2026. It is simple to state but creates significant complexity in practice — particularly for borrowers who used HELOC funds for multiple purposes.

The Qualifying Test: What Counts as “Buy, Build, or Substantially Improve”

The IRS phrase “buy, build, or substantially improve” is more specific than it sounds. Here is what qualifies and what does not.

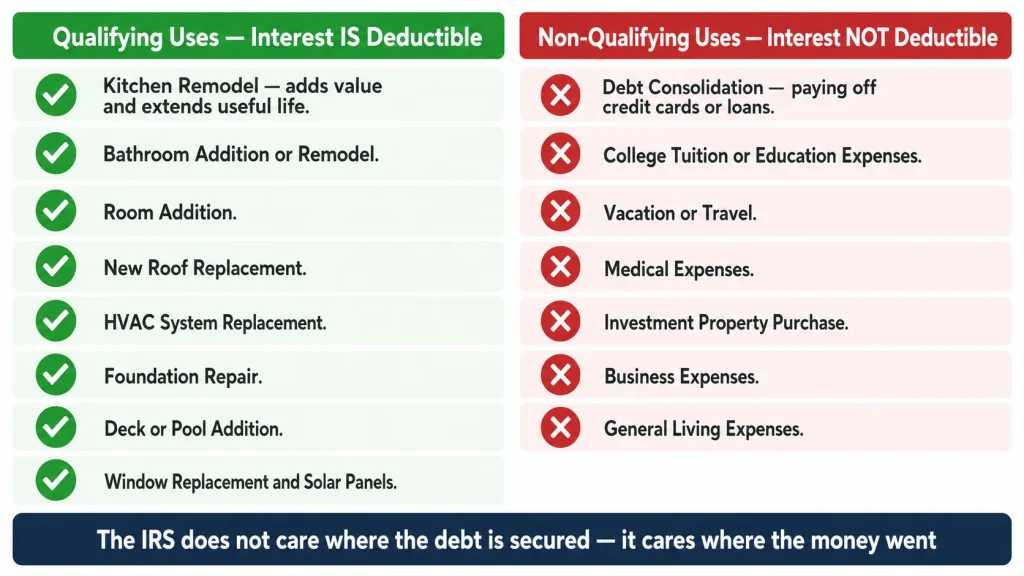

Qualifying Uses (Interest IS Deductible)

Home purchase: If you used a HELOC as part of the purchase of your primary or secondary residence — for example, as a bridge loan or to cover a down payment shortfall — the interest qualifies.

New construction: Interest on a HELOC funding the construction of your home qualifies, provided the home is completed and becomes your residence.

Substantial home improvements: This is the most common qualifying use. Improvements that add value, prolong the home’s useful life, or adapt it to new uses qualify. Specific examples the IRS has historically accepted:

- Kitchen remodel

- Bathroom addition or remodel

- Room addition

- New roof

- HVAC system replacement

- Foundation repair

- Swimming pool or deck addition

- Basement finishing

- Window replacement

- Solar panel installation

The “substantial” qualifier matters. Routine maintenance and repairs — painting a room, replacing a faucet, fixing a broken window — do not qualify as substantial improvements. The improvement must add value or extend the property’s useful life, not merely maintain its current condition.

Non-Qualifying Uses (Interest is NOT Deductible)

Debt consolidation: Using HELOC funds to pay off credit cards, personal loans, auto loans, or any other consumer debt. This is explicitly non-qualifying under current IRS rules — one of the most common misconceptions among HELOC borrowers.

Education expenses: College tuition, student loan payoffs, education-related spending. Non-qualifying.

Vacation or travel: Non-qualifying.

Medical expenses: Non-qualifying as mortgage interest (though medical expenses have their own separate deduction with different rules).

Investment property purchase: Using HELOC funds to buy a separate investment property does not qualify for the home mortgage interest deduction. It may qualify as investment interest or rental expense — a different deduction with different limitations — but not as mortgage interest on Schedule A.

Business expenses: Non-qualifying as mortgage interest (may qualify as business interest in a different schedule).

General living expenses: Non-qualifying.

The Mixed-Use Problem: When You Used Funds for Multiple Purposes

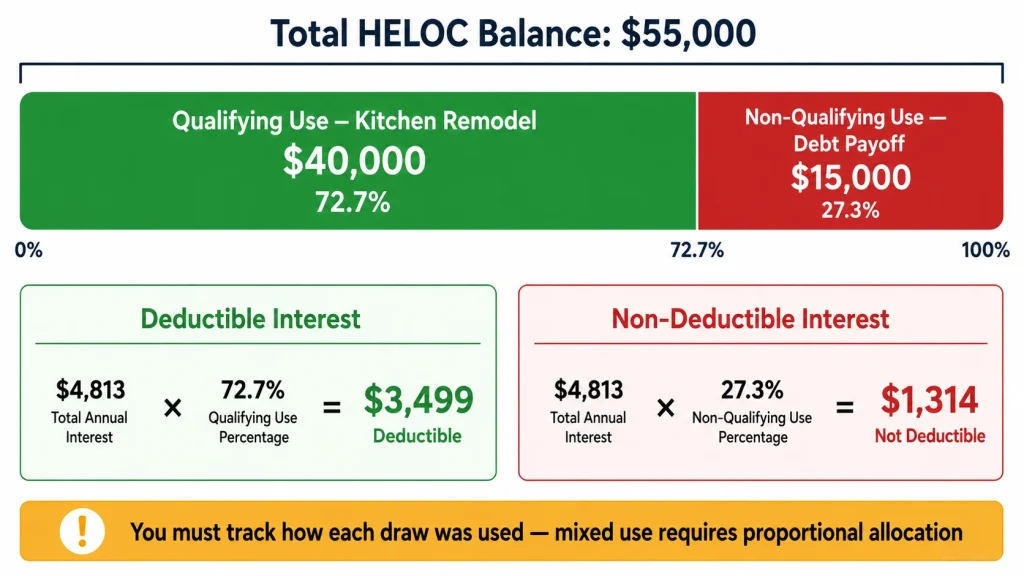

Many HELOC borrowers use their credit line for more than one purpose. You might draw $40,000 for a kitchen remodel and later draw an additional $15,000 to pay off a personal loan. The total balance is $55,000, but only $40,000 was used for a qualifying purpose.

In this situation, you cannot deduct all of your HELOC interest. You must allocate the interest between qualifying and non-qualifying use based on the proportion of each.

Example:

Total HELOC balance: $55,000 Qualifying use (kitchen remodel): $40,000 — 72.7% of balance Non-qualifying use (debt payoff): $15,000 — 27.3% of balance

Annual HELOC interest at 8.75%: $4,813 Deductible portion (72.7%): $3,499 Non-deductible portion (27.3%): $1,314

You can only deduct the $3,499 in interest attributable to the qualifying home improvement use.

The IRS tracing rules require you to track how each draw was used. This is why meticulous record-keeping from the first day of your HELOC is important — particularly if you anticipate drawing funds for both home improvement and non-qualifying purposes.

The Loan Limit: $750,000 Cap

Even when HELOC funds are used for qualifying purposes, the deduction is subject to a dollar cap on the underlying debt.

You can only deduct interest on home acquisition and improvement debt up to $750,000 for joint filers ($375,000 for married filing separately). This limit applies to the combined total of your primary mortgage plus any qualifying HELOC balance — not to each separately.

Example:

Primary mortgage balance: $580,000 Qualifying HELOC balance: $80,000 Combined debt: $660,000

Since $660,000 is below the $750,000 cap, all of the HELOC interest on the qualifying balance is deductible.

Example where the cap applies:

Primary mortgage balance: $700,000 Qualifying HELOC balance: $80,000 Combined debt: $780,000

The $780,000 combined balance exceeds the $750,000 cap by $30,000. You can only deduct interest on $750,000 of the combined debt. The deductible HELOC interest is proportionally reduced.

For most homeowners with mortgages below $600,000, this cap does not limit the HELOC deduction. For borrowers in high-cost markets with large primary mortgages, it is worth calculating whether the cap applies to your situation.

The Itemizing Requirement: The Other Gate Most Borrowers Miss

This is where many HELOC borrowers discover the deduction is unavailable to them even when their use qualifies.

To claim the HELOC interest deduction, you must itemize deductions on Schedule A of your federal tax return. You cannot take both the standard deduction and the HELOC interest deduction — it is one or the other.

The TCJA nearly doubled the standard deduction, which now stands at:

- $29,200 for married filing jointly (2026, inflation-adjusted)

- $14,600 for single filers (2026)

- $21,900 for head of household (2026)

For the HELOC interest deduction to be worth claiming, your total itemized deductions — mortgage interest, HELOC interest, state and local taxes (capped at $10,000), charitable contributions, and other qualifying deductions — must exceed your standard deduction.

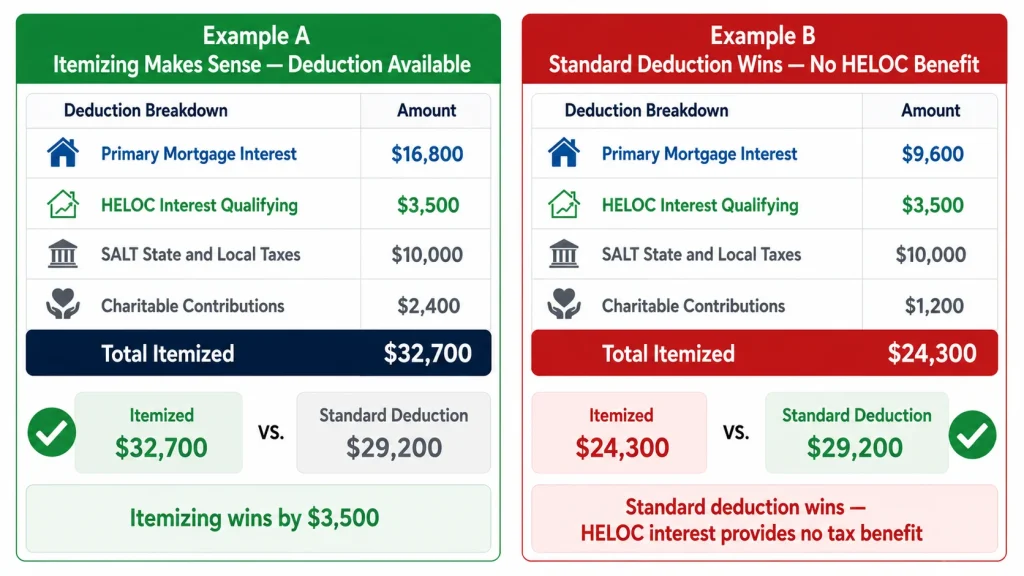

Example for a married couple:

Itemized deductions:

- Primary mortgage interest: $16,800

- HELOC interest (qualifying): $3,500

- State and local taxes (SALT cap): $10,000

- Charitable contributions: $2,400

- Total itemized: $32,700

Standard deduction: $29,200

Since $32,700 exceeds $29,200, itemizing produces a larger deduction by $3,500. The HELOC interest deduction is available and worth claiming.

Example where itemizing does not help:

Same couple but with a smaller mortgage:

- Primary mortgage interest: $9,600

- HELOC interest (qualifying): $3,500

- SALT: $10,000

- Charitable: $1,200

- Total itemized: $24,300

Since $24,300 is below the $29,200 standard deduction, this couple is better off taking the standard deduction. The HELOC interest deduction produces no tax benefit for them — even though their use of funds qualifies.

The majority of American homeowners take the standard deduction. For many, the HELOC interest deduction is technically available but practically irrelevant because their total itemized deductions do not exceed the standard deduction threshold.

What the Deduction Is Actually Worth: Real Dollar Examples

For borrowers who do itemize, the actual tax savings from the HELOC interest deduction depends on their federal tax bracket.

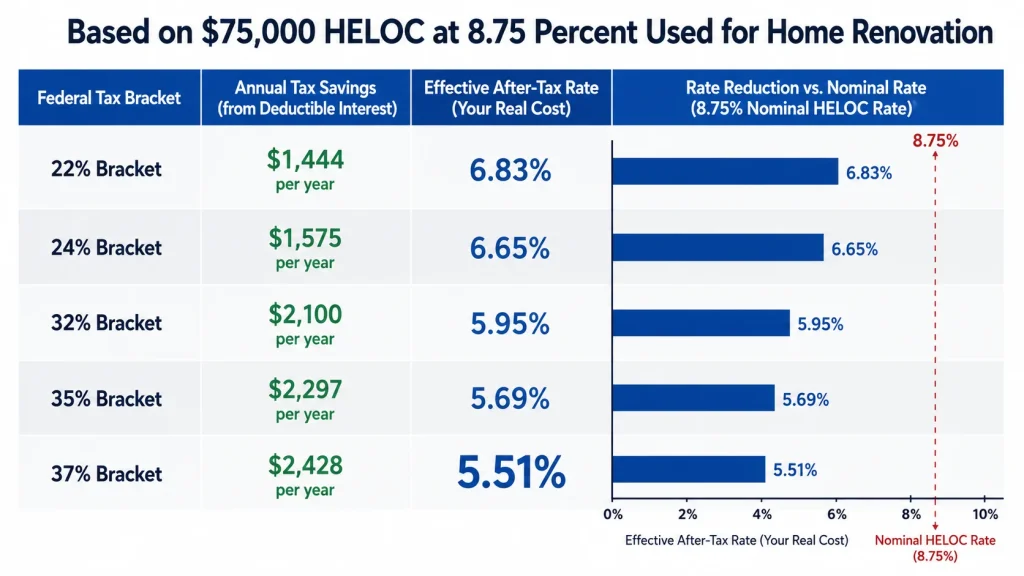

Here is what the deduction is worth at common bracket levels on a $75,000 HELOC balance used for home renovation at 8.75%:

Annual HELOC interest: $6,563

| Tax Bracket | Tax Savings | Effective After-Tax Rate |

|---|---|---|

| 22% | $1,444 | 6.83% |

| 24% | $1,575 | 6.65% |

| 32% | $2,100 | 5.95% |

| 35% | $2,297 | 5.69% |

| 37% | $2,428 | 5.51% |

For a homeowner in the 32% bracket using their HELOC for home renovation, the after-tax effective rate drops to 5.95% — meaningfully below the nominal 8.75% rate. That is a genuine financial advantage worth accounting for in your borrowing decision.

For a homeowner in the 22% bracket who does not itemize, the effective rate is simply 8.75% — no adjustment.

The Second Home Rule

The HELOC interest deduction applies to debt on your primary residence or one secondary residence. If you have a vacation home or second property that you use personally (not as a rental), a HELOC secured by that property and used to substantially improve it may also qualify for the deduction — subject to the same $750,000 combined limit across all qualifying properties.

This means a homeowner could potentially deduct interest on:

- HELOC on primary home used for home improvement, AND

- HELOC on vacation home used for vacation home improvement

Both are potentially deductible, subject to the combined $750,000 debt limit.

A HELOC on a rental property used to improve that rental property is treated differently — as a rental expense on Schedule E, not as mortgage interest on Schedule A.

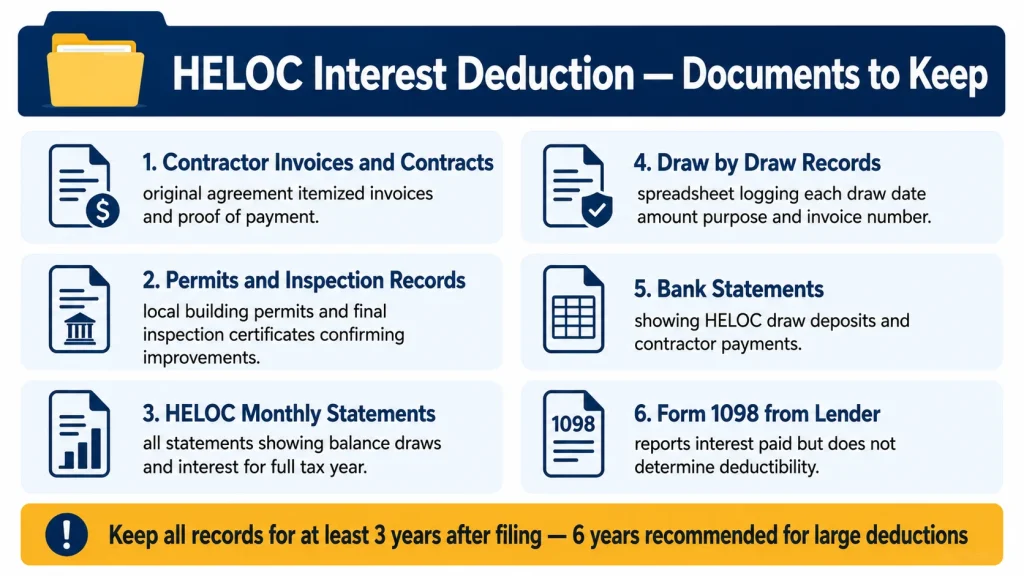

Record-Keeping: What You Need to Document

If you plan to claim the HELOC interest deduction, maintaining proper documentation is essential. The IRS can disallow the deduction if you cannot demonstrate that the funds were used for qualifying purposes.

What to keep:

Contractor invoices and contracts: For every home improvement project funded by HELOC draws, maintain the original contractor agreement, itemized invoices, and proof of payment (bank statements showing the payment clearing).

Permits and inspection records: Local building permits and final inspection certificates confirm that improvements were made and document their scope.

HELOC statements: Keep all monthly statements showing your balance, draws, and interest charges for the full tax year.

Draw-by-draw records: A simple spreadsheet logging each HELOC draw — date, amount, purpose, and corresponding invoice — is the most useful document if you ever need to substantiate the deduction.

Bank statements: Showing the HELOC draw deposits and corresponding payments to contractors, suppliers, or vendors.

The IRS statute of limitations on tax returns is generally three years from filing — meaning you should retain records for at least three years after you claim the deduction. If the deduction is substantial, keeping records for six years is a more conservative and safer approach.

Frequently Asked Questions

If I used my HELOC for home renovation in 2024 but am filing in 2026, is the interest deductible? Yes — the deductibility of HELOC interest is determined by the tax year in which the interest was paid, not when the renovation occurred. Interest paid in tax year 2024 is claimed on your 2024 return; interest paid in 2025 on your 2025 return; and so on.

My lender sends me a Form 1098 for my HELOC interest. Does that mean it’s deductible? Not automatically. Lenders are required to report HELOC interest on Form 1098 regardless of how the funds were used. The form reports what was paid — not whether it qualifies for deduction. The qualification depends on the use of funds, which you determine and document independently of what appears on the 1098.

Can I deduct HELOC interest if I use the funds for a rental property I own? The interest may be deductible as a rental expense on Schedule E — but not as mortgage interest on Schedule A. These are different deductions with different rules and different limitations. Consult a tax advisor for your specific situation.

What if the TCJA rules expire after 2025? The TCJA provisions were set to expire at the end of 2025. As of mid-2026, Congress has extended the key provisions including the mortgage interest deduction rules as part of the broader tax package. The rules described in this article reflect the current law. Tax law can change — confirm current rules with a tax advisor each year.

Does my state also allow HELOC interest deduction? State tax treatment of HELOC interest varies. Many states conform to federal rules, but some have their own rules. California, for instance, has decoupled from some federal TCJA provisions. Check your state’s specific rules or ask a tax advisor familiar with your state.

Can I deduct HELOC interest if I work from home and use part of the renovation for a home office? The home office deduction has its own separate rules. A portion of home improvement costs may be allocable to the home office if the improvement affects the office space — but this is complex and the interaction with the HELOC interest deduction requires careful professional guidance.

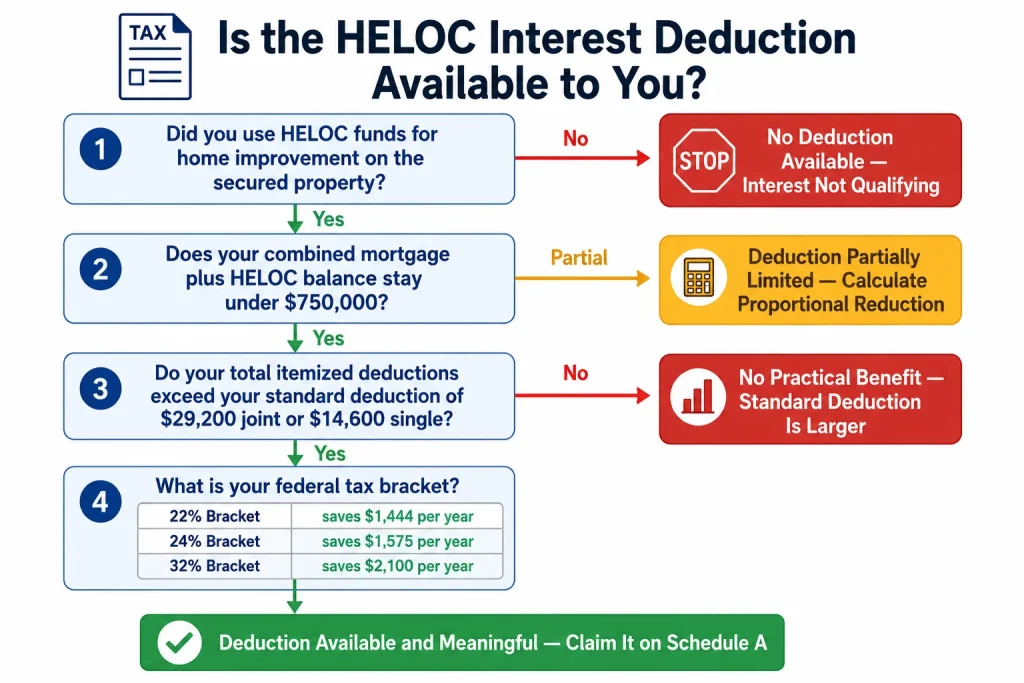

A Practical Decision Guide: Is the Deduction Available to You?

Work through these four questions to determine whether the HELOC interest deduction is available and meaningful for your situation.

Question 1: What did you use the HELOC funds for? Home improvement on the secured property → potentially qualifying. Debt payoff, education, vacations, or other consumer use → not qualifying. Stop here — no deduction available.

Question 2: Does the combined mortgage + HELOC balance stay under $750,000? Yes → proceed. No → deduction is partially limited. Calculate the proportional reduction.

Question 3: Do you itemize deductions? Your total itemized deductions exceed your standard deduction → proceed. Standard deduction is larger → no practical benefit from HELOC interest deduction even if use qualifies.

Question 4: What is your tax bracket? Calculate your actual dollar savings: Annual HELOC interest × your tax bracket = annual tax saving. That savings divided by 12 = monthly after-tax rate reduction.

If the answer to all four questions produces a meaningful tax saving — proceed with confidence that the deduction is available. If any question produces a stop or a significant limitation, revise your calculation accordingly.

The Bottom Line

HELOC interest is tax deductible in 2026 — but only when the funds were used to buy, build, or substantially improve the home securing the loan, and only when you itemize deductions and your total itemized deductions exceed your standard deduction.

For most homeowners using a HELOC for home renovation who have significant mortgage interest and state and local taxes, the deduction is real and produces a meaningful after-tax rate reduction — effectively lowering the cost of borrowing by 1 to 3 percentage points depending on your tax bracket.

For homeowners who used their HELOC for debt consolidation, education, or other non-home purposes, the interest is not deductible regardless of how the loan is secured.

The three most important practical takeaways:

- Track how every HELOC draw is used from day one — mixed-use borrowing requires proportional allocation

- Confirm whether you itemize before assuming the deduction is available

- Consult a CPA or tax advisor who knows your full picture before filing — the interaction between mortgage interest, SALT limits, HELOC interest, and the standard deduction is more nuanced than any single rule suggests

Use our HELOC Payment Calculator to see your annual interest cost — then apply your tax bracket to calculate your actual after-tax rate if you qualify for the deduction.