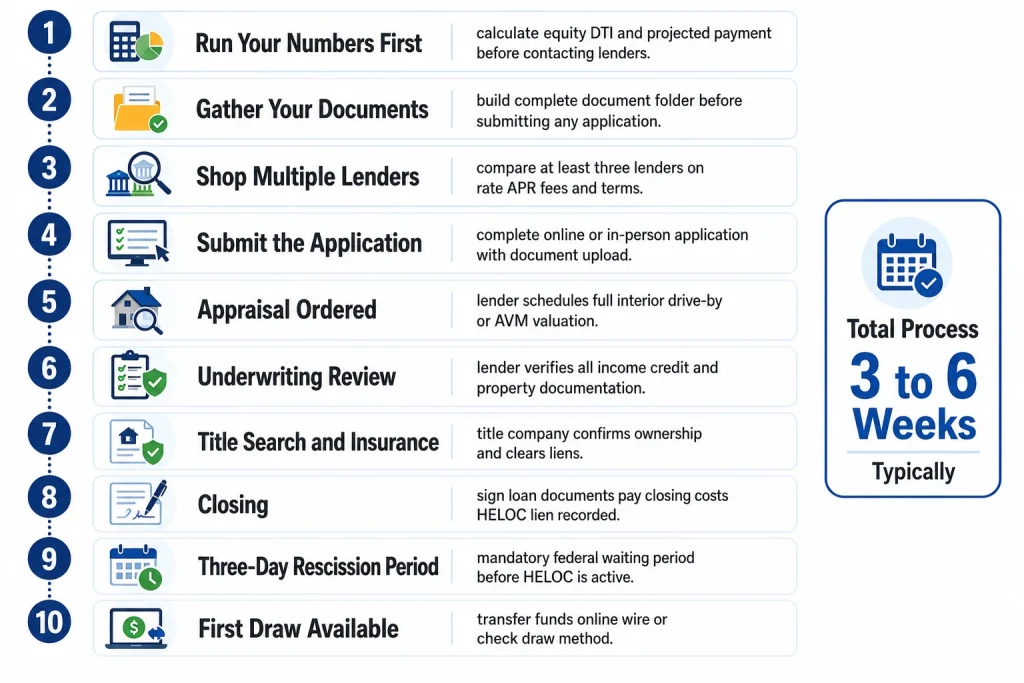

How to Apply for a HELOC: Step-by-Step Process

Applying for a HELOC is more involved than opening a credit card but less complicated than getting a full mortgage. Most borrowers who go in prepared — documents gathered, lenders compared, numbers already run — find the process straightforward. The ones who struggle are usually those who show up underprepared and get surprised at the document request or the appraisal value.

This guide walks you through every step from deciding you want a HELOC to making your first draw — what happens at each stage, what you need to provide, and where the process commonly stalls.

Step 1: Run Your Numbers Before You Talk to Anyone

Before contacting a single lender, spend an hour getting clear on your financial position. You are going to be asked these questions anyway — better to know the answers before the conversation starts.

Calculate your estimated equity and maximum HELOC:

Find your home’s approximate current value — a recent comparable sale in your neighborhood, a real estate site estimate, or a quick call to a local agent gives you a reasonable starting point. Then pull your most recent mortgage statement for the exact current balance.

Estimated max HELOC = (Home Value × 0.85) − Mortgage Balance

If that number is close to what you need, you are likely in good shape. If it is significantly less than you need, know that going in — either the project scope needs adjustment or you need to wait for more equity.

Pull your own credit report:

You can pull your own reports without affecting your score at AnnualCreditReport.com. Check all three bureaus — Equifax, Experian, TransUnion — and look for errors, old collections, or anything that would surprise a lender. Dispute any errors before applying. Errors take 30 to 45 days to resolve and you want that behind you.

Calculate your DTI:

Add up every monthly debt payment that appears on your credit report — mortgage, car payments, student loans, minimum credit card payments. Divide by your gross monthly income. If the result plus the projected HELOC minimum payment is above 43%, the application may be difficult. Know this before you apply, not during underwriting.

Use the HELOC Payment Calculator:

Model your expected draw amount at current rates to see what your interest-only payment will be during the draw period and what your fully amortized payment will be when repayment begins. Our HELOC Payment Calculator lets you run both numbers instantly. If either payment is uncomfortably high for your budget, that is a signal to adjust the amount before applying.

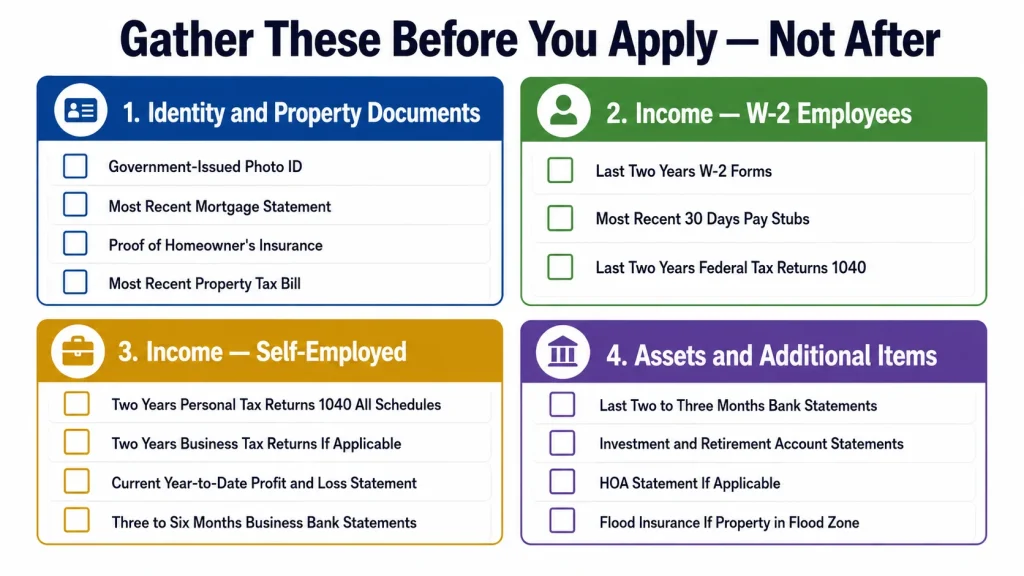

Step 2: Gather Your Documents

Nothing slows a HELOC application down like missing documents. Lenders have specific requirements and they will not move forward until the file is complete. Getting everything together before you submit the application — rather than providing documents one at a time over two weeks — can cut several days off the approval timeline.

Standard documents for most applications:

Identity and property:

- Government-issued photo ID (driver’s license or passport)

- Most recent mortgage statement showing current balance

- Proof of homeowner’s insurance (declarations page)

- Most recent property tax bill or payment confirmation

Income — W-2 employees:

- Last two years of W-2 forms

- Most recent 30 days of pay stubs (most recent two pay stubs if paid biweekly)

- Last two years of federal tax returns (1040) — required by most lenders even for W-2 employees

Income — self-employed:

- Last two years of personal federal tax returns (1040) with all schedules

- Last two years of business tax returns (if applicable — S-corp, partnership, or LLC)

- Current year-to-date profit and loss statement (may be required)

- Three to six months of business bank statements

Assets:

- Last two to three months of bank statements (checking and savings)

- Last two to three months of investment and retirement account statements

Additional items some lenders require:

- HOA statement if the property is in a homeowners association

- Copy of current homeowner’s insurance policy

- Flood insurance documentation if the property is in a flood zone

- Divorce decree or separation agreement if applicable to income or property ownership

Create a folder — digital or physical — with all of these before you submit your first application. When a lender asks for a document, you want to be able to provide it the same day.

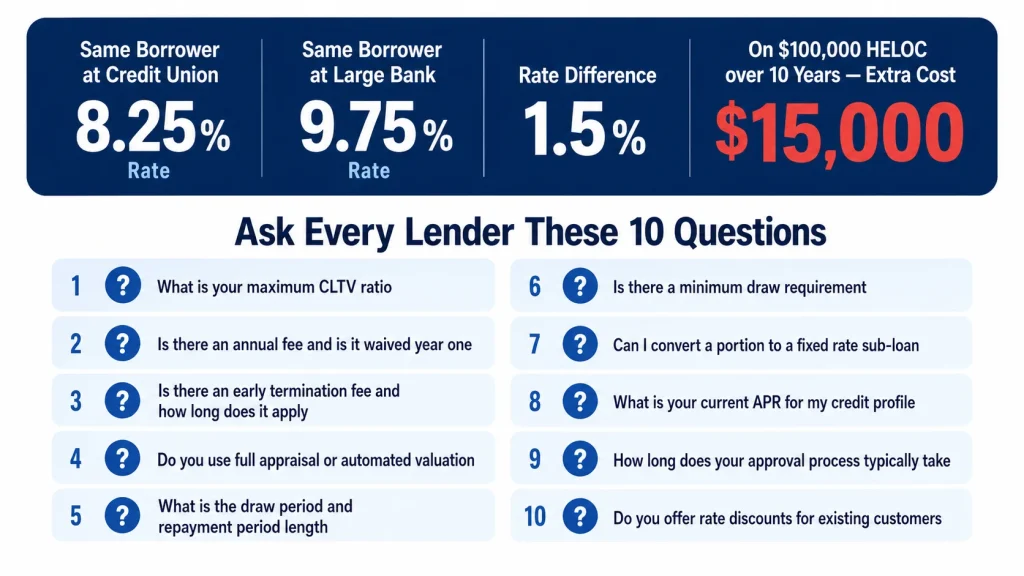

Step 3: Shop Multiple Lenders — This Step Is Worth Real Money

Most borrowers contact one or two lenders. The ones who contact three to five get meaningfully better outcomes — both on rate and on terms.

HELOC rates, fees, and credit limits vary more across lenders than most borrowers expect. The same borrower profile might receive an 8.25% rate at a credit union and a 9.75% rate at a large bank. On a $100,000 HELOC over 10 years, that 1.5-point difference is $15,000 in interest.

Where to look:

Your existing bank or mortgage lender. Start here not because they will have the best rate, but because they already know you. Existing customers often receive fee waivers and sometimes modest rate discounts. It is also the fastest application since they have your account history.

Credit unions. Consistently offer competitive HELOC rates and are more willing to work with borrowers who do not fit neatly into a large bank’s automated underwriting box. If you are not a member of a credit union, check eligibility — many have broadened their membership criteria and joining takes 15 minutes.

Online lenders. Figure, Spring EQ, and Aven have fully digital processes, often close faster than traditional lenders, and offer competitive rates for qualified borrowers. They tend to use automated property valuations which speeds things up considerably.

Community banks and regional lenders. Worth a call for non-standard properties or situations where you want a human underwriter reviewing your file rather than an algorithm.

What to compare:

Do not just compare interest rates. The annual percentage rate (APR) accounts for fees and gives a better apples-to-apples comparison. Beyond APR, ask each lender:

- What is your maximum CLTV?

- Is there an annual fee? Is it waived the first year?

- Is there an early termination fee? How long does it apply?

- Do you use a full appraisal or automated valuation?

- What is the draw period length and repayment period length?

- Is there a minimum draw requirement?

- Can I convert a portion to a fixed-rate sub-loan?

Getting answers to these questions from multiple lenders takes two to three hours total. It is time worth spending.

Step 4: Submit the Application

Once you have chosen a lender, the formal application begins. Most lenders now offer online applications that take 30 to 45 minutes to complete. Some still prefer in-person or phone applications — particularly community banks and credit unions.

What the application covers:

- Personal information (name, address, Social Security number)

- Employment information and income

- Property information (address, estimated value, existing liens)

- Desired credit line amount

- Purpose of the HELOC (some lenders ask)

- Authorization to pull your credit

When you submit the application, the lender will run a hard credit inquiry. This typically drops your score by 3 to 5 points temporarily — a minor and short-lived effect. If you are applying to multiple lenders within a short window (14 to 45 days depending on the scoring model), most credit scoring models treat multiple HELOC inquiries as a single event for score purposes. Apply to all your target lenders within the same two-week window to minimize the credit impact.

After submission:

Within a few days, the lender will issue a Loan Estimate — a standardized three-page document showing the proposed terms, rate, estimated payments, and closing costs. Review this carefully. If the rate or fees differ significantly from what you discussed, ask for clarification before proceeding.

Step 5: The Appraisal

After the application is submitted and the credit review is complete, the lender orders an appraisal of your property. This is the step that often takes the most time and occasionally produces surprises.

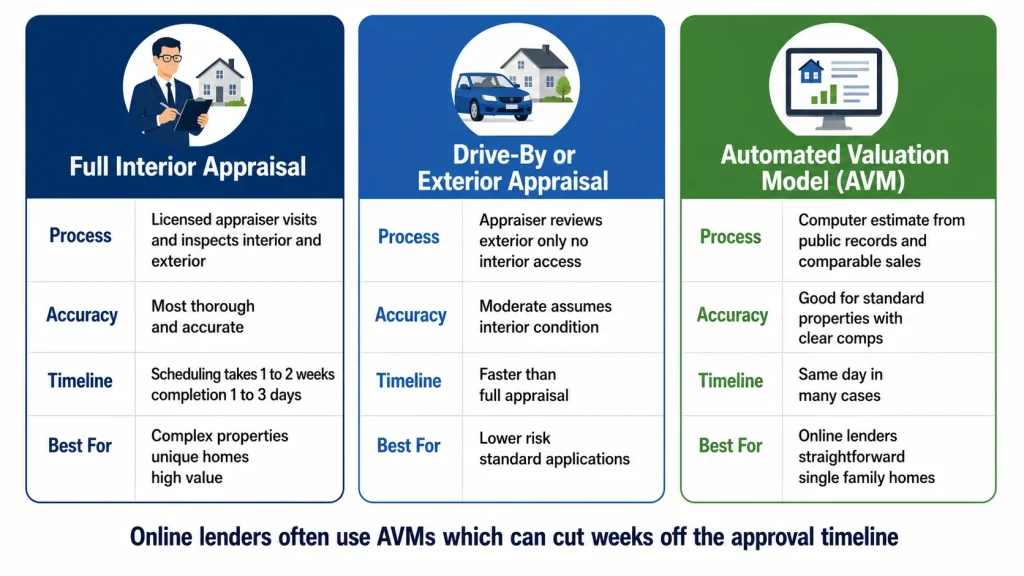

Types of appraisals:

Full interior appraisal: A licensed appraiser visits your home, inspects the interior and exterior, measures the square footage, reviews comparable sales in your neighborhood, and produces a formal appraisal report. Most thorough but takes the most time — scheduling alone can take one to two weeks in busy markets.

Drive-by or exterior appraisal: The appraiser reviews the exterior only without entering the home. Faster and cheaper than a full appraisal, used for lower-risk applications where the lender has high confidence in the value.

Automated Valuation Model (AVM): A computer-generated estimate based on public records, recent comparable sales, and property characteristics. No appraiser visits the property. Many online HELOC lenders use AVMs for straightforward single-family homes with clear comparable sales data. Fastest option — sometimes completed same day.

What to do before the appraiser arrives:

If you are getting a full interior appraisal, a few hours of preparation can make a difference. This is not about staging the home for a sale — appraisers are trained to see past cosmetics. But addressing obvious deferred maintenance, making sure all rooms are accessible, and cleaning up the exterior improves the presentation and supports the highest defensible value.

Fix obvious issues: broken windows, leaking fixtures, visible water damage, holes in walls. These are not just cosmetic — they can be flagged as condition issues that lead to a lower valuation or required repairs.

If the appraisal comes in lower than expected:

A low appraisal reduces your available equity and therefore your maximum HELOC credit limit. Your options:

- Accept the lower credit line if it still meets your needs

- Request a reconsideration of value (ROV) if you believe comparable sales were missed or incorrectly analyzed — provide specific comps to support your position

- Get a second appraisal at a different lender

- Wait for market appreciation and reapply later

Step 6: Underwriting

Once the appraisal is complete, the file moves to underwriting. The underwriter reviews all the documentation — income, credit, appraisal, title, insurance — and makes the approval decision.

Most borrowers have limited visibility into this stage. You submitted your documents weeks ago and now you wait. The most important thing you can do during underwriting is respond immediately to any conditions or additional document requests.

Conditional approval is common and not alarming. It means the underwriter has reviewed the file and is prepared to approve but needs one or more additional items — a letter explaining a gap in employment, documentation of a large deposit, clarification of a tax return item. Respond within 24 hours when possible. Files that sit waiting for borrower responses are the ones that fall behind.

Do not make significant financial changes during underwriting. Do not open new credit accounts, make large purchases on credit, change jobs, or make unusually large deposits or withdrawals from your bank accounts. Any of these can trigger additional requests, re-underwriting, or in serious cases, denial.

Step 7: Title Search and Insurance

Before closing, the lender orders a title search to confirm you legally own the property and that no undisclosed liens or claims exist against it. This is typically handled by a title company and takes five to ten business days.

In some states, an attorney must perform the title search and oversee closing. Your lender will tell you if this applies in your state.

If the title search reveals any issues — an old lien from a prior contractor, a boundary dispute, an unreleased lien from a previous owner — these must be resolved before closing. Title issues are uncommon on properties that have been owned for several years without unusual circumstances, but they do occur and can delay closing by weeks if not addressed promptly.

Step 8: Closing

When underwriting is complete and the title is clear, your lender schedules the closing. This is where you sign the loan documents and the HELOC becomes official.

What happens at closing:

You sign a package of documents including the HELOC agreement, the deed of trust or mortgage (which places the lender’s lien on your property), the Truth in Lending disclosure, and several other standard documents. The signing typically takes 30 to 60 minutes.

Closing may happen:

- At a title company or attorney’s office

- At the lender’s branch

- At your home (mobile notary)

- Remotely via electronic signing and remote online notarization (RON) — increasingly available and convenient

Closing costs are paid at closing — either by check, wire transfer, or rolled into the loan balance if the lender permits. Review the final Closing Disclosure (which you receive at least three business days before closing) against the Loan Estimate you received when you applied. Any significant differences should be questioned.

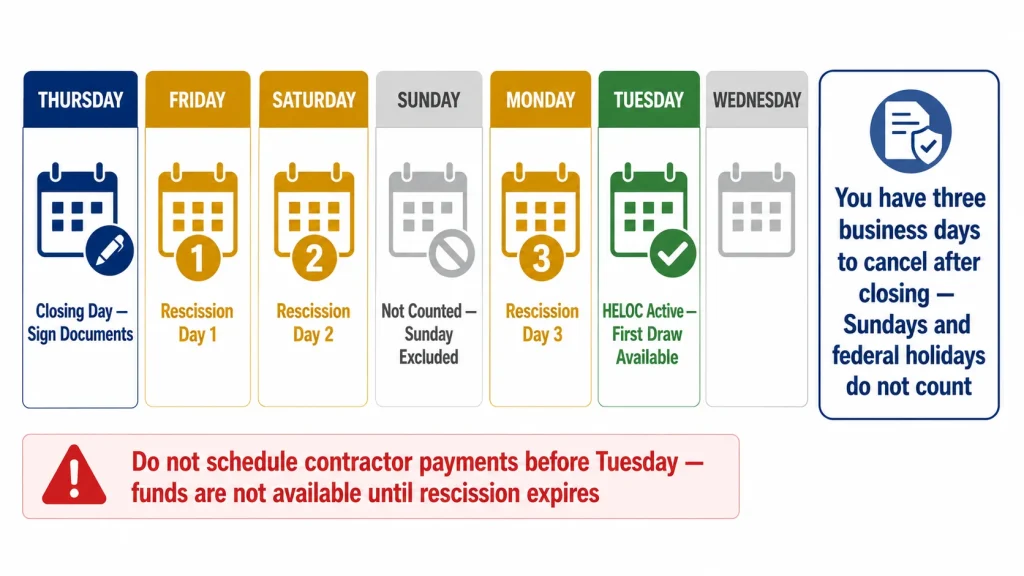

Step 9: The Three-Day Right of Rescission

Federal law requires a mandatory three-business-day waiting period after closing before a HELOC on your primary residence becomes effective. This is the right of rescission — you have three business days to cancel the HELOC without penalty if you change your mind.

The three days do not include Sundays or federal holidays. If you close on a Thursday, your rescission period expires Sunday night and your HELOC is live on Monday.

During these three days, the lender cannot disburse any funds. Do not schedule draws or contractor deposits that require funds before the rescission period expires.

Note: The right of rescission applies to HELOCs on primary residences. Second homes and investment properties do not have the three-day rescission requirement.

Step 10: Making Your First Draw

Once the rescission period expires, your HELOC is active and you can begin drawing funds.

How to draw funds:

Most lenders offer multiple draw methods:

- Online or mobile app transfer to a linked bank account (1 to 2 business days)

- Wire transfer (same day or next business day, fee usually $15–$30)

- HELOC checks (if provided by your lender — deposit or use like a personal check)

- Direct payment to a contractor (some lenders offer this)

A few practical notes on your first draw:

Test the draw process with a small amount first — $500 to $1,000 — to confirm the transfer works and understand the timing before you need a large draw for a contractor payment. Finding out the transfer takes two days instead of one is better learned on a test draw than when a $25,000 contractor deposit is due tomorrow.

Keep a simple log of every draw: date, amount, purpose, and balance. This documentation matters for tax purposes if any portion of your draws are used for home improvement (potentially deductible) versus other uses (not deductible).

Confirm your interest rate and first payment due date with the lender. Your first minimum payment is typically due 30 days after your first draw.

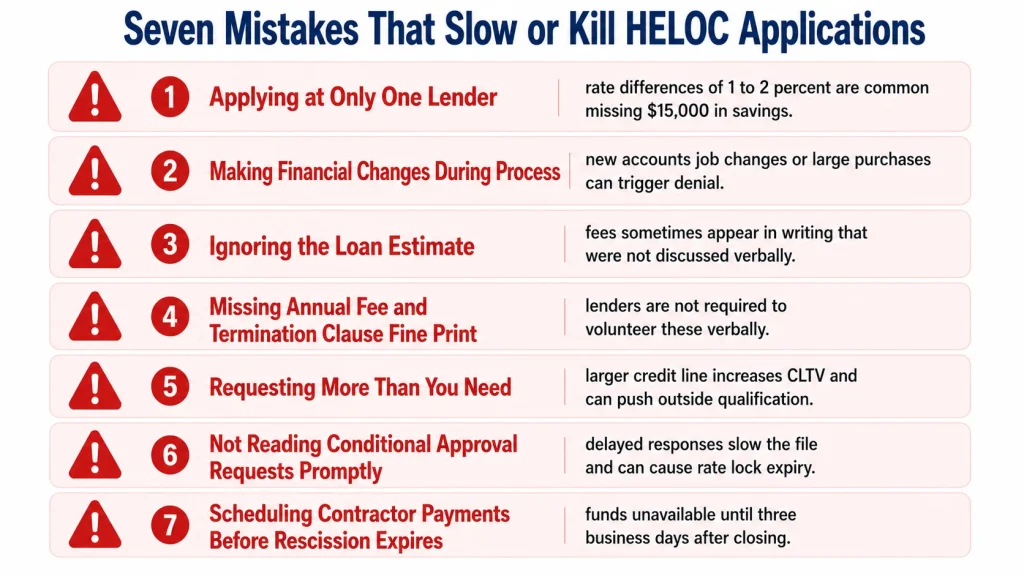

Common Application Mistakes to Avoid

Applying at only one lender. Rate differences of 1 to 2 percent are common across lenders for the same borrower. Always compare at least three.

Making financial changes during the process. Job changes, large purchases, new credit accounts — all of these can trigger re-underwriting or denial. Keep your financial life stable from application submission through closing.

Ignoring the Loan Estimate. Review every line. Fees that were not discussed verbally sometimes appear in writing. If something does not match what you were told, ask before signing.

Not reading the loan agreement for annual fees and early termination clauses. These details are in the fine print and lenders are not required to volunteer them verbally.

Requesting a credit line larger than you need. A larger credit line increases your CLTV ratio and can push you outside a lender’s qualification parameters. Apply for what you actually need, not the maximum available.

Forgetting about the three-day rescission period when scheduling contractor work. Promising a contractor a payment on day two post-closing when funds are not yet available creates unnecessary stress.

The Bottom Line

A HELOC application is a process, not a transaction. It takes three to six weeks from start to funded, requires real documentation, and involves an appraisal that can produce surprises. None of that is a reason to avoid it — the lower interest rate compared to most alternatives is worth the process for meaningful borrowing amounts.

The borrowers who get through it smoothly are the ones who prepared: ran their numbers first, gathered documents before applying, shopped multiple lenders, and responded quickly at every stage when the lender asked for something.

Use our HELOC Payment Calculator before you apply — knowing your projected payment before the lender runs your file puts you in control of the conversation from the first call.