HELOC for Debt Consolidation: Does It Make Sense?

Using a HELOC to consolidate high-interest debt is one of the most financially impactful moves available to a homeowner — and one of the most dangerous if executed without discipline.

The math is genuinely compelling. Rolling $50,000 of credit card debt at 23% APR into a HELOC at 8.75% cuts your annual interest cost from $11,500 to $4,375 — a $7,125 annual saving on the same balance. Over five years of repayment, that gap compounds into $30,000 or more in interest savings.

But the math only tells half the story. The other half is behavioral, and it is where debt consolidation most often fails. This article gives you both halves — the financial case for using a HELOC to consolidate debt and the honest risk assessment that determines whether it is the right move for your specific situation.

How HELOC Debt Consolidation Works

The mechanics are straightforward. You open a HELOC secured by your home equity, draw funds from the credit line, and use those funds to pay off your existing high-interest debts — credit cards, personal loans, auto loans, medical bills, or any combination.

You then owe the consolidated balance on your HELOC instead of across multiple accounts. You make a single monthly payment to one lender at the HELOC’s variable interest rate — typically 8.25% to 10.50% in 2026 — instead of minimum payments spread across multiple high-rate accounts.

The HELOC’s interest rate is lower because it is secured by your home. That security transfers the risk from the lender to you — which is the core of the risk analysis that follows.

The Financial Case: Real Dollar Savings

Let us look at three realistic debt consolidation scenarios to put actual numbers behind the concept.

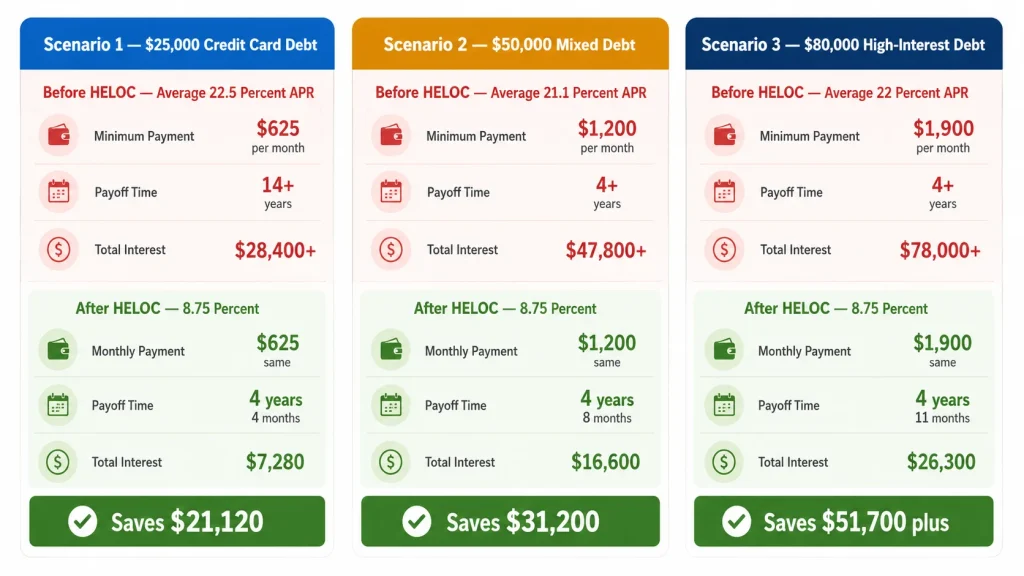

Scenario 1: $25,000 in Credit Card Debt

Before consolidation:

- Total balance: $25,000 across three credit cards

- Average APR: 22.5%

- Minimum payments: approximately $625/month

- Time to pay off at minimum payments: 14+ years

- Total interest at minimum payments: $28,400+

After consolidating to HELOC at 8.75%, paying $625/month:

- Monthly payment: $625 (same as before)

- Time to pay off: 4 years 4 months

- Total interest paid: $7,280

- Interest saved: $21,120

- Time saved: 10+ years

Scenario 2: $50,000 Mixed Debt (Credit Cards + Personal Loan)

Before consolidation:

- Credit cards: $35,000 at 23.99% APR

- Personal loan: $15,000 at 14.5%

- Combined minimum payments: approximately $1,200/month

- Weighted average rate: 21.1%

- Total interest if paid minimum: $47,800+

After consolidating to HELOC at 8.75%, paying $1,200/month:

- Monthly payment: $1,200 (same as before)

- Time to pay off: 4 years 8 months

- Total interest paid: $16,600

- Interest saved: $31,200

- Time saved: Dramatically accelerated

Scenario 3: $80,000 High-Interest Debt

Before consolidation:

- Credit cards: $55,000 at 24.99% APR

- Personal loans: $25,000 at 16.5%

- Combined minimum payments: approximately $1,900/month

- Total interest over remaining term: $78,000+

After consolidating to HELOC at 8.75%, paying $1,900/month:

- Monthly payment: $1,900 (same as before)

- Time to pay off: 4 years 11 months

- Total interest paid: $26,300

- Interest saved: $51,700+

Summary Table

| Debt Amount | High-Rate Interest | HELOC Interest (8.75%) | Total Saved |

|---|---|---|---|

| $25,000 | $28,400 | $7,280 | $21,120 |

| $50,000 | $47,800 | $16,600 | $31,200 |

| $80,000 | $78,000 | $26,300 | $51,700 |

These are not marginal improvements. The interest savings from HELOC debt consolidation are frequently larger than the original debt amount — particularly for borrowers who have been making minimum payments on high-rate cards for years.

Use our HELOC Payment Calculator to calculate exactly what your consolidated balance would cost on a HELOC versus what you are currently paying.

The Core Risk: You Are Pledging Your Home

Before anything else, this risk must be stated plainly and taken seriously.

Credit card debt, personal loan debt, and medical debt are unsecured. If you stop paying, your creditors can damage your credit and pursue legal collection actions. But they cannot take your home.

HELOC debt is secured by your home. If you stop paying, your lender can foreclose. You can lose your house.

When you consolidate unsecured debt into a HELOC, you are not eliminating the debt — you are moving it from a position where your home is safe to a position where your home is collateral. This is a meaningful change in your financial risk profile that deserves more than a sentence in the fine print.

For most financially stable borrowers with consistent income, this trade is rational — you get a dramatically lower rate in exchange for accepting a risk that you are confident you can manage. But the trade is real, and it should be made consciously.

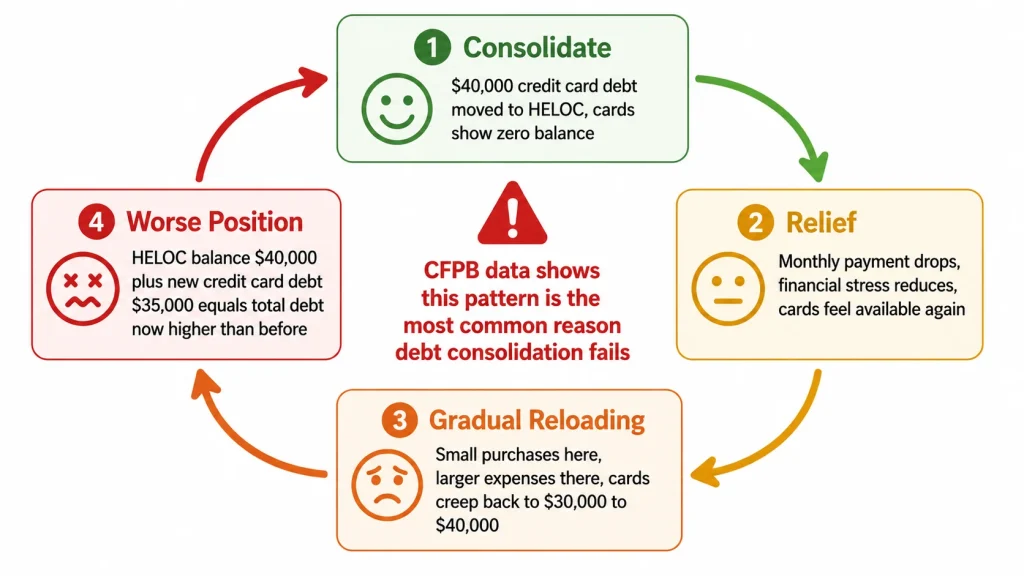

The Behavioral Risk: The Reloading Problem

This is the most common reason HELOC debt consolidation fails — and it is purely behavioral, not financial.

The pattern: You consolidate $40,000 in credit card debt into your HELOC. Your credit cards now show zero balances. You feel financial relief — legitimately, because your monthly interest cost has dropped by hundreds of dollars. Over the next 18 to 24 months, you gradually use the cards again — small purchases here, a larger expense there — until the card balances have crept back up to $30,000 or $40,000.

Now you have both a $40,000 HELOC balance and a $30,000–$40,000 credit card balance. Your total debt has increased. Your home is pledged as collateral. Your financial situation is worse than before consolidation.

This is not a rare failure mode. The Consumer Financial Protection Bureau (CFPB) and financial counseling organizations consistently report this pattern in borrowers who consolidate without addressing the underlying spending behavior that created the debt.

The question you must answer honestly before consolidating:

What created this debt? Was it a specific one-time event — job loss, medical crisis, divorce — that has been resolved and is unlikely to recur? Or was it chronic overspending relative to income — lifestyle inflation, discretionary purchases regularly exceeding what your income can sustain?

If the answer is the first, consolidation makes strong sense. The problem that caused the debt is gone; consolidation simply cleans up the financial wreckage at a lower cost.

If the answer is the second, consolidation without behavioral change will produce the reloading problem. The lower HELOC payment creates headroom in your budget that gets filled with new spending, and the credit cards reload while the HELOC balance remains.

How to Assess Whether You Are a Good Candidate

Run through these six questions honestly. The answers determine whether HELOC debt consolidation is a sound move for your specific situation.

1. Do you have sufficient home equity?

You need at least 15–20% equity remaining after the HELOC is added. On a $400,000 home with a $280,000 mortgage and $50,000 in debt to consolidate: $400,000 × 85% = $340,000 maximum combined debt $340,000 − $280,000 (existing mortgage) = $60,000 maximum HELOC

You have enough equity to consolidate the $50,000. If your mortgage were $295,000, you could only access $45,000 — not enough to consolidate the full balance.

2. Is your income stable?

HELOC debt requires monthly payments for up to 20+ years. If your income is variable, commission-based, seasonal, or at risk of disruption, the secured nature of a HELOC creates meaningful risk. Stable W-2 income is a stronger foundation for HELOC debt than self-employment or commission income.

3. What caused the debt?

One-time event with no recurrence risk → strong candidate for consolidation. Chronic overspending pattern → consolidation without behavioral change will likely make things worse.

4. Can you commit to not re-using the credit cards post-consolidation?

Not “trying” not to. Not “being careful.” A firm commitment — ideally backed by a concrete plan such as closing the cards, cutting them up, or locking them away — to not re-accumulate the debt you just consolidated.

5. What will your HELOC payment be at repayment, and can you afford it?

Use our HELOC Payment Calculator to calculate the fully amortized repayment payment on your consolidated balance. A $50,000 balance at 8.75% with a 15-year repayment requires $497/month. Can your budget sustain that reliably?

6. Are you approaching the end of your draw period?

Consolidating debt into a HELOC that is already 7 years into a 10-year draw period leaves you only 3 years before payment shock hits. The repayment period jump on a large consolidated balance can be severe. Know where you are in the HELOC lifecycle before adding debt to it.

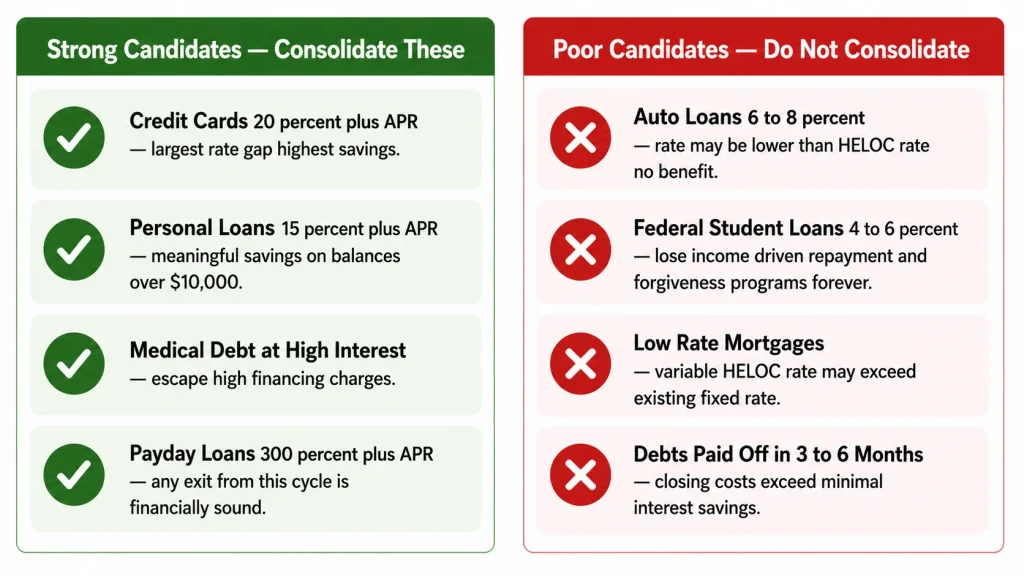

What Debts Make the Most Sense to Consolidate

Not every debt is worth consolidating into a HELOC. The financial case is strongest when the rate differential is large and the balance is substantial.

Strong Candidates for Consolidation

Credit card debt at 20%+ APR: This is the primary use case. The rate gap between credit cards (20–30%) and a HELOC (8–10%) is enormous. Even modest balances produce meaningful savings. Large balances produce transformative savings.

Personal loans at 15%+ APR: A meaningful rate differential. Worth consolidating, particularly for balances above $10,000.

Medical debt at high interest: Some medical financing arrangements carry high rates. If your medical debt is accruing significant interest, consolidation makes financial sense.

Payday loans: Extraordinarily high effective rates — often 300%+ APR when annualized. Any escape from payday loan debt cycles via HELOC consolidation is financially sound. The rate reduction is so dramatic that the math is decisive.

Weaker Candidates for Consolidation

Auto loans at 6%–8%: The rate differential between a 7% auto loan and an 8.75% HELOC is small or even negative. Consolidating a low-rate auto loan into a higher-rate HELOC makes no financial sense.

Student loans at 4%–6%: Federal student loans at low fixed rates should never be consolidated into a HELOC at a higher variable rate. Federal student loans also come with income-driven repayment options, forgiveness programs, and other borrower protections that disappear permanently when you pay them off with HELOC funds.

Mortgage balance: Never roll your existing mortgage into a HELOC unless it is already a high-rate mortgage and you have done the full math. A HELOC has a variable rate that can rise significantly over time.

Debts you are about to pay off anyway: If a credit card balance will be fully paid from savings or income within 3–6 months, consolidating it into a HELOC adds closing cost overhead and process complexity for negligible financial benefit.

The Interest Rate Risk: Variable Rate on a Large Balance

When you consolidate $50,000 to $80,000 of debt into a HELOC, you are taking on a large variable-rate obligation. This is meaningfully different from a small HELOC draw.

A 1% rate increase on $80,000 costs an additional $800 per year in interest — $67/month. A 2% increase costs $1,600/year — $133/month. These are not trivial numbers at larger consolidation balances.

In 2026, with rates having stabilized after the 2022–2024 hiking cycle, the near-term rate risk is more moderate than it was two years ago. But variable rate exposure on a large balance over a 10–15 year repayment period is real risk that deserves honest acknowledgment.

How to manage this risk:

Pay down the consolidated balance as aggressively as your budget allows during the draw period, while the rate is known and your payment is still interest-only. Every dollar of principal you reduce before repayment begins is a dollar that can no longer be affected by rate increases.

Some lenders also allow you to convert a portion of your HELOC balance to a fixed-rate sub-loan — ask your lender whether this option is available if you want to lock in rate certainty on a portion of your consolidated balance.

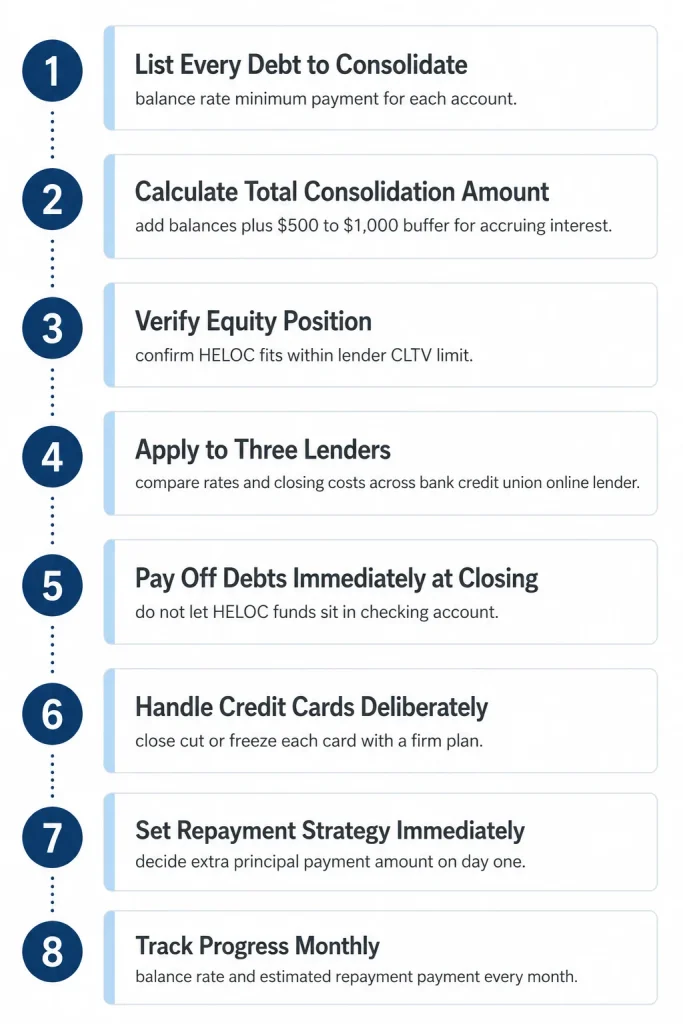

A Step-by-Step Consolidation Plan

If you have decided HELOC debt consolidation makes sense for your situation, here is how to execute it cleanly.

Step 1: List every debt you plan to consolidate Write down each account: balance, interest rate, minimum payment, and whether you are paying it off or keeping it open. Be specific and complete — no rounding, no estimates.

Step 2: Calculate your total consolidation amount Add up the balances you are consolidating. Add a small buffer — $500 to $1,000 — for any interest that accrues between now and the payoff date.

Step 3: Verify your equity position supports the consolidation Use your home’s current value and existing mortgage balance to confirm the HELOC you need falls within your lender’s CLTV limit. If you are not sure of your home’s current value, a licensed appraiser or an automated valuation tool can give you an estimate.

Step 4: Apply for the HELOC Shop at least three lenders — your existing mortgage lender, a credit union, and an online lender. Compare both rates and closing costs. For a debt consolidation HELOC, the rate is particularly important since you will carry a significant balance for an extended period.

Step 5: Pay off the debts immediately at closing Do not let the HELOC funds sit. The day the funds are available, pay off every debt on your list. Do not stage the payoffs or use the funds for anything else first.

Step 6: Handle the credit card question deliberately This is the behavioral fork in the road. For each credit card you pay off, make a conscious decision: close it, keep it open with a zero balance and freeze it, or keep it for specific limited use with a firm spending rule. There is no universally right answer — but there must be a deliberate answer, not a default.

Step 7: Set your repayment strategy immediately The day after consolidation, decide how much you will pay above the interest-only minimum each month. Remember: the minimum payment only covers interest and does not reduce your balance. If you pay only the minimum for the full draw period, you will enter repayment with the same balance you started with — and face payment shock on top of a large balance.

Step 8: Track your progress monthly Review your HELOC balance, interest rate, and estimated repayment payment each month. If your rate has changed, recalculate. If your balance has not moved meaningfully, increase your payment.

Tax Considerations: The Deductibility Question

Under current IRS rules, HELOC interest is deductible only when funds are used to buy, build, or substantially improve the home securing the loan.

Debt consolidation is explicitly not a qualifying use. If you use HELOC funds to pay off credit cards, personal loans, or any other consumer debt, the interest you pay on those funds is not tax deductible — even though the HELOC is secured by your home.

This is a meaningful distinction from using a HELOC for home renovation. A renovation HELOC may produce an effective after-tax rate of 6.65%–6.83%. A debt consolidation HELOC has no tax benefit — its effective rate equals its nominal rate.

The rate advantage over credit cards is still enormous even without deductibility. But do not assume HELOC interest is automatically deductible — for debt consolidation specifically, it is not.

Always confirm with a tax advisor before making any deductibility assumptions.

When HELOC Debt Consolidation Makes Strong Sense

You are a strong candidate for HELOC debt consolidation when all of the following are true:

- You have at least 20%+ equity in your home after accounting for the HELOC

- Your debt was caused by a specific one-time event, not chronic overspending

- You have stable, documented income that will support HELOC payments for years

- Your current debt carries rates of 15%+ — the higher the rate, the stronger the case

- You can commit firmly to not re-accumulating the consolidated debt

- You have a concrete plan for the credit cards post-consolidation

- You have calculated your repayment period payment and your budget can absorb it

When all seven of these conditions are met, HELOC debt consolidation is one of the most financially impactful moves available to a homeowner. The interest savings are real, the payment reduction is real, and the accelerated debt elimination is real.

When It Does Not Make Sense

HELOC debt consolidation is likely a mistake when:

- The debt was caused by ongoing overspending that has not been addressed

- Your income is unstable or at risk

- You do not have a firm plan for the credit cards post-consolidation

- Your debt rates are already relatively low (under 10%)

- You are approaching your draw period end date with a large existing HELOC balance

- Your equity position is tight — less than 20% remaining after the HELOC

- You are considering consolidating federal student loans or a low-rate auto loan

The Bottom Line

HELOC debt consolidation can save tens of thousands of dollars in interest, cut years off your debt repayment timeline, and meaningfully reduce your monthly payment burden. The financial math is not subtle — the rate gap between a HELOC and high-interest consumer debt produces enormous savings over any meaningful repayment period.

The risk is also real. You are pledging your home against debt that was previously unsecured. You are taking on variable rate exposure on a potentially large balance. And you are testing whether your spending behavior has truly changed or whether the freed-up budget headroom will simply reload the cards.

The honest answer to “does it make sense?” is: it depends entirely on you. The math almost always says yes. The behavioral analysis determines whether you will actually follow through on the math’s promise.

Use our HELOC Payment Calculator to run your own consolidation numbers — see exactly what your current debt costs versus what a HELOC would cost at your balance and rate, and use that number to make the decision with full information.