HELOC Payment Shock: What It Is and How to Avoid It

Every year, thousands of American homeowners get blindsided by a sharp, sudden jump in their monthly HELOC payment. Not because they mismanaged their finances. Not because interest rates spiked overnight. But simply because they did not fully understand how a HELOC is structured when they signed for it.

This jump has a name: HELOC payment shock.

If you currently have a HELOC, are considering one, or are approaching the end of your draw period, this is one of the most important things you can read. We will explain exactly what payment shock is, show you the real numbers, and walk through every strategy available to soften or eliminate the impact.

What is HELOC Payment Shock?

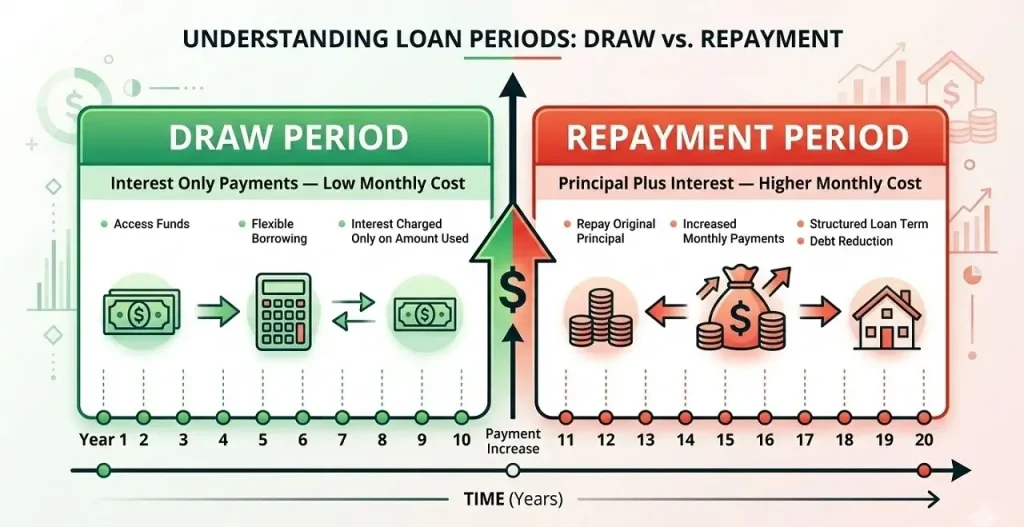

HELOC payment shock is the sudden, significant increase in your monthly payment that occurs when your HELOC transitions from the draw period to the repayment period.

During the draw period — typically the first 5 to 10 years — most lenders only require you to pay interest on your outstanding balance. The principal you borrowed stays untouched. Your monthly payment is relatively low, and many borrowers grow comfortable with it.

Then the draw period ends.

The moment your HELOC enters the repayment period, the rules change completely. You can no longer borrow new funds, and your entire outstanding balance must now be repaid — with interest — over the remaining 10 to 20 years. Your payment jumps from interest-only to fully amortized, meaning every payment now covers both principal and interest.

The result is a payment that can be anywhere from 50% to 100% higher than what you were paying before — sometimes more.

This is payment shock. And for borrowers who are not prepared, it can cause serious financial strain.

The Real Numbers: How Much Can Your Payment Jump?

Let’s move past the theory and look at actual dollar figures. The size of the payment shock depends on three variables: your outstanding balance, your interest rate, and your repayment term.

Here are real examples using common HELOC balances at a 8.75% interest rate — close to where many variable-rate HELOCs sit in 2026.

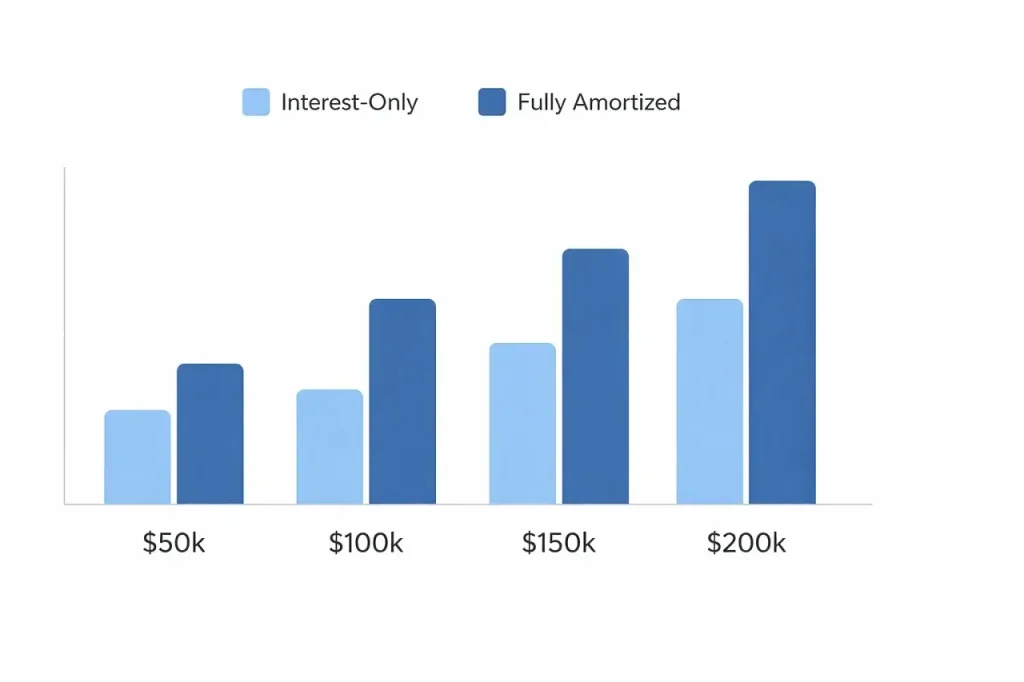

Example 1: $50,000 Balance

| Phase | Payment Type | Monthly Payment |

|---|---|---|

| Draw period | Interest-only | $365 |

| Repayment period (15 years) | Principal + interest | $497 |

| Payment increase | +$132 (+36%) |

Example 2: $100,000 Balance

| Phase | Payment Type | Monthly Payment |

|---|---|---|

| Draw period | Interest-only | $729 |

| Repayment period (15 years) | Principal + interest | $994 |

| Payment increase | +$265 (+36%) |

Example 3: $150,000 Balance

| Phase | Payment Type | Monthly Payment |

|---|---|---|

| Draw period | Interest-only | $1,094 |

| Repayment period (15 years) | Principal + interest | $1,491 |

| Payment increase | +$397 (+36%) |

Example 4: $200,000 Balance

| Phase | Payment Type | Monthly Payment |

|---|---|---|

| Draw period | Interest-only | $1,458 |

| Repayment period (15 years) | Principal + interest | $1,988 |

| Payment increase | +$530 (+36%) |

A $530 per month increase on a $200,000 balance. That is not a rounding error — that is a real budget disruption for most households.

And these examples assume your interest rate stays flat. If your variable rate has climbed during the draw period, the jump could be significantly larger.

Want to calculate your exact payment shock based on your balance and rate? Use our HELOC Payment Calculator to model both phases side by side.

What Makes Payment Shock Worse

Several factors can amplify payment shock beyond the baseline numbers above. Understanding them helps you assess your personal risk level.

1. A Short Repayment Term

The shorter your repayment period, the higher your monthly payment. A 10-year repayment term produces significantly higher payments than a 20-year term on the same balance. Some lenders offer only 10-year repayment, which compresses the amortization and drives payments up fast.

For a $100,000 balance at 8.75%:

- 20-year repayment: $882/month

- 15-year repayment: $994/month

- 10-year repayment: $1,244/month

Always ask your lender what repayment term they offer before you sign.

2. Rising Variable Rates During the Draw Period

If the Federal Reserve raised rates during your draw period — as happened aggressively between 2022 and 2024 — your rate may be meaningfully higher now than when you first opened the line. Higher rate at repayment = larger payment shock.

A borrower who opened a HELOC at 5% and is now entering repayment at 8.75% will face a payment shock roughly double what they anticipated when they originally ran the numbers.

3. A Large Outstanding Balance

This one is obvious but worth stating. The more you drew from your HELOC without paying down principal, the larger the balance sitting there when repayment begins. Borrowers who treated the draw period as interest-only for its full duration — making zero voluntary principal payments — face the steepest shock.

4. A Balloon Payment Structure

Some older HELOCs — particularly those written before 2010 — were structured with a balloon payment rather than a traditional amortization schedule. Instead of gradual monthly repayments, the entire balance became due in a lump sum at the end of the draw period. While less common today, if your HELOC was opened more than 10 years ago, review your original agreement carefully. A balloon payment is the most extreme form of payment shock possible.

6 Strategies to Avoid or Reduce HELOC Payment Shock

The good news: payment shock is entirely preventable if you act before the repayment period begins. Here are the six most effective strategies, ranked from simplest to most involved.

Strategy 1: Start Paying Down Principal During the Draw Period

This is the single most effective thing you can do. You are never required to pay only the minimum interest during the draw period — that is just the floor. If you pay extra principal every month while you still have the flexibility to do so, your balance entering the repayment period will be lower, and your payment shock will be smaller.

Even modest extra payments make a meaningful difference. On a $100,000 HELOC at 8.75%, paying an extra $300/month toward principal during a 10-year draw period reduces your balance at repayment by over $36,000 — cutting your repayment payment by around $358/month.

Use our HELOC Payment Calculator to see exactly how much extra principal payments would reduce your end-of-draw balance.

Strategy 2: Know Your Repayment Date and Plan Ahead

This sounds basic, but a surprising number of HELOC borrowers do not know their exact draw period end date. Find yours. Mark it on your calendar. Set a reminder 12 months before it arrives.

That 12-month window is your preparation time. Use it to build up savings, pay down your balance, or explore refinancing options before the clock runs out.

Strategy 3: Refinance the HELOC Before Repayment Begins

If your balance is large and the projected repayment payment would strain your budget, refinancing is worth exploring. Options include:

Refinancing into a new HELOC — Some lenders will allow you to open a new HELOC to replace the old one, effectively restarting your draw period. This resets the clock and keeps your payments low, but it does not reduce your debt — it delays the inevitable. Use this only if you have a concrete plan to pay down the balance during the new draw period.

Converting to a home equity loan — Rolling your HELOC balance into a fixed-rate home equity loan gives you predictable payments and eliminates variable rate risk. Your payment will still be higher than your interest-only minimum, but you will know exactly what it is every month.

Cash-out refinancing — If you have significant equity and mortgage rates are favorable, a cash-out refinance can absorb your HELOC balance into a new first mortgage. This simplifies your debt into one payment, though closing costs ($3,000–$6,000+) need to factor into the math.

Strategy 4: Make a Lump Sum Principal Payment Before Repayment Starts

If you have savings, a work bonus, a tax refund, or proceeds from selling an asset, applying a lump sum to your HELOC principal before the repayment period starts can dramatically reduce your payment shock.

Paying down $20,000 of a $100,000 HELOC balance before repayment begins reduces your monthly payment by roughly $199/month on a 15-year repayment schedule at 8.75%. That one payment saves you nearly $2,400 per year.

Strategy 5: Ask Your Lender About a Loan Modification

If you are already in repayment and the payment is causing financial hardship, contact your lender directly. Many lenders — including large banks like Wells Fargo, Bank of America, and Chase — have hardship programs that can temporarily reduce payments, extend the repayment term, or modify the loan structure.

This is not a publicized option. You have to ask. Lenders generally prefer modification over default, so if you are genuinely struggling, this conversation is worth having before you miss a payment.

Strategy 6: Budget for the Transition 12 Months Early

If you cannot reduce your balance or refinance in time, the next best move is simply to absorb the higher payment into your budget before it hits. A full year before your draw period ends, start making the projected repayment payment voluntarily. The extra money goes toward principal, further reducing your balance, and you arrive at the repayment period already comfortable with the new payment amount.

It is a psychological and financial reset that makes payment shock feel like a non-event.

How to Calculate Your Own Payment Shock

You do not have to guess what your payment shock will be. Here is the simple math:

Step 1: Find your current HELOC balance (check your latest statement)

Step 2: Find your current interest rate

Step 3: Find your repayment term (check your original loan agreement — typically 10, 15, or 20 years)

Step 4: Calculate your interest-only payment:

Balance × (Annual Rate ÷ 12) = Monthly interest-only payment

Step 5: Calculate your fully amortized repayment payment using our HELOC Payment Calculator — enter your balance, rate, and repayment term to get your exact monthly payment.

Step 6: Subtract Step 4 from Step 5. That is your payment shock number.

Once you see your actual number, you can decide which of the six strategies above makes the most sense for your situation.

When Payment Shock Becomes a Crisis

For most borrowers, payment shock is a manageable transition — uncomfortable but survivable with planning. For some, however, it becomes a genuine financial crisis.

Warning signs that your situation needs urgent attention:

- Your projected repayment payment exceeds 20% of your gross monthly income

- You have little to no savings buffer heading into repayment

- Your variable rate has risen more than 2% since you opened the HELOC

- You are already stretched thin on your current interest-only payments

If any of these apply, do not wait. Start exploring your refinancing options now, not six months before your draw period ends. Lenders take time. Appraisals take time. The window for comfortable refinancing closes faster than most borrowers expect.

The Consumer Financial Protection Bureau (CFPB) also offers resources for homeowners struggling with HELOC repayment, including guidance on working with lenders and understanding your rights.

The Bottom Line

HELOC payment shock is not inevitable. It is a predictable event with a known timeline — which means it is also entirely preventable with the right preparation.

The most important things to take away from this article:

- Know your draw period end date

- Understand the difference between your current interest-only payment and your future fully amortized payment

- Start paying down principal during the draw period if you can

- Explore refinancing options at least 12 months before repayment begins

- If you are already in trouble, talk to your lender — modification programs exist

Use our HELOC Payment Calculator to model your specific numbers right now. Five minutes of calculation today could save you hundreds of dollars a month later.