What is a HELOC Minimum Payment?

When you open a HELOC, your lender sets a minimum payment due each month — the smallest amount you are required to pay to keep your account in good standing. Understanding exactly what that minimum payment is, how it is calculated, and what it actually costs you over time is one of the most practical things a HELOC borrower can know.

The minimum payment on a HELOC is not fixed like a car loan or student loan payment. It changes based on your outstanding balance, your current interest rate, and which phase of the HELOC you are in. Pay only the minimum for years and you may find yourself owing just as much as when you started — sometimes more.

This guide explains everything you need to know about HELOC minimum payments — draw period, repayment period, the real cost of paying minimums long-term, and when it makes financial sense to pay more.

Why HELOC Minimum Payments Are Different From Other Loans

Most loans have a fixed minimum payment that stays the same every month from the first payment to the last. Your car loan payment is the same in month one as it is in month 48. Your student loan payment does not change unless you refinance or change repayment plans.

A HELOC is fundamentally different for three reasons:

Your balance changes. Unlike a loan where the balance only goes down, a HELOC lets you draw and repay repeatedly during the draw period. Your balance — and therefore your minimum payment — can go up or down from month to month depending on how you use the line.

Your interest rate changes. HELOCs carry variable interest rates tied to the prime rate. When the Federal Reserve adjusts rates, your HELOC rate moves too, and your minimum payment adjusts with it.

Your payment type changes completely between phases. During the draw period, your minimum payment is typically interest-only. During the repayment period, it becomes a fully amortized principal-plus-interest payment — a significant jump that catches many borrowers off guard.

Understanding these three variables is the foundation for understanding your HELOC minimum payment at any point in time.

HELOC Minimum Payment During the Draw Period

During the draw period — typically the first 5 to 10 years of your HELOC — the vast majority of lenders set the minimum payment equal to the interest accrued on your outstanding balance for that month.

This is called an interest-only minimum payment. You are paying the cost of borrowing for the month, but nothing toward the principal you owe.

The Formula

Minimum Payment = Outstanding Balance × (Annual Interest Rate ÷ 12)

This is calculated fresh every month based on your current balance and current rate. If either changes, your minimum payment changes too.

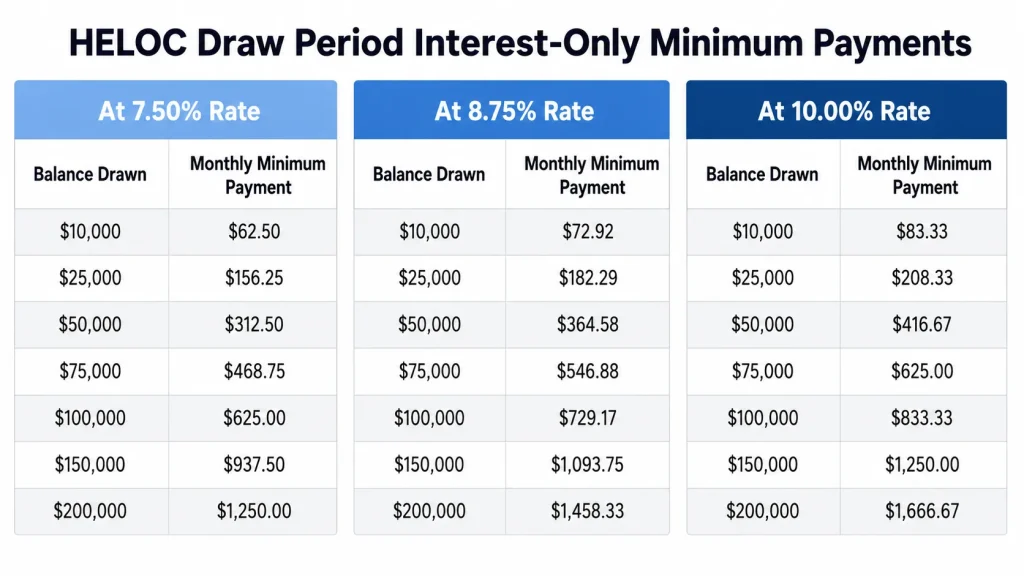

Draw Period Minimum Payment Examples

Here is what the interest-only minimum payment looks like across common HELOC balances at three different rate levels:

At 7.50% Interest Rate

| Balance Drawn | Monthly Minimum Payment |

|---|---|

| $10,000 | $63 |

| $25,000 | $156 |

| $50,000 | $313 |

| $75,000 | $469 |

| $100,000 | $625 |

| $150,000 | $938 |

| $200,000 | $1,250 |

At 8.75% Interest Rate

| Balance Drawn | Monthly Minimum Payment |

|---|---|

| $10,000 | $73 |

| $25,000 | $182 |

| $50,000 | $365 |

| $75,000 | $547 |

| $100,000 | $729 |

| $150,000 | $1,094 |

| $200,000 | $1,458 |

At 10.00% Interest Rate

| Balance Drawn | Monthly Minimum Payment |

|---|---|

| $10,000 | $83 |

| $25,000 | $208 |

| $50,000 | $417 |

| $75,000 | $625 |

| $100,000 | $833 |

| $150,000 | $1,250 |

| $200,000 | $1,667 |

Use our HELOC Payment Calculator to calculate your exact minimum payment based on your specific balance and current interest rate.

How Your Draw Period Minimum Payment Changes Month to Month

Because the minimum payment is recalculated monthly based on your current balance and rate, it can shift in three different ways:

When you draw more funds: Your balance increases, so your minimum payment increases. Draw an additional $20,000 on a $50,000 balance at 8.75% and your minimum payment jumps from $365 to $511 the following month.

When you pay down principal voluntarily: Your balance decreases, so your minimum payment decreases. Pay an extra $5,000 toward principal and your minimum drops by $36/month at 8.75%.

When your interest rate changes: Even with an unchanged balance, a rate change shifts your minimum. A 0.50% rate increase on a $100,000 balance adds $42/month to your minimum payment.

This fluidity is one of the key differences between a HELOC and a standard installment loan — and it is why you cannot simply set a fixed auto-payment and forget about your HELOC minimum payment indefinitely.

HELOC Minimum Payment During the Repayment Period

When the draw period ends, the minimum payment calculation changes entirely. Your outstanding balance is now fully amortized — spread across your remaining repayment term in equal monthly payments that cover both principal and interest.

The minimum payment in the repayment period is calculated the same way as a standard mortgage payment — using the standard amortization formula based on your balance, interest rate, and remaining term.

The Formula

Monthly Payment = P × [r(1+r)^n] ÷ [(1+r)^n − 1]

Where:

- P = outstanding principal balance

- r = monthly interest rate (annual rate ÷ 12)

- n = number of remaining monthly payments

You do not need to calculate this by hand — our HELOC Payment Calculator does it instantly. But understanding the formula clarifies why the repayment minimum is so much higher than the draw period minimum.

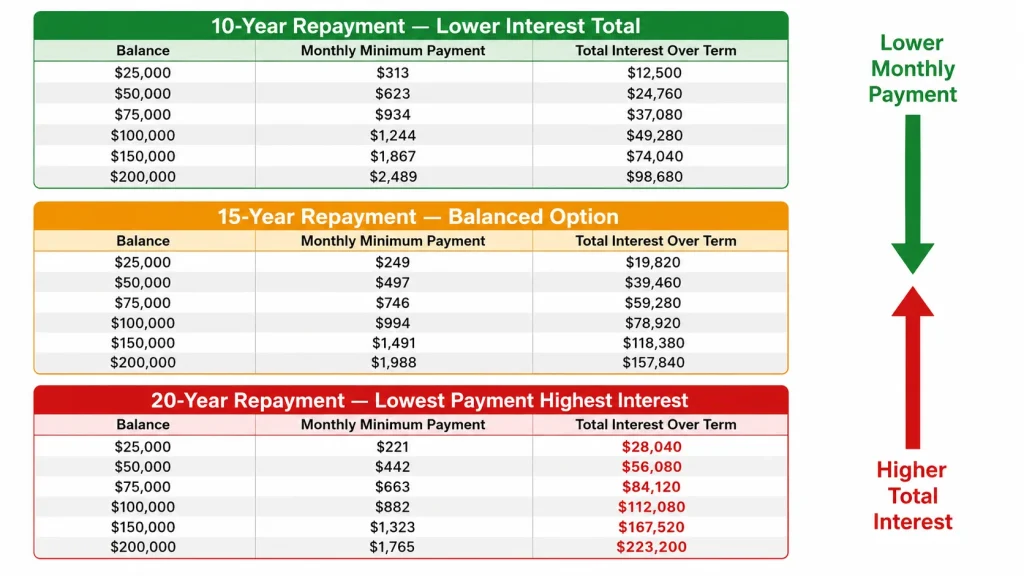

Repayment Period Minimum Payment Examples

Here is what the fully amortized minimum payment looks like for common balances at 8.75% across different repayment terms:

At 8.75% Interest Rate — 10-Year Repayment

| Balance at Repayment | Monthly Minimum Payment | Total Interest Over Term |

|---|---|---|

| $25,000 | $313 | $12,500 |

| $50,000 | $623 | $24,760 |

| $75,000 | $934 | $37,080 |

| $100,000 | $1,244 | $49,280 |

| $150,000 | $1,867 | $74,040 |

| $200,000 | $2,489 | $98,680 |

At 8.75% Interest Rate — 15-Year Repayment

| Balance at Repayment | Monthly Minimum Payment | Total Interest Over Term |

|---|---|---|

| $25,000 | $249 | $19,820 |

| $50,000 | $497 | $39,460 |

| $75,000 | $746 | $59,280 |

| $100,000 | $994 | $78,920 |

| $150,000 | $1,491 | $118,380 |

| $200,000 | $1,988 | $157,840 |

At 8.75% Interest Rate — 20-Year Repayment

| Balance at Repayment | Monthly Minimum Payment | Total Interest Over Term |

|---|---|---|

| $25,000 | $221 | $28,040 |

| $50,000 | $442 | $56,080 |

| $75,000 | $663 | $84,120 |

| $100,000 | $882 | $112,080 |

| $150,000 | $1,323 | $167,520 |

| $200,000 | $1,765 | $223,200 |

Notice the tradeoff clearly in these tables. A longer repayment term lowers your minimum payment but dramatically increases your total interest cost. A $100,000 balance repaid over 10 years costs $49,280 in interest. The same balance repaid over 20 years costs $112,080 — more than double — just for the privilege of a lower monthly minimum.

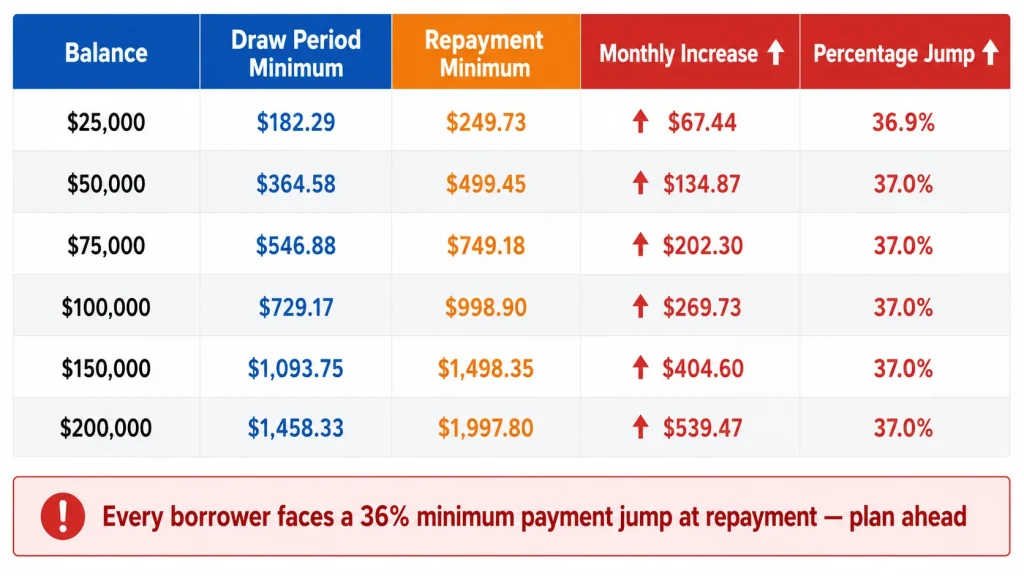

The Jump: Draw Period vs. Repayment Period Minimum Payment

The single most important thing to understand about HELOC minimum payments is how dramatically they increase when the draw period ends. This jump — known as payment shock — is the leading cause of HELOC-related financial hardship.

Here is a direct side-by-side comparison of draw period vs. repayment period minimum payments for common balances at 8.75%:

| Balance | Draw Period Minimum (Interest-Only) | Repayment Minimum (15-Year) | Monthly Increase | Percentage Jump |

|---|---|---|---|---|

| $25,000 | $182 | $249 | +$67 | +37% |

| $50,000 | $365 | $497 | +$132 | +36% |

| $75,000 | $547 | $746 | +$199 | +36% |

| $100,000 | $729 | $994 | +$265 | +36% |

| $150,000 | $1,094 | $1,491 | +$397 | +36% |

| $200,000 | $1,458 | $1,988 | +$530 | +36% |

Every borrower with a $100,000 balance faces a minimum payment increase of $265/month — just from the phase transition, before any rate changes are factored in. At $200,000, that jump is $530/month.

This is not a worst-case scenario. This is the standard, expected minimum payment increase for every HELOC borrower who carries a balance through the full draw period paying only the minimum.

We cover strategies to prepare for and reduce this jump in detail in our article on HELOC Payment Shock.

What Happens if You Only Pay the Minimum?

Most borrowers instinctively know they should pay more than the minimum. But seeing the concrete numbers makes it real.

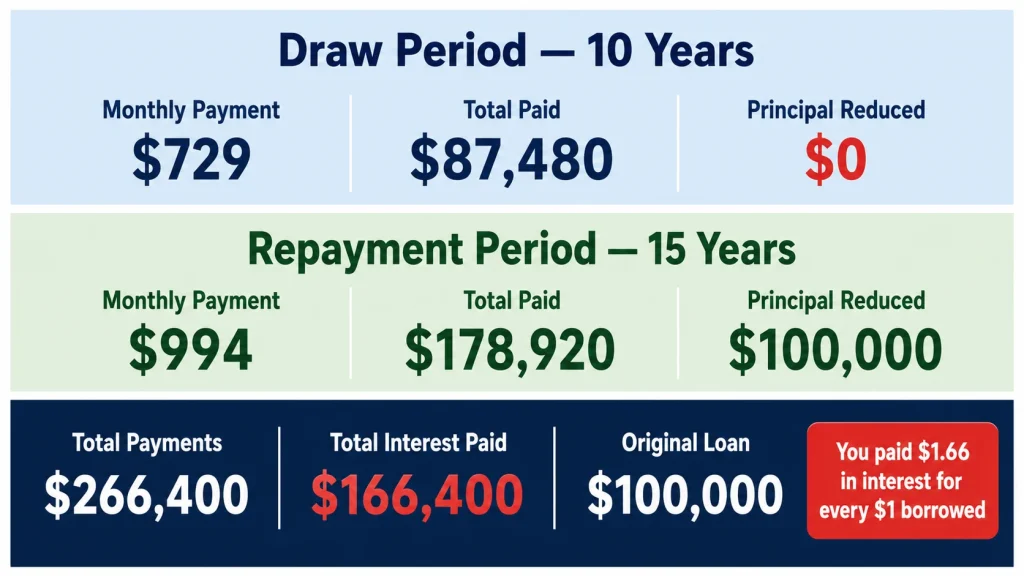

Here is what happens to a $100,000 HELOC at 8.75% if the borrower pays only the minimum throughout both periods — a 10-year draw period followed by a 15-year repayment period:

Draw period (10 years, interest-only minimum):

- Monthly payment: $729

- Total paid: $87,480

- Principal paid: $0

- Balance at end of draw period: $100,000

Repayment period (15 years, fully amortized minimum):

- Monthly payment: $994

- Total paid: $178,920

- Principal paid: $100,000

- Interest paid: $78,920

Full lifetime totals:

- Total payments made: $266,400

- Total interest paid: $166,400

- Original amount borrowed: $100,000

A borrower who took out $100,000 and paid only minimums for 25 years will have paid $266,400 — paying back the original $100,000 plus $166,400 in interest. They paid 1.66 times their original loan amount in interest charges alone.

This is the true cost of the minimum payment strategy on a HELOC. It is not wrong to pay the minimum when cash flow is tight — but treating it as the default strategy for the full life of the loan is one of the most expensive financial decisions a homeowner can make.

Minimum Payment vs. Paying Extra: A Direct Comparison

What does paying even modestly above the minimum actually accomplish? Here is a direct comparison on a $100,000 HELOC entering the repayment period at 8.75% with a 15-year term:

| Monthly Payment | Payoff Time | Total Interest | Savings vs. Minimum |

|---|---|---|---|

| $994 (minimum only) | 15 years | $78,920 | — |

| $1,094 (+$100) | 12 yrs 8 mos | $64,600 | $14,320 |

| $1,194 (+$200) | 11 yrs 1 mo | $56,800 | $22,120 |

| $1,294 (+$300) | 9 yrs 11 mos | $51,200 | $27,720 |

| $1,494 (+$500) | 8 yrs 4 mos | $42,600 | $36,320 |

| $1,744 (+$750) | 6 yrs 10 mos | $35,700 | $43,220 |

Adding just $100/month above the minimum saves $14,320 in interest and cuts 2 years 4 months off the payoff timeline. Adding $300/month saves $27,720 and eliminates more than 5 years of payments.

The minimum payment is a floor — not a financial strategy.

Does Your Lender Have a Different Minimum Payment Structure?

Not every lender calculates the HELOC minimum payment the same way. While interest-only draw period minimums are the most common structure, some lenders use alternative calculations worth knowing about.

1% of outstanding balance: Some lenders — particularly older HELOCs and certain bank products — set the draw period minimum at 1% of the outstanding balance rather than pure interest. On a $100,000 balance this equals $1,000/month, which is significantly higher than the interest-only minimum of $729/month at 8.75%. This structure actually works in the borrower’s favor since it forces some principal reduction each month.

Fixed minimum dollar amount: A small number of lenders set a flat minimum — say $100 or $150/month — regardless of balance or interest. This can result in situations where the minimum does not even cover the full interest accrued, leading to negative amortization where your balance actually grows each month. Always verify your lender’s minimum payment structure before signing.

Interest plus 1% of principal: Some lenders structure the draw period minimum as interest plus 1% of the outstanding principal balance. This is a more conservative structure that ensures some principal reduction from the first month.

Read your loan agreement carefully or ask your lender directly: “How is my minimum payment calculated, and does it cover the full interest accrued each month?”

What Happens if You Miss a HELOC Minimum Payment?

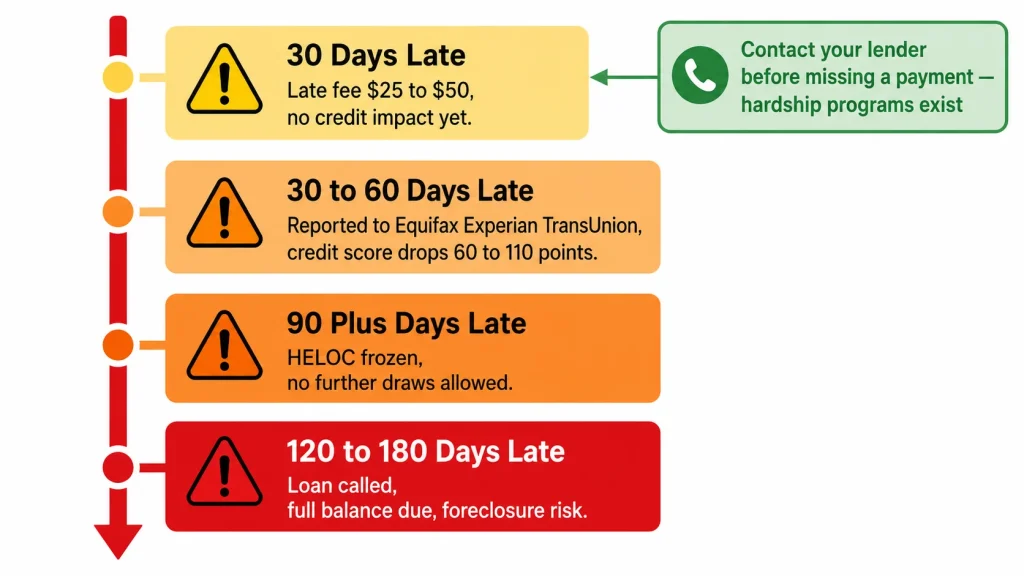

Missing a HELOC minimum payment has escalating consequences depending on how long the payment remains unpaid.

30 days late: Most lenders charge a late fee — typically $25 to $50. Your account may be flagged internally but typically no credit impact yet.

30–60 days late: Your lender reports the delinquency to the major credit bureaus — Equifax, Experian, and TransUnion. This triggers a credit score drop that can be significant depending on your overall credit profile. A single 30-day late payment can drop a good credit score by 60–110 points.

90+ days late: Your lender may freeze your HELOC — suspending your ability to draw additional funds even if your credit limit has availability. Some lenders accelerate this step at 60 days.

120–180 days late: The lender may call the loan — demanding full repayment of the outstanding balance immediately. If you cannot pay, foreclosure proceedings can begin since your home secures the debt.

If you are facing difficulty making your minimum payment, contact your lender immediately — before missing a payment. Most major lenders have hardship programs that can temporarily reduce your payment, extend your draw period, or modify your loan terms. These options disappear once you fall significantly behind.

How to Always Know Your Current Minimum Payment

Given that your HELOC minimum payment can change every month, staying on top of it requires a simple system:

Check your monthly statement. Your lender sends a monthly statement — either by mail or electronically — that shows your current balance, your current interest rate, and your minimum payment due. Make reading this statement a monthly habit, not an occasional one.

Set up account alerts. Most lenders allow you to set up automatic alerts when your payment amount changes, when your rate changes, or when your payment due date approaches. Use these — they take five minutes to configure and eliminate surprises.

Recalculate when rates change. Whenever you see news about the Federal Reserve adjusting the federal funds rate, check your HELOC statement the following month. Your rate — and your minimum — will have adjusted.

Use a calculator before drawing new funds. Before drawing additional money from your HELOC, calculate what your new minimum payment will be. Our HELOC Payment Calculator lets you model any balance and rate combination instantly so you always know what you are committing to before you draw.

The Bottom Line

Your HELOC minimum payment is not a fixed number — it is a dynamic figure that changes with your balance, your interest rate, and the phase of your HELOC. Understanding how it is calculated, how much it will jump when repayment begins, and what paying only the minimum costs you over time is essential knowledge for every HELOC borrower.

The key takeaways:

- Draw period minimums are interest-only — your balance never moves if you pay only the minimum

- Repayment period minimums are 35–37% higher than draw period minimums on the same balance — prepare for this jump well in advance

- Paying only the minimum on a $100,000 HELOC over 25 years costs $166,400 in interest

- Even $100–$200 extra per month above the minimum saves tens of thousands in interest and years of payments

- Check your statement monthly — your minimum payment can and does change

Use our HELOC Payment Calculator to find your exact minimum payment right now, and to model what happens when you pay above it. The numbers will make the decision easy.