HELOC vs. Home Equity Loan: Which is Better in 2026?

If you have built up equity in your home and need to borrow money, two products will come up in nearly every conversation: a HELOC and a home equity loan. Both let you tap your home’s equity. Both use your property as collateral. Both typically offer lower interest rates than credit cards or personal loans.

But they work very differently — and choosing the wrong one for your situation can cost you thousands of dollars in unnecessary interest, leave you with the wrong payment structure for your budget, or expose you to risks you did not anticipate.

This guide gives you a complete, honest side-by-side comparison of HELOCs and home equity loans in 2026 — covering rates, payments, flexibility, costs, tax treatment, and the specific situations where each product wins clearly.

The Fundamental Difference in One Paragraph

A home equity loan gives you a single lump sum of money at a fixed interest rate, repaid in equal monthly installments over a set term — typically 5 to 30 years. From the day you close, your payment never changes. You know exactly what you owe and exactly when it will be paid off.

A HELOC gives you a revolving credit line at a variable interest rate. You draw what you need, when you need it, repay it, and borrow again — like a credit card secured by your home. Your payment changes based on your outstanding balance and the current interest rate.

Everything else in this comparison flows from that core difference: certainty and simplicity vs. flexibility and variability.

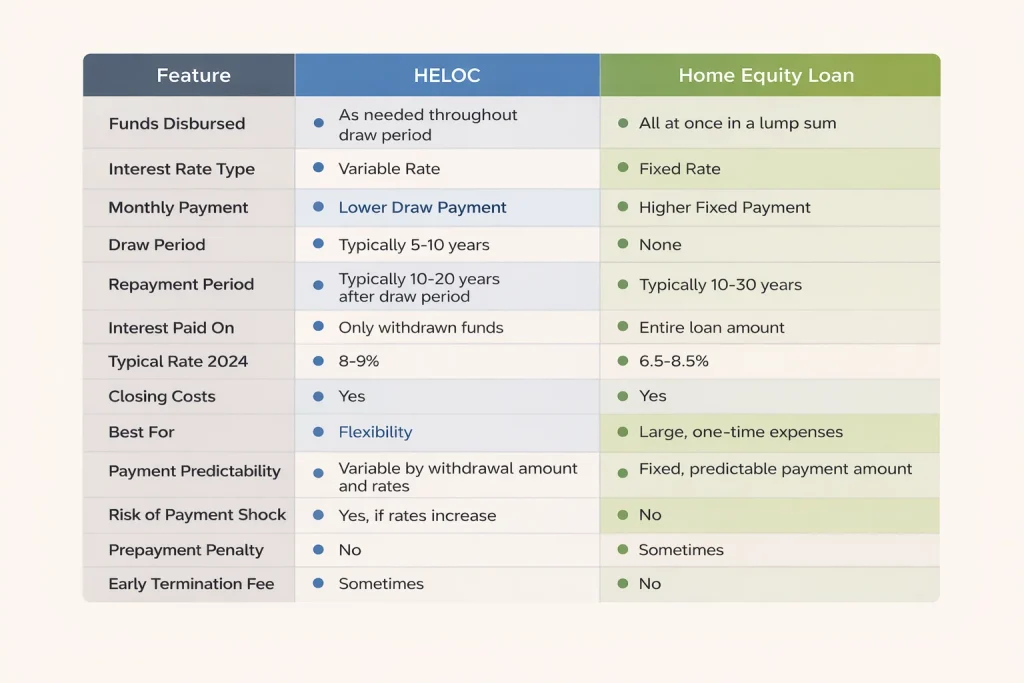

Side-by-Side Comparison: HELOC vs. Home Equity Loan

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Funds disbursed | As needed, up to credit limit | Full lump sum at closing |

| Interest rate type | Variable (tied to prime rate) | Fixed for life of loan |

| Monthly payment | Changes with balance and rate | Fixed — same every month |

| Draw period | 5–10 years (borrow as needed) | None — one-time disbursement |

| Repayment period | 10–20 years | 5–30 years (starts immediately) |

| Interest paid on | Only amount drawn | Full loan amount from day one |

| Typical rate in 2026 | 8.25% – 10.50% variable | 7.50% – 9.50% fixed |

| Closing costs | $200 – $2,000 | $500 – $3,000 |

| Best for | Ongoing or staged expenses | One-time, known expenses |

| Payment predictability | Low — changes monthly | High — never changes |

| Risk of payment shock | Yes — at draw period end | No — payment is fixed |

| Prepayment penalty | Rarely | Sometimes |

| Early termination fee | Sometimes | Rarely |

Interest Rates: HELOC vs. Home Equity Loan in 2026

This is the comparison that most borrowers focus on first — and where the most confusion exists.

HELOC Rates

HELOCs carry variable interest rates tied to the Wall Street Journal Prime Rate plus a lender margin. In June 2026, the prime rate sits at 7.50%, meaning most HELOC rates are in the range of 8.25% to 10.50% depending on your credit score, LTV ratio, and lender.

Your HELOC rate moves whenever the Federal Reserve adjusts the federal funds rate. If rates rise 0.50%, your HELOC rate rises 0.50% — automatically, on your next billing cycle. If rates fall, your rate falls too.

This variability cuts both ways. In a falling rate environment, HELOC borrowers benefit without doing anything. In a rising rate environment, they absorb higher costs without any choice in the matter.

Home Equity Loan Rates

Home equity loans carry fixed interest rates set at closing and unchanged for the life of the loan. In 2026, fixed home equity loan rates range from approximately 7.50% to 9.50% for well-qualified borrowers — often slightly lower than current HELOC rates because lenders price in a premium for the certainty they are providing.

Once you close on a home equity loan at 8.25%, that rate is yours regardless of what the Federal Reserve does over the next 20 years. Rates can rise 3% and your payment does not move a cent.

Which Rate Is Actually Better?

This depends entirely on the rate environment and your timeline. Here is the honest assessment:

If rates are expected to fall: A HELOC benefits you automatically as your rate drops with the prime rate. A fixed home equity loan locks you into a rate that may look expensive in two years.

If rates are expected to rise: A home equity loan protects you completely. A HELOC exposes you to every rate increase over your borrowing period.

If rates are stable: The difference is minimal and the initial rate comparison is what matters most.

In 2026, with rates having stabilized after the aggressive hiking cycle of 2022–2024, many economists expect moderate rate cuts over the next 12–24 months. In this environment, HELOCs carry slightly more appeal — but the future is never certain, and a fixed rate provides genuine peace of mind that has real value.

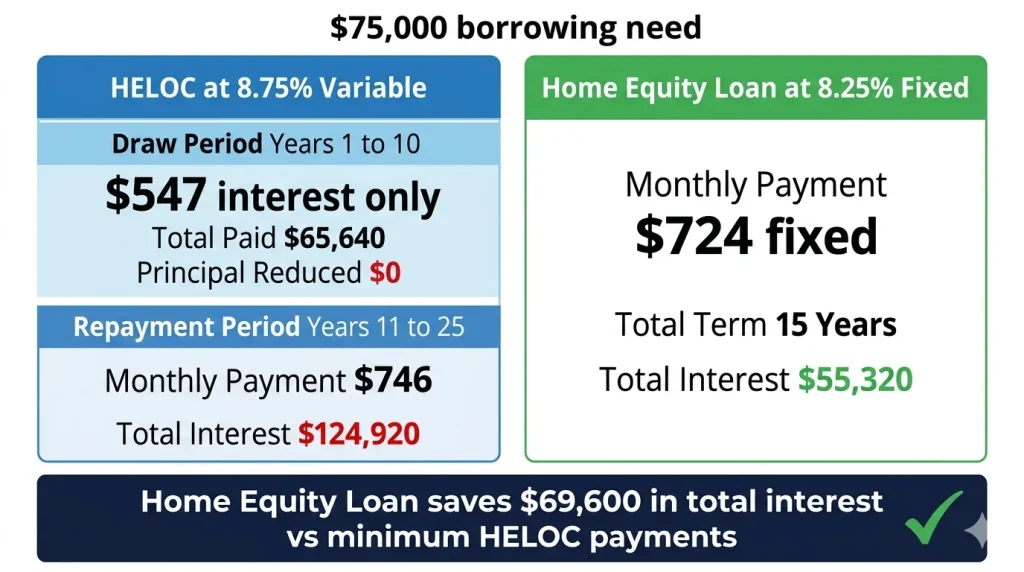

Monthly Payments: A Real Dollar Comparison

Let us run the actual payment math on a $75,000 borrowing need under both products in 2026.

Home Equity Loan: $75,000 at 8.25% Fixed, 15 Years

- Monthly payment: $724 every month, from month one to month 180

- Total interest paid: $55,320

- Payment predictability: 100% — never changes

HELOC: $75,000 Draw at 8.75% Variable, 10-Year Draw + 15-Year Repayment

Draw period (years 1–10, interest-only minimum):

- Monthly payment: $547 (interest only)

- Total paid in draw period: $65,640

- Principal reduced: $0

Repayment period (years 11–25):

- Monthly payment: $746 (principal + interest)

- Total paid in repayment: $134,280

- Total interest over full 25 years: $124,920

The Comparison Summary

| Home Equity Loan | HELOC (minimum payments) | |

|---|---|---|

| Monthly payment | $724 fixed | $547 draw / $746 repayment |

| Total term | 15 years | 25 years |

| Total interest paid | $55,320 | $124,920 |

| Total cost difference | — | $69,600 more |

Wait — does this mean a home equity loan is always cheaper? Not necessarily. The HELOC comparison above assumes the borrower draws the full $75,000 immediately and pays only interest-only minimums for the entire 10-year draw period. That is the worst-case HELOC scenario.

If the borrower only needs $30,000 initially and draws the rest over time — or makes extra principal payments during the draw period — the HELOC’s total interest cost drops significantly. The flexibility of a HELOC is only worth its cost when you actually use it strategically.

Use our HELOC Payment Calculator to model your specific borrowing scenario under both structures.

Flexibility: Where the HELOC Wins Clearly

The home equity loan’s fixed payment and predictable structure are genuine advantages — but they come with a significant tradeoff: you receive all the money at once and start paying interest on the full amount immediately, whether you use it or not.

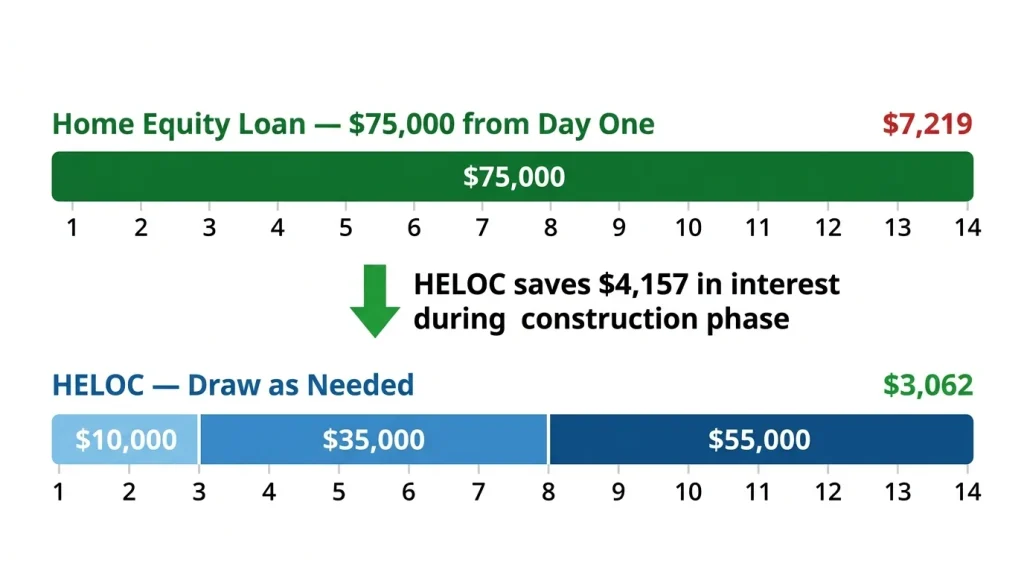

If you borrow $75,000 through a home equity loan for a kitchen renovation that will take 14 months to complete, you pay interest on $75,000 from day one — including the months when $50,000 of it is still sitting in your bank account waiting to be spent.

A HELOC solves this precisely. You draw $10,000 in month one for demo and framing. Another $25,000 in month four for cabinets and appliances. Another $20,000 in month nine for countertops and finishing. You only pay interest on what you have actually drawn, not on the $75,000 credit limit sitting available.

For a renovation unfolding over 12 months:

Home equity loan ($75,000 from day one at 8.25%):

- Month 1–14 interest cost: $75,000 × 0.6875% × 14 months = $7,219

HELOC (drawn in stages, average balance $30,000 over 14 months at 8.75%):

- Month 1–14 interest cost: $30,000 × 0.7292% × 14 months = $3,062

The HELOC’s staged drawing saves $4,157 in interest over the construction period alone — just from the flexibility of drawing as needed rather than taking everything upfront.

This flexibility advantage is real and meaningful for any expense that unfolds over time. It disappears completely for a one-time lump sum need like paying off a specific debt or funding a single known expense.

Payment Shock Risk: The HELOC’s Key Disadvantage

The home equity loan has one significant structural advantage that the interest rate comparison alone does not capture: there is no payment shock.

From the day you close a home equity loan, your payment is fully amortized. You are reducing principal from month one. There is no draw period ending, no phase transition, no sudden payment increase. The payment you see at closing is the payment you make for the life of the loan.

A HELOC borrower who carries a $75,000 balance through the full draw period faces a payment jump from $547/month to $746/month — a $199/month increase — simply from the phase transition. If their rate has also risen during the draw period, the jump can be larger.

For borrowers who are concerned about managing a variable budget or who want complete payment certainty, this is a decisive argument for the home equity loan.

We cover payment shock in detail in our article on HELOC Payment Shock.

Closing Costs: How They Compare

Both products require closing costs, but the amounts differ.

| Cost Item | HELOC | Home Equity Loan |

|---|---|---|

| Application fee | $0 – $500 | $0 – $500 |

| Origination fee | $0 – 1% | 0.5% – 1% |

| Appraisal fee | $0 – $700 | $300 – $700 |

| Title search | $75 – $400 | $100 – $400 |

| Recording fee | $25 – $250 | $25 – $250 |

| Typical total | $200 – $2,000 | $500 – $3,000 |

Home equity loans generally cost slightly more to close than HELOCs because they are treated more like a traditional mortgage by most lenders — requiring more extensive underwriting, title insurance, and documentation.

However, both products cost significantly less to close than a cash-out refinance, which typically runs $3,000 to $6,000 or more.

Tax Deductibility: Same Rules Apply to Both

Under current IRS rules, interest on both HELOCs and home equity loans is tax deductible only if the funds are used to buy, build, or substantially improve the home securing the loan. This rule applies equally to both products — there is no tax advantage of one over the other.

Interest used for debt consolidation, education, vacations, or any non-home purpose is not deductible on either product. Always consult a tax advisor for your specific situation before factoring deductibility into your borrowing decision.

Credit Score and Qualification: Similar Requirements

Both products use your home as collateral and have broadly similar qualification requirements. Most lenders require:

- Credit score: 620 minimum, 700+ for best rates on both products

- Combined LTV: 80–85% maximum for most lenders

- DTI ratio: Below 43% including the new payment

- Home equity: At least 15–20% equity in the property

- Stable income: Documented through pay stubs, W-2s, or tax returns

One nuance: some lenders apply slightly stricter underwriting standards to home equity loans because the fixed payment is a committed obligation from day one — there is no interest-only draw period to ease into. HELOC qualification can sometimes be slightly more lenient because the lender accounts for the lower interest-only payment in the DTI calculation.

Which Product Wins in Specific Situations

Rather than declaring one product universally better, the honest answer is that each one wins clearly in specific circumstances.

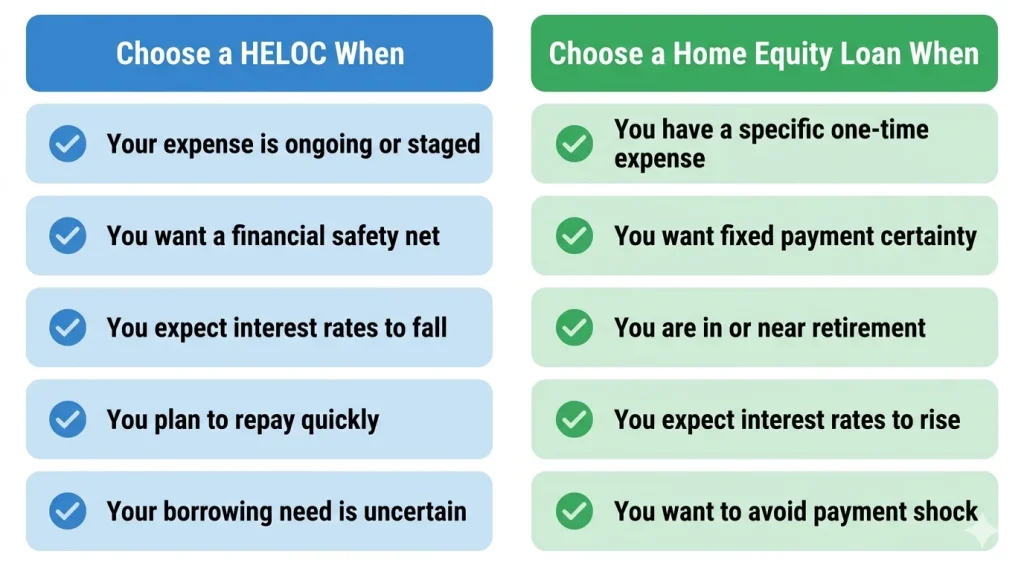

Choose a HELOC when:

Your expense is ongoing or staged. Home renovation in phases, a business investment with irregular capital needs, college tuition spread over four years — any situation where you draw money gradually benefits from the HELOC’s pay-only-for-what-you-use structure.

You want a financial safety net. A HELOC with a zero balance costs you almost nothing but gives you immediate access to funds in a genuine emergency. A home equity loan requires you to carry the full balance from day one.

You expect interest rates to fall. In a declining rate environment, your HELOC rate falls automatically. You benefit without refinancing.

You plan to repay quickly. If you intend to pay off the balance within 2 to 3 years — from a business profit, a home sale, or aggressive extra payments — the HELOC’s flexibility and lower draw-period payment works in your favor.

Your borrowing need is uncertain. If you are not sure exactly how much you need, a HELOC lets you take what is required and no more, rather than guessing upfront and over-borrowing on a home equity loan.

Choose a home equity loan when:

You have a specific, known one-time expense. Paying off a defined debt amount, funding a single large purchase, covering a specific medical bill — any situation where you know exactly how much you need and need it all at once.

You want payment certainty. If your budget depends on predictable fixed expenses and you cannot absorb a variable payment that fluctuates with interest rates, the home equity loan’s fixed payment is worth the slightly higher rate.

You are concerned about overspending. A revolving credit line is psychologically easier to over-draw than a one-time lump sum. Borrowers who are concerned about using more than they intended benefit from the home equity loan’s closed structure.

You are in or near retirement. Fixed income households particularly benefit from fixed payment obligations. A HELOC’s variable rate and payment shock risk are harder to manage on a retirement budget.

You expect interest rates to rise significantly. Locking in a fixed rate today protects you completely from future rate increases that would drive a HELOC’s cost higher.

You want to avoid payment shock. If the prospect of a sudden 35–40% payment increase at the end of a draw period concerns you, a home equity loan eliminates this risk entirely.

A Practical Decision Example

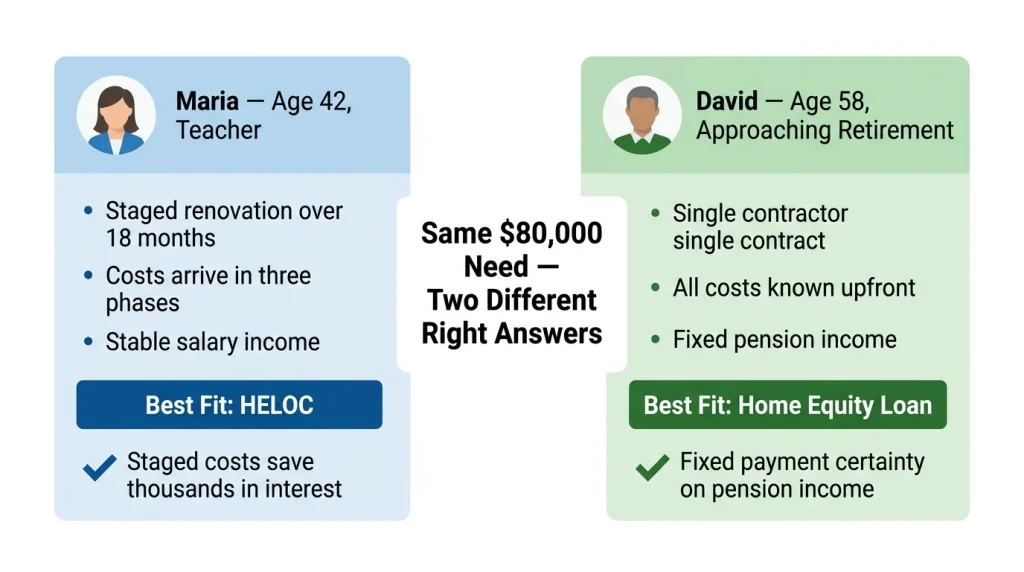

Meet two homeowners facing the same situation — both need $80,000 for home improvements and both qualify for either product.

Homeowner A — Maria, 42, teacher, stable salary: Maria is replacing her roof ($15,000), finishing her basement ($35,000), and upgrading her kitchen ($30,000). The projects will unfold over 18 months with costs arriving in three phases. She plans to make modest extra payments but will not pay the balance off in under 5 years.

Best fit: HELOC. Her staged costs benefit from draw-as-needed structure. She saves thousands in interest by not carrying the full $80,000 balance during the construction phase. Her stable income means she can manage a variable payment.

Homeowner B — David, 58, approaching retirement, fixed pension income: David needs $80,000 to add an accessible first-floor master suite — a single contractor, a single contract, all costs known upfront. He wants to know exactly what his payment will be for the next 15 years on his pension income.

Best fit: Home equity loan. He needs the full amount at once, wants payment certainty on a fixed income, and has no use for revolving credit flexibility. The home equity loan’s fixed payment eliminates all variable rate and payment shock risk.

Same loan amount. Same equity. Two completely different right answers.

What If You Cannot Decide? Consider Both

Some homeowners use both products simultaneously — a home equity loan for a specific known expense and a HELOC kept open at zero balance as an emergency reserve. Most lenders allow this as long as your combined LTV stays within their limits and your DTI supports both payment obligations.

This approach gives you the payment certainty of the home equity loan for your current need while preserving the flexible credit access of a HELOC for future use. The cost of maintaining a zero-balance HELOC is typically just the annual fee — often $0 to $75/year — which many borrowers consider cheap insurance.

The Bottom Line

Neither product is universally better. The right choice depends entirely on your specific situation.

HELOC wins when: You need flexibility, your costs arrive in stages, you expect rates to fall, or you want a safety net without carrying a balance.

Home equity loan wins when: You need a specific lump sum, want fixed payments, are on a fixed income, or are concerned about rate increases and payment shock.

The single most useful question to ask yourself: Do I know exactly how much I need, and do I need it all at once?

If yes — home equity loan. If no — HELOC.

Use our HELOC Payment Calculator to model your exact borrowing scenario under both products and see the total cost difference for your specific numbers.