HELOC vs. Cash-Out Refinance: How to Decide

You have equity in your home and a financial goal that requires capital — a major renovation, debt consolidation, an investment, or a large expense you cannot comfortably fund from savings. Two of the most powerful tools available to you are a HELOC and a cash-out refinance.

Both access your home equity. Both can deliver tens of thousands of dollars. But they work through entirely different mechanisms, carry very different costs, and make sense in very different circumstances.

In 2026 — with mortgage rates significantly higher than the historic lows of 2020 and 2021 — the cash-out refinance vs. HELOC decision carries more financial weight than it did a few years ago. Millions of homeowners are sitting on low fixed-rate mortgages between 2.75% and 4.5%. Refinancing those mortgages to access equity means giving up that rate permanently. The math has changed dramatically.

This guide walks through every dimension of the comparison so you can make the right decision for your situation with full information.

How Each Product Works

HELOC: A Second Lien, Your First Mortgage Untouched

A HELOC is a second mortgage — a separate loan added on top of your existing first mortgage. Your original mortgage stays exactly as it is, with its current rate, balance, and payment completely unchanged.

The HELOC gives you a revolving credit line secured by your home equity, with a variable interest rate tied to the prime rate. You draw what you need during the draw period, pay interest-only minimums, then repay the full balance during the repayment period.

Key point: A HELOC does not touch your existing mortgage.

Cash-Out Refinance: A New First Mortgage That Replaces the Old One

A cash-out refinance replaces your existing mortgage entirely with a new, larger mortgage. The difference between your new loan amount and your old balance is paid out to you in cash at closing.

For example: You owe $220,000 on your current mortgage. Your home is worth $400,000. You do a cash-out refinance for $300,000. At closing, your old $220,000 mortgage is paid off, and you receive the remaining $80,000 in cash — minus closing costs.

Key point: A cash-out refinance replaces your entire mortgage at the current market rate.

The Rate Question: The Most Important Factor in 2026

This comparison starts and ends with interest rates in 2026 — specifically, what rate you currently have on your existing mortgage.

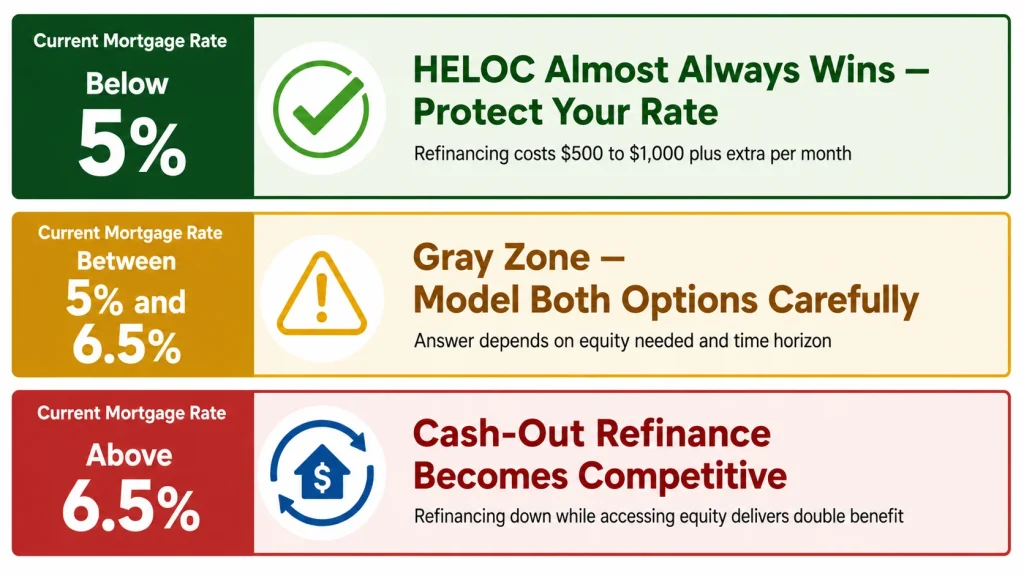

If Your Current Mortgage Rate Is Below 5%

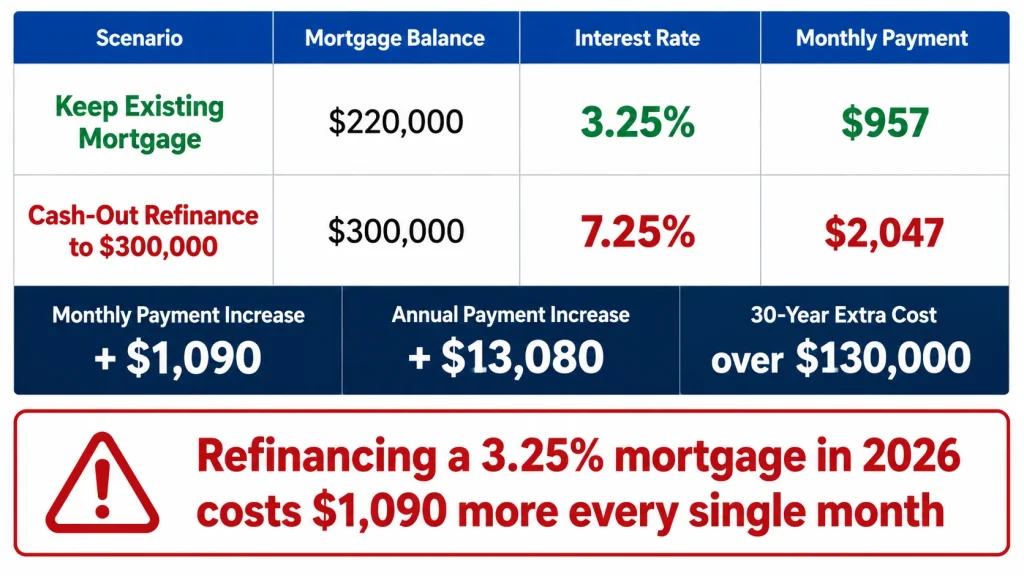

This is the situation for tens of millions of American homeowners who bought or refinanced between 2019 and 2022. If you locked in a 30-year fixed mortgage at 3.25%, 3.5%, or even 4.25%, a cash-out refinance in 2026 would replace that rate with today’s prevailing 30-year fixed rate — currently in the range of 6.75% to 7.50% for most borrowers.

Here is what that means in real dollars on a $220,000 remaining mortgage balance:

| Scenario | Mortgage Balance | Rate | Monthly Payment |

|---|---|---|---|

| Keep existing mortgage | $220,000 | 3.25% | $957 |

| Cash-out refinance to $300,000 | $300,000 | 7.25% | $2,047 |

| Monthly payment increase | +$1,090/month | ||

| Annual payment increase | +$13,080/year |

A homeowner who refinances a 3.25% mortgage to access $80,000 in equity pays an extra $1,090/month — $13,080/year — in higher mortgage costs. Over a 30-year term, the rate difference alone costs an additional $130,000+ compared to keeping the existing mortgage and accessing equity through a HELOC instead.

In this scenario, a HELOC is almost always the right answer. The cost of giving up a sub-5% mortgage to access equity is simply too high in 2026’s rate environment.

If Your Current Mortgage Rate Is Above 6.5%

If you bought your home in 2023 or 2024 — or have an adjustable-rate mortgage that has reset higher — your current rate may already be close to or above today’s refinance rates. In this case, a cash-out refinance becomes far more competitive because you are not sacrificing a historically low rate to access equity.

If you can refinance your $280,000 mortgage from 7.5% down to 7.0% and pull out $60,000 in equity at the same time, you are accessing capital while simultaneously lowering your mortgage rate. That is a compelling combination.

If Your Rate Is Between 5% and 6.5%

This is the genuine gray zone where the decision requires careful modeling. You would be giving up some rate advantage to access equity, but not as catastrophically as the sub-5% scenario. The answer depends on how much equity you need, what you plan to do with it, and how long you plan to stay in the home.

Closing Costs: The Biggest Upfront Difference

This is where the HELOC wins most clearly against a cash-out refinance — and the gap is substantial.

| Cost Item | HELOC | Cash-Out Refinance |

|---|---|---|

| Origination/lender fees | $0 – $1,000 | $1,000 – $3,000 |

| Appraisal | $0 – $700 | $500 – $700 |

| Title search and insurance | $75 – $1,000 | $1,000 – $2,500 |

| Attorney/settlement fees | $150 – $500 | $500 – $1,500 |

| Recording fees | $25 – $250 | $25 – $250 |

| Discount points | None typically | 0 – 2% of loan |

| Typical total | $200 – $2,000 | $3,000 – $6,000+ |

On a $300,000 cash-out refinance, closing costs of $6,000 represent 2% of the loan amount. That $6,000 is either paid upfront or rolled into the new loan — where it accrues interest for the full 30-year term, ultimately costing significantly more.

A HELOC on the same property to access the same equity amount might cost $500 to $1,500 to open. The upfront cost difference alone — $4,500 to $5,500 — is a meaningful factor in the decision.

Break-even calculation for cash-out refinance: If you are refinancing to a lower rate (saving money monthly) while also accessing cash, calculate how many months it takes for your monthly savings to recover the closing costs. If your break-even is 36 months and you plan to stay in the home for 10 years, the refinance may make sense. If the break-even is 60 months and you might move in 4 years, it does not.

Monthly Payment Impact: Comparing Real Scenarios

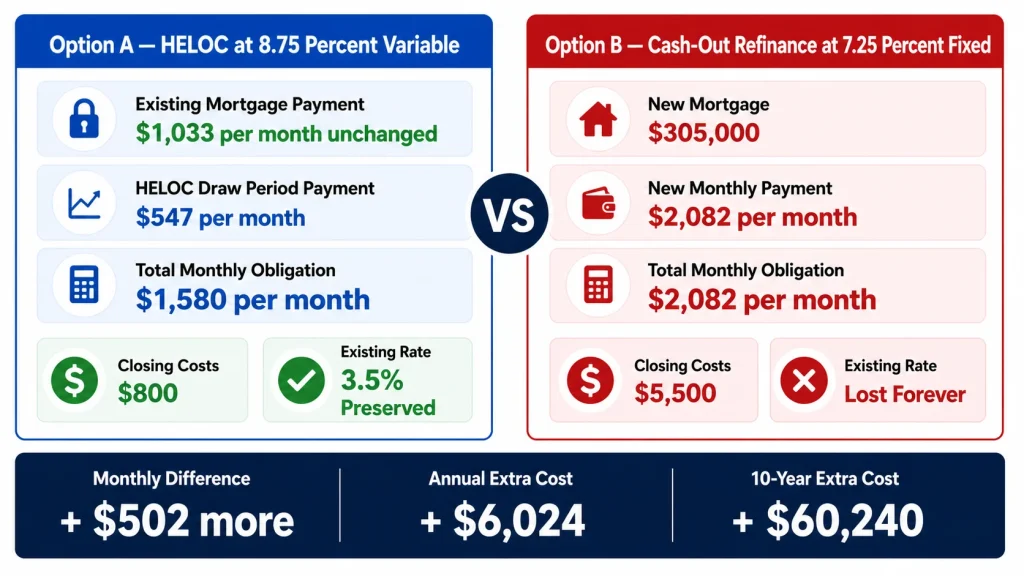

Let us model two homeowners accessing $75,000 in equity — one through a HELOC, one through a cash-out refinance.

Profile: Homeowner with $230,000 remaining on a 3.5% fixed mortgage, home worth $420,000, needs $75,000 for home renovation.

Option A: HELOC at 8.75% Variable

- Existing mortgage payment: $1,033/month (unchanged)

- HELOC draw period payment: $547/month (interest-only on $75,000)

- Total monthly obligation: $1,580/month

- Closing costs: $800

- Existing mortgage rate: 3.5% preserved

Option B: Cash-Out Refinance at 7.25% Fixed

- New mortgage: $305,000 (existing $230,000 + $75,000 cash out)

- New monthly payment: $2,082/month

- Total monthly obligation: $2,082/month

- Closing costs: $5,500

- Existing 3.5% mortgage: gone forever

| HELOC | Cash-Out Refinance | |

|---|---|---|

| Monthly payment | $1,580 | $2,082 |

| Monthly difference | — | +$502 more |

| Closing costs | $800 | $5,500 |

| Existing mortgage rate | 3.5% preserved | Lost — now at 7.25% |

| Annual extra cost | — | +$6,024 |

| 10-year extra cost | — | +$60,240 |

For this homeowner, the cash-out refinance costs $502 more per month and $60,240 more over 10 years — entirely due to giving up the 3.5% mortgage rate.

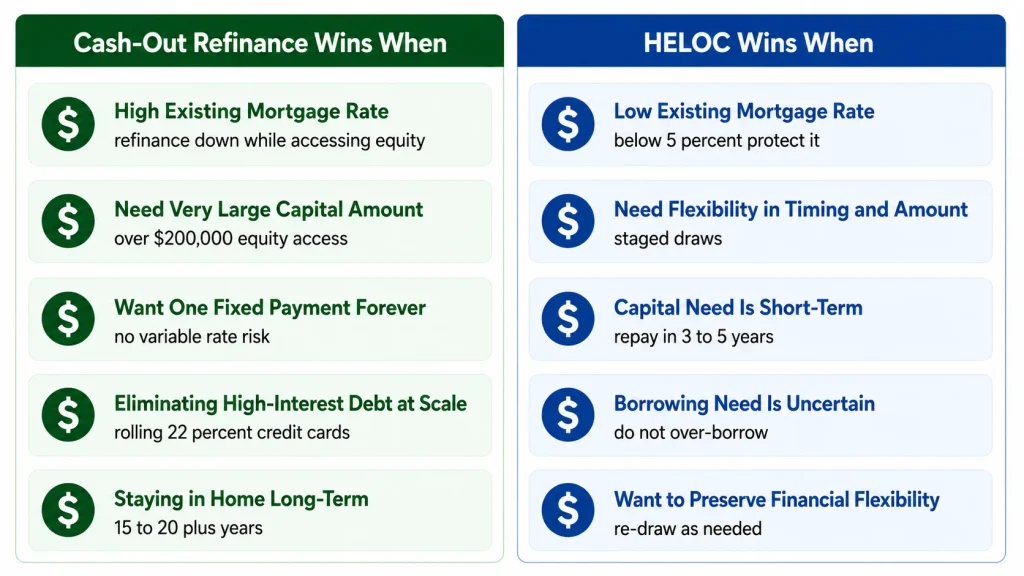

When Cash-Out Refinance Wins: Specific Scenarios

Despite the rate environment working against it for many homeowners in 2026, there are clear situations where a cash-out refinance is the better choice.

You Have a High Existing Mortgage Rate

As discussed, if your current mortgage rate is at or above 6.5%, a cash-out refinance that simultaneously lowers your rate and accesses equity can deliver a double benefit. You get the capital you need and reduce your mortgage cost at the same time.

You Need a Very Large Amount of Capital

Cash-out refinances can access significantly more equity than a HELOC in some cases — particularly for large loan amounts. Most lenders cap HELOC credit lines at 80–85% CLTV, but some cash-out refinance programs allow up to 80% LTV on the new first mortgage only, which may produce a larger accessible equity pool depending on your situation.

If you need $200,000 or more in equity access and your CLTV limits your HELOC to less than that, a cash-out refinance may be the only viable option.

You Want One Simple Fixed Payment Forever

A cash-out refinance consolidates everything into a single fixed mortgage payment for the next 15 to 30 years. No second lien. No variable rate. No draw period. No repayment period transition. No payment shock risk.

For borrowers who strongly value simplicity and payment certainty above all else — particularly those who struggle to manage multiple debt obligations — one consolidated fixed payment has genuine appeal even at a higher total cost.

You Are Eliminating High-Interest Debt at Scale

If you are rolling $80,000 of credit card debt at 22%+ APR into a cash-out refinance at 7.25%, the interest rate reduction is dramatic. Even accounting for the loss of a lower mortgage rate, the savings on the eliminated high-interest debt can make the math work — particularly for large debt amounts.

The critical caveat: this only works if you do not re-accumulate the credit card debt after the refinance. Rolling unsecured debt into your mortgage and then running the cards back up is the fastest route to a genuine financial crisis.

You Plan to Stay in the Home Long-Term

The higher closing costs of a cash-out refinance are easier to justify when you spread them over a long horizon. If you plan to stay in the home for 15 to 20 years and the monthly payment difference versus a HELOC is modest, the long-term simplicity of a single mortgage payment may outweigh the upfront cost difference.

When HELOC Wins: Specific Scenarios

You Have a Low Existing Mortgage Rate

If your mortgage rate is below 5% — and especially if it is below 4% — protecting that rate is almost always the right financial decision in 2026. A HELOC lets you access your equity without touching your first mortgage. This is the single most compelling argument for a HELOC in today’s rate environment.

You Need Flexibility in Timing and Amount

Ongoing home renovations, a business investment with uncertain capital needs, college tuition spread over multiple years — any situation where you need to draw money in stages benefits from the HELOC’s revolving structure. You pay interest only on what you have drawn, not on a lump sum sitting in your bank account.

Your Capital Need Is Short-Term

If you plan to repay the borrowed amount within 3 to 5 years — from a business sale, an inheritance, aggressive extra payments, or a home sale — a HELOC’s lower closing costs and flexible repayment make it significantly more efficient than a 30-year cash-out refinance with $5,000+ in closing costs.

Your Borrowing Need Is Uncertain

If you are not sure exactly how much you need — a renovation where costs may shift, a business where capital requirements are unclear — a HELOC lets you take only what you actually use. A cash-out refinance requires you to guess your needs upfront and take the full amount at closing, paying interest on every dollar from day one.

You Want to Preserve Financial Flexibility

A HELOC that is paid down can be re-drawn during the draw period. You access equity, use it, repay it, and the credit becomes available again. A cash-out refinance is a one-time transaction — once you have the cash and close the loan, the only way to access more equity is another full refinance with another round of closing costs.

The Tax Deduction: Same Rules, Different Application

Both products may offer interest deductibility when funds are used for home improvement, subject to IRS rules. However, there is a practical difference in application.

With a cash-out refinance, your entire new mortgage interest is potentially deductible — though IRS rules limit deductibility to loans up to $750,000 for joint filers, and the deductibility of the cash-out portion depends on how those funds are used.

With a HELOC, only the interest on funds used for home improvement qualifies. Interest on HELOC funds used for other purposes — debt consolidation, education, investments — does not.

For most homeowners using either product for home improvement, both qualify for the same deduction. The tax treatment is rarely the deciding factor between these two products. Always consult a tax advisor for your specific situation.

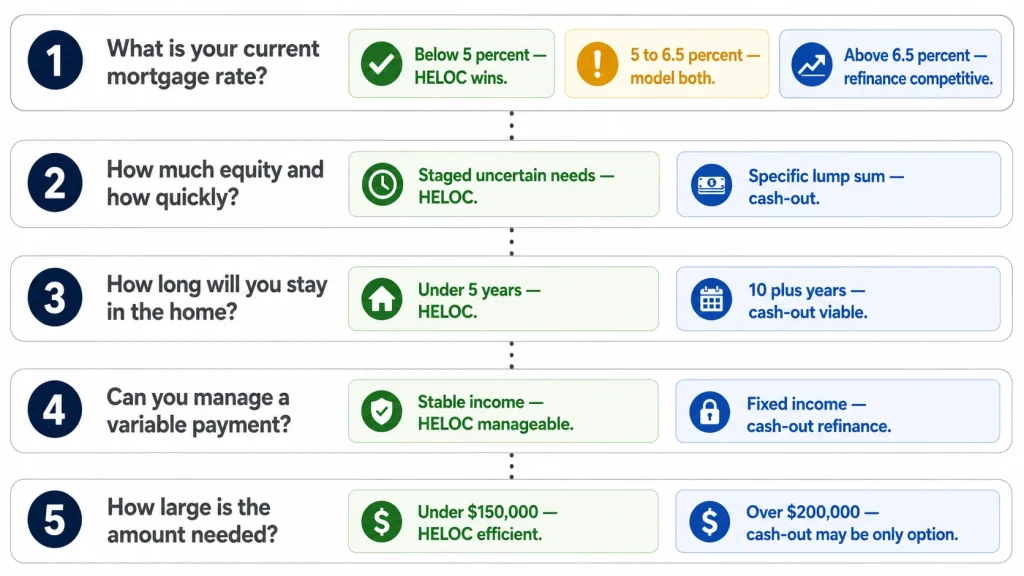

The Decision Framework: Five Questions to Answer

Work through these five questions in order to arrive at the right answer for your situation.

Question 1: What is your current mortgage rate?

- Below 5% → HELOC almost always wins. Protect your rate.

- 5% to 6.5% → Model both options carefully with real numbers.

- Above 6.5% → Cash-out refinance becomes genuinely competitive.

Question 2: How much equity do you need and how quickly?

- Specific known amount needed all at once → Cash-out refinance more appropriate.

- Uncertain amount or staged needs → HELOC wins on flexibility.

Question 3: How long will you stay in the home?

- Less than 5 years → HELOC wins. Cash-out refinance closing costs do not have time to recover.

- 10+ years → Long-term simplicity of cash-out refinance becomes more attractive.

Question 4: Can you manage a variable payment?

- Fixed income, tight budget, or strong preference for certainty → Cash-out refinance.

- Stable income with flexibility to absorb rate changes → HELOC manageable.

Question 5: How large is the amount you need?

- Under $150,000 → HELOC typically handles this efficiently.

- Over $200,000 → Cash-out refinance may be the only practical option for some homeowners.

Side-by-Side Summary

| Factor | HELOC | Cash-Out Refinance |

|---|---|---|

| Existing mortgage | Untouched | Replaced entirely |

| Rate type | Variable | Fixed |

| Closing costs | $200 – $2,000 | $3,000 – $6,000+ |

| Monthly payment | Lower initially | Higher (includes full mortgage) |

| Best rate environment | Protect low existing rate | High existing rate — refinance down |

| Flexibility | High — draw as needed | None — lump sum only |

| Payment certainty | Low | High |

| Best loan amount | Under $150,000 typically | Any size |

| Short-term need | Excellent | Poor — high closing costs |

| Long-term need | Good | Good |

| Complexity | Two payments | One payment |

The Bottom Line

In 2026, for the majority of homeowners who locked in mortgage rates below 5% between 2019 and 2022, a HELOC is the clearly superior way to access home equity. The cost of giving up a historically low mortgage rate to do a cash-out refinance is simply too high — often $500 to $1,000+ per month in additional payment burden for the life of the new loan.

The cash-out refinance earns its place when your existing mortgage rate is already high, when you need an exceptionally large amount of capital, when you are consolidating significant high-interest debt, or when you plan to stay in the home long enough to justify the closing costs and value the simplicity of a single consolidated payment above all else.

The most important thing you can do before making this decision is run your actual numbers. Know your current mortgage rate, know your existing balance, know how much equity you need, and model both options with real dollar outcomes.

Use our HELOC Payment Calculator to calculate your HELOC payment and total interest cost — then compare it honestly against what a cash-out refinance would cost you in monthly payment terms given your specific existing mortgage rate.