What is a HELOC? Complete Beginner’s Guide (2026)

If you own a home and need to borrow money, you have probably come across the term HELOC. Banks advertise it. Financial sites recommend it. But for most homeowners, the mechanics of how a HELOC actually works — and whether it makes sense for their situation — are far from obvious.

This guide breaks it all down in plain English. No jargon, no fluff. By the time you finish reading, you will know exactly what a HELOC is, how payments work, what it costs, and how to decide if it is the right move for you.

What is a HELOC?

A HELOC — short for Home Equity Line of Credit — is a revolving line of credit secured by your home. Think of it like a credit card, except the credit limit is based on the equity you have built up in your property, and the interest rate is significantly lower because your home backs the debt.

Unlike a traditional loan where you receive a lump sum upfront, a HELOC gives you a credit limit you can draw from as needed, repay, and borrow again — similar to how a credit card works. This flexibility is one of the main reasons homeowners choose a HELOC over other borrowing options.

The amount you can borrow depends on:

- Your home’s current market value

- How much you still owe on your mortgage

- Your lender’s maximum combined loan-to-value (CLTV) ratio, typically 80–85%

For example, if your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity. A lender allowing 85% CLTV would calculate your maximum HELOC limit like this:

$400,000 × 85% = $340,000 maximum combined debt $340,000 − $250,000 (existing mortgage) = $90,000 maximum HELOC

Want to see what your own credit limit might look like? Use our HELOC Payment Calculator to run the numbers for your home.

How Does a HELOC Work?

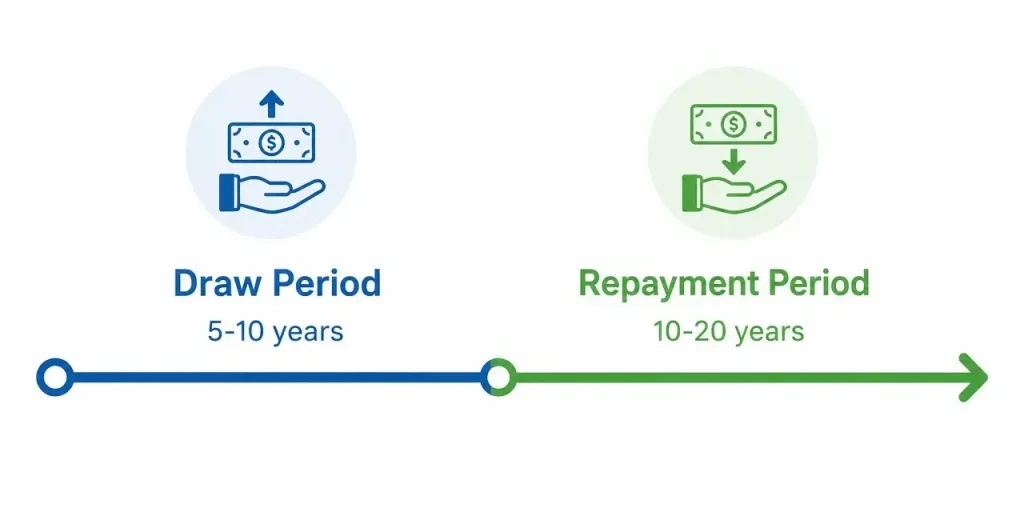

A HELOC has two distinct phases that every borrower needs to understand before signing anything.

The Draw Period

The draw period is the first phase — typically lasting 5 to 10 years. During this time, you can borrow from your credit line as needed, up to your approved limit. You only pay interest on the amount you actually use, not the full credit limit.

Most lenders require interest-only minimum payments during the draw period. So if your HELOC limit is $90,000 but you have only drawn $30,000 at a 7.5% interest rate, your minimum monthly payment would be roughly $188 — interest only, with no principal reduction required.

This is what makes HELOCs appealing for things like ongoing home renovations where costs come in stages. You draw money when you need it, pay interest only on what you use, and leave the rest untouched.

The Repayment Period

Once the draw period ends, the repayment period begins — typically lasting 10 to 20 years. During this phase:

- You can no longer draw new funds

- Your outstanding balance must be fully repaid

- Payments become fully amortized, meaning they cover both principal and interest

This is the point where many borrowers experience what is known as payment shock — a significant jump in monthly payments because you are now paying down the principal on top of interest. If you borrowed $60,000 during your draw period and your repayment period is 15 years at 7.5%, your new monthly payment would be around $556 compared to the interest-only minimum of roughly $375.

HELOC Interest Rates: What to Expect in 2026

HELOCs carry variable interest rates, which is one of the most important things to understand about this product.

Your rate is typically tied to the Wall Street Journal Prime Rate plus a margin set by your lender. For example:

Prime Rate (8.5%) + Lender Margin (0.5%) = 9.0% HELOC Rate

As the Federal Reserve adjusts its federal funds rate, the Prime Rate moves with it, and your HELOC rate moves too. This means your monthly payment can increase or decrease over time without any action on your part.

In a rising rate environment, this is a real risk. A $100,000 HELOC balance at 7% costs $583/month in interest. That same balance at 9.5% costs $792/month — a $209 monthly increase just from rate movement.

Some lenders offer rate caps that limit how high your HELOC rate can go over its lifetime, or periodic caps that limit how much it can move in a single year. Always ask your lender about rate caps before signing.

A small number of lenders also offer fixed-rate HELOCs or allow you to convert a portion of your balance to a fixed rate. These options sacrifice some flexibility but protect you from rate volatility.

What Can You Use a HELOC For?

A HELOC is one of the more flexible borrowing tools available to homeowners. Common uses include:

Home improvement and renovation — The most common use and often the most financially sound, since improvements can increase your home’s value. The IRS may also allow you to deduct HELOC interest if funds are used to substantially improve the home (consult a tax advisor for your specific situation).

Debt consolidation — Using a HELOC to pay off high-interest credit card debt can save significant money. Rolling $25,000 in credit card debt at 22% APR into a HELOC at 8.5% saves roughly $3,375 in annual interest. However, this converts unsecured debt into debt backed by your home — a risk worth understanding.

Education expenses — Some homeowners use HELOCs to fund college tuition, though federal student loan options should generally be explored first.

Emergency fund backup — Keeping an open HELOC with a zero balance gives you a financial safety net without paying interest until you actually need it.

Real estate investing — Experienced investors sometimes use HELOC funds as a down payment on investment properties. This is a higher-risk strategy that requires careful cash flow planning.

HELOC Costs and Fees

A HELOC is not free to open. Here are the costs you should expect:

| Cost | Typical Range |

|---|---|

| Application fee | $0 – $500 |

| Origination fee | 0% – 1% of credit limit |

| Appraisal fee | $300 – $700 |

| Title search fee | $100 – $300 |

| Annual fee | $25 – $100/year |

| Early termination fee | $200 – $500 (if closed within 2–3 years) |

Many lenders advertise “no closing cost HELOCs.” These do exist, but read the fine print — the lender often recoups those costs through a slightly higher interest rate or an early termination fee if you close the line within a specified period.

Total upfront closing costs for a HELOC typically range from $200 to $2,000, depending on your lender and loan size. This is considerably less than a full cash-out refinance, which often runs $3,000–$6,000 or more.

HELOC Requirements: Do You Qualify?

Lenders evaluate several factors when you apply for a HELOC. While requirements vary, here are typical thresholds across most major US lenders:

Credit score: Most lenders require a minimum score of 620, though the best rates go to borrowers with 720+. A score below 680 will likely mean higher rates or outright denial at some institutions.

Combined loan-to-value (CLTV): Most lenders cap CLTV at 80–85%. If your home has dropped in value or you have a large mortgage balance, you may have limited borrowing room.

Debt-to-income ratio (DTI): Lenders typically want your total monthly debt payments — including the projected HELOC payment — to stay below 43% of your gross monthly income. Some lenders allow up to 50% DTI for well-qualified borrowers.

Home equity: You generally need at least 15–20% equity in your home before any lender will approve a HELOC.

Stable income: You will need to document income through pay stubs, W-2s, or tax returns. Self-employed borrowers may face additional scrutiny.

HELOC vs. Home Equity Loan: What’s the Difference?

This is one of the most common points of confusion among homeowners.

A home equity loan gives you a lump sum at a fixed interest rate, repaid over a set term. Your payment is identical every month from day one.

A HELOC gives you a revolving credit line at a variable rate. You borrow what you need, when you need it, and payments fluctuate based on your balance and rate.

Choose a home equity loan if: You need a specific amount for a one-time expense (e.g., a roof replacement costing $18,000) and want payment predictability.

Choose a HELOC if: You have ongoing or unpredictable expenses (e.g., a kitchen renovation with costs spread over 12 months) and want flexibility.

A Real-World HELOC Example

Let’s walk through a complete example so the numbers feel concrete.

Homeowner profile:

- Home value: $450,000

- Mortgage balance: $280,000

- Credit score: 740

- Lender max CLTV: 85%

Step 1 — Calculate maximum HELOC: $450,000 × 85% = $382,500 $382,500 − $280,000 = $102,500 approved credit limit

Step 2 — Draw period payments: Homeowner draws $50,000 for a kitchen renovation at 8.75% rate Monthly interest-only payment = $50,000 × (8.75% ÷ 12) = $365/month

Step 3 — Repayment period: Draw period ends. Balance is $50,000 with 15-year repayment at 8.75% New monthly payment = $497/month (principal + interest)

The homeowner’s payment increased by $132/month at repayment — manageable if planned for in advance.

Use our HELOC Payment Calculator to model your own scenario with your actual numbers.

Is a HELOC Right for You?

A HELOC is a powerful borrowing tool, but it is not right for everyone. Here is a simple way to think about it:

A HELOC makes sense if:

- You have strong equity and a stable income

- You need flexible access to funds over time

- You are disciplined about repayment and won’t treat it as free money

- You are using it for something that adds value (home improvement) or saves money (debt consolidation at a lower rate)

Think twice if:

- Your income is variable or uncertain — a HELOC secured by your home means missed payments put your home at risk

- You are planning to sell the home within 1–2 years — closing costs and early termination fees may not be worth it

- You cannot comfortably absorb a rate increase — stress-test your budget assuming a 2% rate increase before committing

- You tend to overspend when credit is available — a revolving credit line requires financial discipline

The Bottom Line

A HELOC is one of the lowest-cost ways for a homeowner to access capital. Done right — borrowed for the right reasons, with a clear repayment plan — it can save money, fund valuable improvements, and provide genuine financial flexibility.

The key is going in with eyes open: understanding that your rate will change, that payment shock is real when the repayment period begins, and that your home is the collateral backing every dollar you borrow.

Ready to see what your HELOC payments would actually look like? Use our free HELOC Payment Calculator to model your draw amount, rate, and repayment schedule in minutes.