HELOC vs. Reverse Mortgage: What’s the Difference?

If you are a homeowner aged 62 or older sitting on significant home equity, you have likely encountered two very different products pitched as ways to access that equity: a HELOC and a reverse mortgage. Financial advisors recommend them. Lenders advertise them. And the decision between them — or against both — is one of the most consequential financial choices a senior homeowner can make.

These two products could not be more different in structure, cost, risk, and long-term financial impact. One requires monthly payments and preserves your equity. The other requires no monthly payments but gradually consumes your equity over time. One is straightforward and widely understood. The other is one of the most complex financial products sold to consumers, with a history of misuse and borrower confusion.

This article gives you an honest, complete comparison — with no sales pitch for either product — so you can evaluate both options with full information.

Who This Comparison Is For

This comparison is primarily relevant to homeowners aged 62 and older — the minimum age to qualify for a Home Equity Conversion Mortgage (HECM), the federally insured reverse mortgage product backed by the Federal Housing Administration (FHA).

Younger homeowners considering home equity access should focus on HELOCs, home equity loans, and cash-out refinancing rather than reverse mortgages, as the age requirement makes reverse mortgages unavailable to them.

For homeowners 62 and older, both products are potentially available, which makes the comparison genuinely relevant.

How Each Product Works

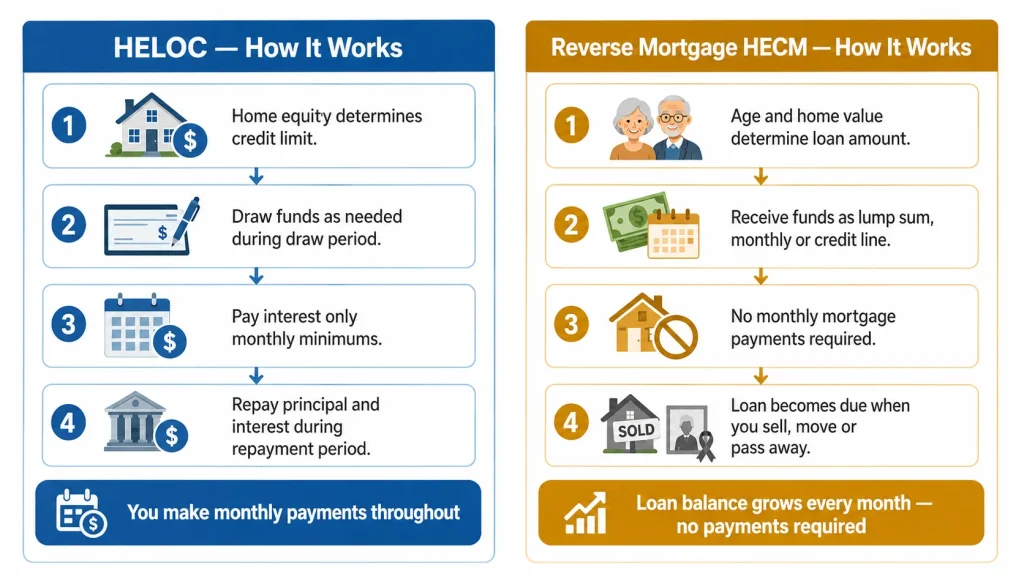

HELOC: A Revolving Credit Line With Monthly Payments

A HELOC gives you access to a revolving line of credit based on your home equity, at a variable interest rate, with a draw period typically lasting 5 to 10 years followed by a repayment period of 10 to 20 years.

During the draw period, you can borrow as needed up to your credit limit and make interest-only minimum payments. During the repayment period, your payments become fully amortized — covering both principal and interest.

The key feature: you make monthly payments throughout the life of the HELOC. Your balance can grow or shrink depending on how you use it, and your home equity is preserved or reduced based on your borrowing behavior.

Reverse Mortgage: No Monthly Payments, Growing Loan Balance

A reverse mortgage — specifically the Home Equity Conversion Mortgage (HECM) insured by the FHA — allows homeowners 62 and older to convert home equity into cash without making monthly mortgage payments.

Instead of you paying the lender each month, the loan balance grows over time as interest accrues and is added to what you owe. You receive money from the lender — as a lump sum, a monthly payment, a line of credit, or a combination — and the loan does not become due until one of the following trigger events occurs:

- You sell the home

- You permanently move out of the home

- You pass away

- You fail to maintain the home, pay property taxes, or keep homeowner’s insurance current

At that point, the loan balance — original principal plus all accrued interest — must be repaid, typically from the proceeds of selling the home.

The key feature: You make no monthly mortgage payments, but your loan balance grows every month and your equity shrinks — sometimes significantly — over time.

Eligibility Requirements: Who Qualifies for Each

HELOC Eligibility

- Age: No minimum age requirement

- Home equity: At least 15–20% equity in the property

- Credit score: Minimum 620, with 680+ for competitive rates

- Income: Must document sufficient income to cover monthly payments

- DTI ratio: Below 43% including the projected HELOC payment

- Primary or secondary residence: Most lenders accept both

Reverse Mortgage (HECM) Eligibility

- Age: All borrowers on the title must be at least 62

- Primary residence only: Must be your principal residence — no investment properties or vacation homes

- Home equity: Substantial equity required — the older you are and the more equity you have, the more you can access

- HUD counseling: Required — you must complete a counseling session with a HUD-approved housing counselor before proceeding

- Property taxes and insurance: Must be current and you must agree to keep them current

- Property type: Single-family homes, FHA-approved condos, and some manufactured homes qualify

The HUD counseling requirement is not optional. It is federally mandated and exists specifically because reverse mortgages are complex products with significant consequences that borrowers have historically misunderstood.

How Much You Can Access: Loan Limits Compared

HELOC Credit Limit

Your HELOC credit limit is determined by your equity position and your lender’s maximum combined loan-to-value (CLTV) ratio, typically 80–85%.

For a home worth $500,000 with a $150,000 remaining mortgage: $500,000 × 85% = $425,000 − $150,000 = $275,000 maximum HELOC

Your income and DTI ratio also factor in — high equity alone does not guarantee a large HELOC if your income cannot support the repayment.

Reverse Mortgage Loan Limit

The amount you can access through a HECM reverse mortgage is calculated differently and depends on three factors:

- Your age (or the age of the youngest borrower on the title): Older borrowers can access more

- Your home’s appraised value (up to the 2026 HECM loan limit of $1,209,750)

- Current interest rates: Lower rates allow access to more equity

The FHA publishes a Principal Limit Factor (PLF) table that determines what percentage of your home’s value you can access. In 2026, a 70-year-old borrower might access 45–55% of their home’s value. A 75-year-old might access 50–60%.

For a home worth $500,000 with no existing mortgage, a 72-year-old borrower might access approximately $240,000–$265,000 — less than the HELOC example above because the reverse mortgage PLF limits access more conservatively.

If you have an existing mortgage, it must be paid off at closing — typically from the reverse mortgage proceeds. A significant existing mortgage balance can meaningfully reduce how much cash you receive.

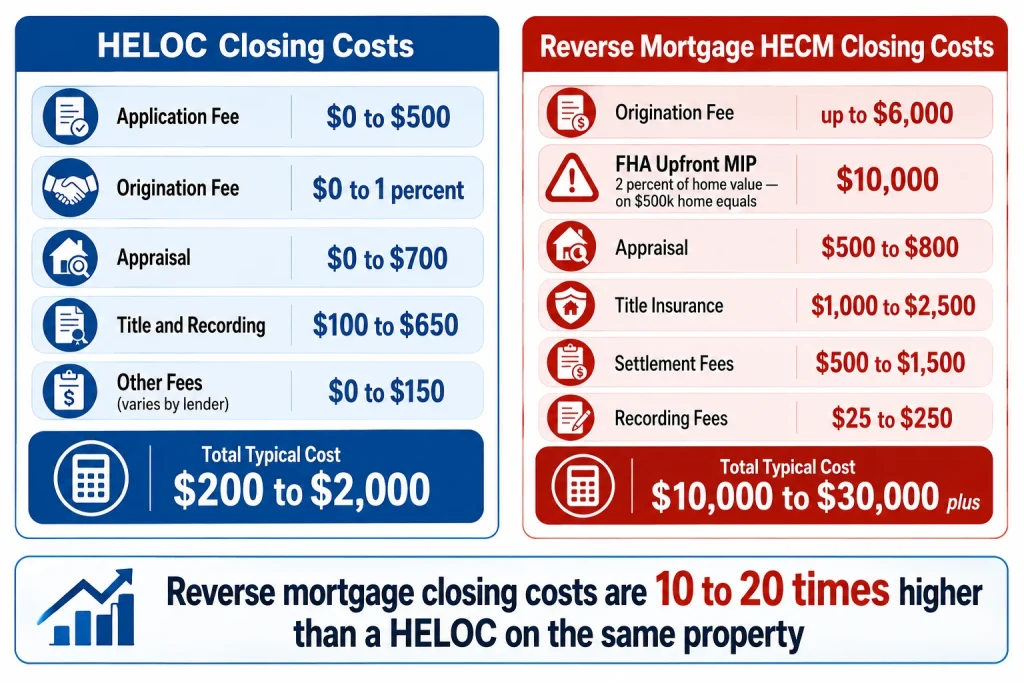

Costs: A Significant Difference

Both products have costs, but the reverse mortgage is dramatically more expensive to initiate.

HELOC Costs

| Cost Item | Typical Range |

|---|---|

| Application fee | $0 – $500 |

| Origination fee | $0 – 1% of credit limit |

| Appraisal | $0 – $700 |

| Title and recording fees | $100 – $650 |

| Total typical closing costs | $200 – $2,000 |

| Annual fee | $0 – $100/year |

Reverse Mortgage (HECM) Costs

| Cost Item | Typical Range |

|---|---|

| Origination fee | Up to $6,000 (FHA regulated) |

| FHA mortgage insurance premium (upfront) | 2% of home value (up to HECM limit) |

| Appraisal | $500 – $800 |

| Title insurance | $1,000 – $2,500 |

| Settlement/closing fees | $500 – $1,500 |

| Recording fees | $25 – $250 |

| Total typical closing costs | $10,000 – $30,000+ |

| Annual FHA mortgage insurance | 0.50% of loan balance per year |

On a $500,000 home, the upfront FHA mortgage insurance premium alone is $10,000 (2% × $500,000). Add the origination fee of up to $6,000, title insurance, and other fees, and total closing costs on a reverse mortgage routinely reach $15,000 to $25,000.

This is 10 to 20 times the closing cost of a HELOC on the same property. The reverse mortgage’s upfront cost structure is one of the most significant — and least discussed — aspects of the product.

Some lenders offer no-closing-cost reverse mortgages where fees are rolled into the loan balance. This feels attractive upfront but means the costs accrue interest over the life of the loan, ultimately costing significantly more.

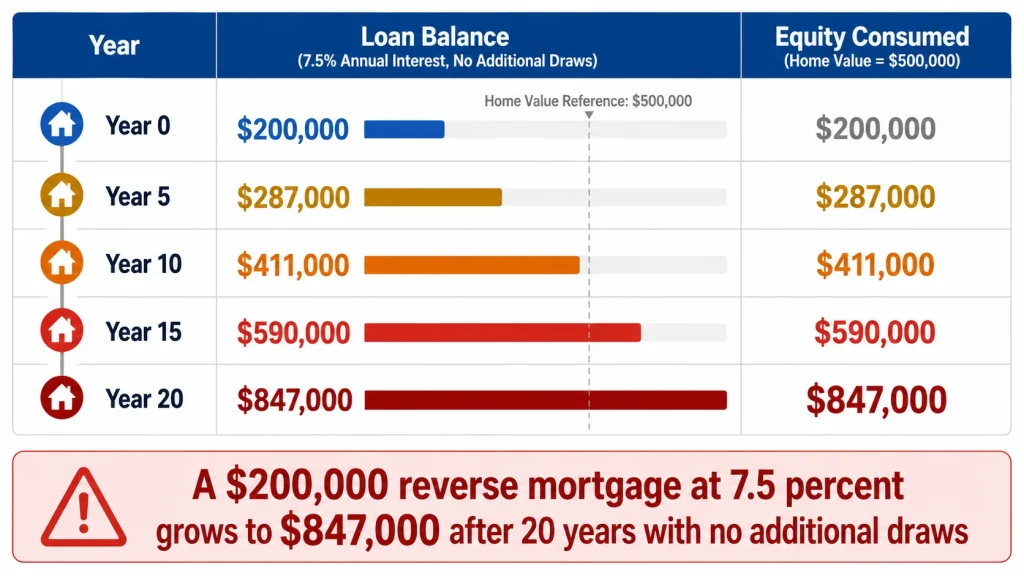

The Growing Balance Problem: Reverse Mortgage Equity Erosion

This is the most important concept to understand about a reverse mortgage — and the one most frequently misunderstood by borrowers.

With a HELOC, your balance grows only when you draw funds and shrinks when you make payments. You have complete control over the trajectory.

With a reverse mortgage, your loan balance grows every single month whether you draw new funds or not — because interest is being added to the outstanding balance continuously. In the early years this growth is modest. Over a decade or two, it becomes significant.

Here is what happens to a $200,000 reverse mortgage balance at a 7.5% interest rate with no new draws:

| Year | Loan Balance | Approximate Equity Consumed |

|---|---|---|

| Year 0 (at closing) | $200,000 | $200,000 |

| Year 5 | $287,000 | $287,000 |

| Year 10 | $411,000 | $411,000 |

| Year 15 | $590,000 | $590,000 |

| Year 20 | $847,000 | $847,000 |

On a home worth $500,000 at closing, a $200,000 reverse mortgage balance grows to $590,000 after 15 years — consuming $390,000 more in equity through interest accrual alone, with no additional draws. By year 20, the balance may exceed the home’s value entirely, depending on appreciation.

The FHA mortgage insurance guarantees that you will never owe more than the home is worth — the FHA absorbs any shortfall when the home sells. This protection is real and valuable. But it does not change the fact that equity is being steadily consumed, which directly affects what you — or your heirs — will have left when the home is eventually sold.

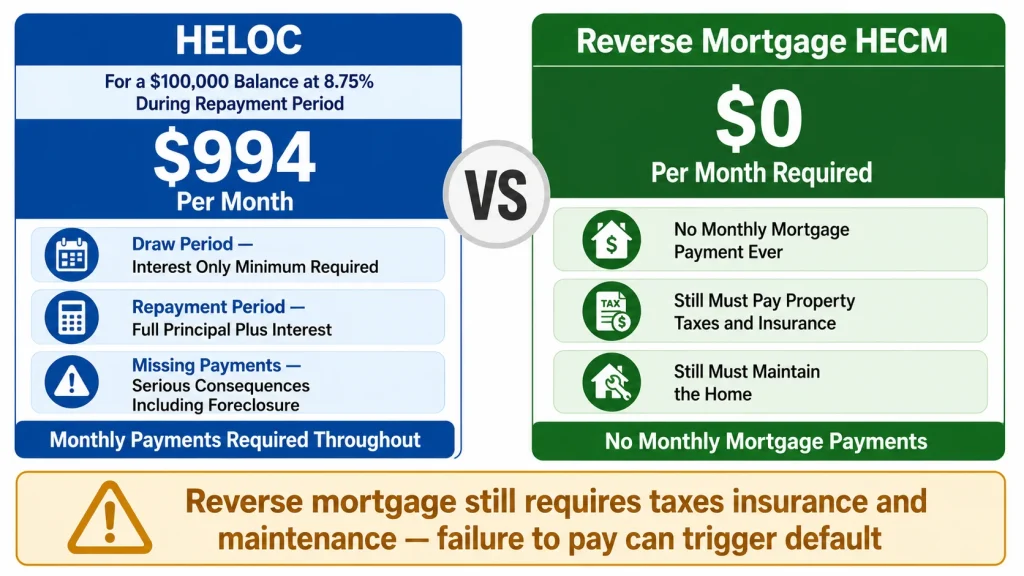

Monthly Payments: The Core Lifestyle Difference

HELOC: Monthly Payments Required

A HELOC requires monthly payments throughout its life. During the draw period, at minimum you must pay the interest accrued that month. During the repayment period, you must make full principal-plus-interest payments.

For a retired homeowner on a fixed income, these monthly payment obligations can be a meaningful budget burden — particularly during the repayment period when payments jump significantly. A $100,000 HELOC balance entering a 15-year repayment at 8.75% requires approximately $994/month.

The monthly payment requirement is the primary practical reason many senior homeowners consider a reverse mortgage as an alternative.

Reverse Mortgage: No Monthly Mortgage Payments

A reverse mortgage requires no monthly mortgage payments for as long as you live in the home. This is not a waiver or a deferral — it is a structural feature of the product.

You are still responsible for property taxes, homeowner’s insurance, and home maintenance. Failure to keep these current is a default condition that can trigger the loan becoming due. These obligations are non-negotiable and have caused real problems for borrowers who did not fully understand them.

But the elimination of a monthly mortgage payment can be genuinely transformative for a homeowner on a fixed retirement income. Converting home equity to income without a monthly payment obligation changes the retirement cash flow picture significantly.

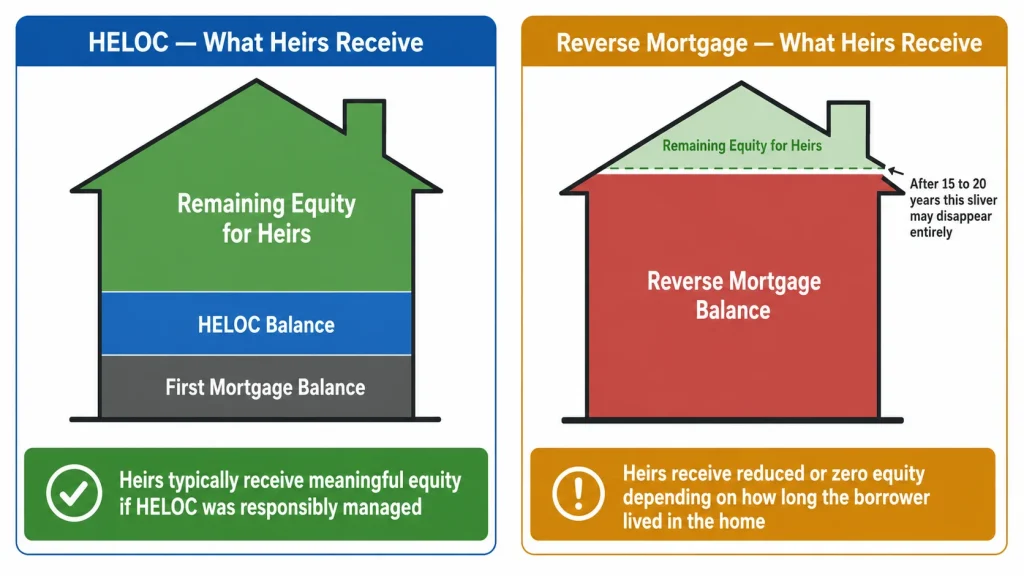

What Happens to the Home: Inheritance and Estate Considerations

This is often the most emotionally significant dimension of the comparison for senior homeowners.

HELOC and Home Inheritance

A HELOC is a standard second mortgage. When you pass away:

- The HELOC balance is a debt against the estate

- Heirs can sell the home, pay off the HELOC from proceeds, and keep any remaining equity

- Heirs can also refinance the HELOC into their own mortgage if they want to keep the home

- The equity remaining after paying off the HELOC and any first mortgage belongs to the estate

If you have been paying down your HELOC responsibly, there may be substantial equity remaining for heirs.

Reverse Mortgage and Home Inheritance

When the last borrower passes away or permanently leaves the home, the reverse mortgage becomes due. Heirs typically have 6 to 12 months to:

- Pay off the loan balance and keep the home (they must refinance or pay cash)

- Sell the home and keep any equity remaining after the loan balance is repaid

- Walk away if the loan balance exceeds the home’s value — the FHA insurance covers the difference, and heirs owe nothing beyond the home

The practical reality for many heirs: if the borrower lived in the home for 15–20 years with a reverse mortgage, the loan balance may have grown to consume most or all of the home’s equity. Heirs receive little to nothing from the estate beyond what the home is worth minus the reverse mortgage balance.

For homeowners who want to leave home equity to children or other heirs, a reverse mortgage is a significant concern. For homeowners whose priority is maximizing their own retirement income and comfort — with no strong interest in leaving home equity as inheritance — the reverse mortgage’s equity consumption may be an acceptable trade.

Tax Treatment

Both products have similar tax treatment in most respects.

HELOC interest: May be deductible when funds are used to buy, build, or substantially improve the home, subject to IRS limits. Interest on funds used for other purposes is not deductible.

Reverse mortgage proceeds: Not taxable income. Funds received from a reverse mortgage are loan proceeds, not income, and therefore not subject to federal income tax. However, the interest that accrues on the reverse mortgage balance is not deductible until the loan is paid off — which typically occurs at sale or death.

Important caveat: Reverse mortgage proceeds that sit in a bank account can potentially affect eligibility for means-tested government programs like Medicaid and Supplemental Security Income (SSI). This is a complex area requiring guidance from a benefits counselor or elder law attorney for homeowners who receive or may need these benefits.

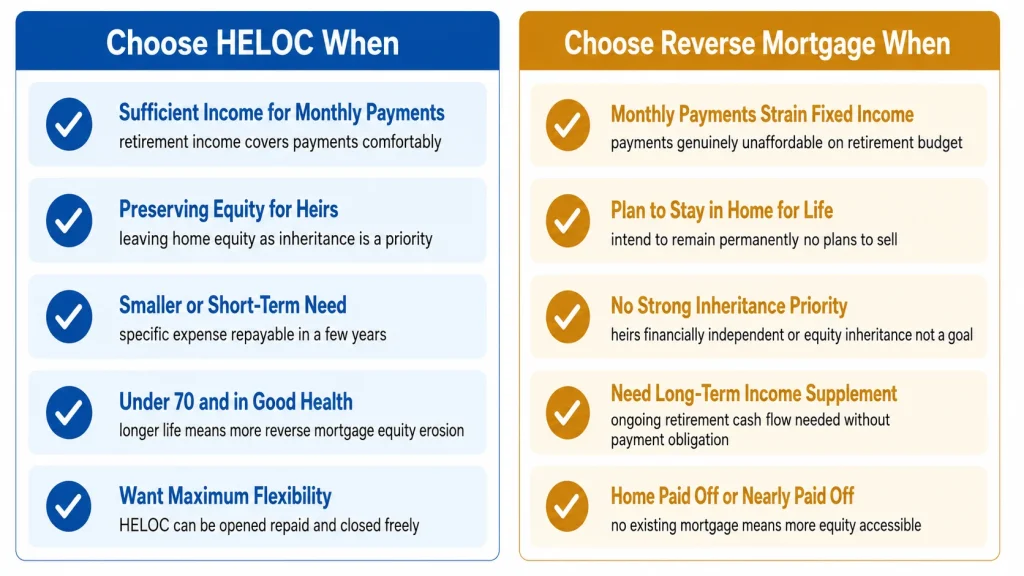

When a HELOC Makes More Sense for Seniors

You have sufficient income to make monthly payments comfortably. If your retirement income — Social Security, pension, investment withdrawals — can support HELOC payments without strain, the HELOC’s lower cost and equity preservation make it the better financial tool.

You want to preserve equity for heirs. If leaving home equity to children or other beneficiaries is a priority, a HELOC that you actively repay preserves far more equity than a reverse mortgage.

You need a smaller or short-term amount. For a specific home repair, a medical expense, or a one-time need you can repay within a few years, a HELOC’s lower cost structure is far more efficient than a $15,000–$25,000 reverse mortgage closing cost.

You want to maintain maximum flexibility. A HELOC can be opened, used, repaid, and closed. A reverse mortgage is a long-term commitment with significant exit costs.

You are under 70 and in good health. The longer you live with a reverse mortgage, the more equity it consumes. A younger senior in good health who takes a reverse mortgage may find the loan balance has grown enormously by the time the home eventually sells.

When a Reverse Mortgage Makes More Sense

Your retirement income does not comfortably cover monthly HELOC payments. If adding a HELOC payment would genuinely strain your fixed income budget, the reverse mortgage’s no-payment structure may be the more sustainable choice.

You plan to stay in the home for life. A reverse mortgage makes the most financial sense when you intend to remain in the home permanently. The equity erosion is less relevant if you never plan to sell.

You have no heirs or your heirs are financially independent. If leaving home equity as inheritance is not a priority, the equity consumption of a reverse mortgage is purely a financial calculation about your own retirement income needs.

You need to supplement retirement income over the long term. A reverse mortgage configured as a monthly payment or a growing line of credit can function as a long-term retirement income supplement in ways a HELOC cannot — without any repayment obligation.

Your home is paid off or nearly paid off. With no existing mortgage or a very small balance, a reverse mortgage can convert a large portion of your home’s value to accessible equity while eliminating any existing mortgage payment entirely.

The Hybrid Approach: HELOC First, Reverse Mortgage Later

Some financial planners recommend a sequenced approach for senior homeowners:

Use a HELOC in your 60s and early 70s while you have sufficient income to make payments and the ability to qualify on income and credit. Preserve the reverse mortgage as a later-stage option if retirement income gaps emerge, health declines, or the HELOC becomes unmanageable.

This approach preserves the lower-cost option while you can use it and keeps the reverse mortgage available as a safety net if circumstances change.

Side-by-Side Comparison Summary

| Factor | HELOC | Reverse Mortgage (HECM) |

|---|---|---|

| Minimum age | None | 62 |

| Monthly payments | Required | Not required |

| Loan balance over time | Borrower controlled | Grows continuously |

| Upfront closing costs | $200 – $2,000 | $10,000 – $30,000+ |

| Ongoing costs | Annual fee up to $100 | 0.50% annual FHA MIP |

| Equity impact | Preserved with repayment | Steadily consumed |

| Home as collateral | Yes | Yes |

| Counseling required | No | Yes — HUD mandated |

| Primary residence required | No — second homes OK | Yes — primary only |

| Heirs receive equity | Typically yes | Reduced or none |

| Income requirement | Yes — must qualify | Minimal — no payment to cover |

| Best for | Seniors with stable income | Seniors needing payment relief |

The Bottom Line

A HELOC and a reverse mortgage are not competing versions of the same product — they are fundamentally different tools designed for different financial situations.

A HELOC is the right tool when you can afford monthly payments, want to preserve equity, need a smaller or short-term amount, or want to keep your financial options open. It is lower cost, more flexible, and preserves more wealth long-term for borrowers who manage it responsibly.

A reverse mortgage is the right tool when monthly payments are genuinely unaffordable on a fixed retirement income, you plan to stay in the home for the rest of your life, inheritance of home equity is not a priority, and you need a long-term income supplement without payment obligations. The dramatically higher cost and equity erosion are the trade for eliminating monthly payment risk.

Neither product is appropriate for every senior homeowner. The right answer requires honest assessment of your income, your health outlook, your heirs’ expectations, your long-term housing plans, and your tolerance for financial complexity.

If you are considering a reverse mortgage, the federally mandated HUD counseling session is genuinely valuable — not a box to check but an education worth completing. For both products, consulting with a fee-only financial advisor who has no commission interest in which product you choose is the most reliable way to get objective guidance.

Use our HELOC Payment Calculator to model your HELOC payment and total interest cost — giving you a concrete comparison point for evaluating what a HELOC would actually cost you relative to the reverse mortgage alternative.