Using a HELOC to Buy Another Property

Using a HELOC to buy another property is one of the most aggressive — and potentially rewarding — ways a homeowner can deploy home equity. It is also one of the riskiest. You are leveraging one asset to acquire another, stacking two property-related debt obligations on top of each other, and betting that the second property generates enough return to justify the cost and risk of borrowing against your primary home to fund it.

Done with the right property, the right numbers, and the right financial foundation, it works. Done carelessly, it can put both your primary home and your investment at risk simultaneously.

This guide covers how the strategy works, the real costs involved, the cash flow math you need to run before committing, the tax landscape in 2026, and the specific situations where this approach makes financial sense — and where it does not.

How It Works: Using a HELOC as a Down Payment or Full Purchase

There are two primary ways homeowners use a HELOC to acquire another property.

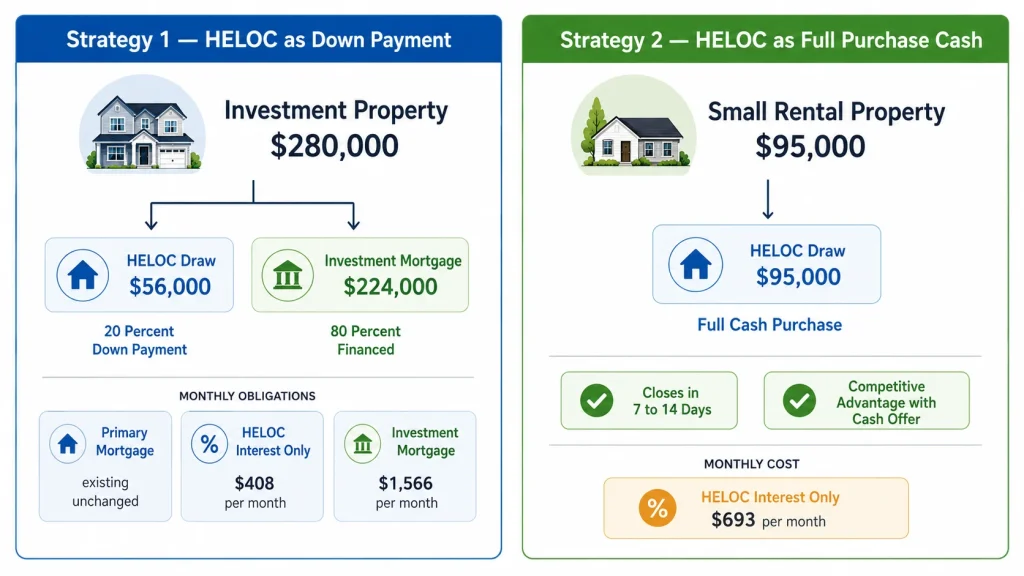

Strategy 1: HELOC as a Down Payment

The most common approach. You draw from your HELOC to fund the down payment on a new property — typically 20–25% of the purchase price for an investment property — then obtain a separate mortgage for the remaining balance.

Example:

- Investment property purchase price: $280,000

- Down payment required (20%): $56,000

- HELOC draw: $56,000

- Investment property mortgage: $224,000 at 7.5% (30-year fixed)

Your debt structure after purchase:

- Primary home mortgage: existing balance + payments continue

- HELOC on primary home: $56,000 at 8.75% variable

- Investment property mortgage: $224,000 at 7.5% fixed

Monthly obligations:

- Primary mortgage payment: (existing, unchanged)

- HELOC interest-only minimum: $408/month

- Investment property mortgage: $1,566/month

This strategy works when the investment property generates enough rental income to cover its own mortgage, the HELOC payment, and still produce positive cash flow.

Strategy 2: HELOC as Full Purchase Price (All-Cash Acquisition)

For lower-priced properties — a small rental, a mobile home park lot, a rural property — some investors use a large HELOC to buy outright without a separate mortgage. This simplifies the transaction and can be attractive to sellers who prefer cash buyers.

Example:

- Small rental property purchase price: $95,000

- HELOC draw: $95,000 at 8.75%

- Interest-only minimum payment: $693/month

This approach works only when the rental income comfortably exceeds the HELOC interest cost, with room for vacancy, maintenance, and property management expenses.

All-cash purchases via HELOC also close faster than financed transactions — sometimes in 7 to 14 days — which can give you a competitive advantage in markets where sellers prioritize certainty and speed over price.

The Full Cost Picture: What You Are Actually Taking On

Before running any investment analysis, you need to understand every financial obligation this strategy creates.

Cost Layer 1: HELOC Closing Costs

Opening a HELOC costs $200 to $2,000 depending on your lender, home value, and state. These are one-time upfront costs paid regardless of whether the property purchase succeeds.

Cost Layer 2: HELOC Interest on the Down Payment

The $56,000 HELOC draw for a down payment costs $408/month in interest-only payments at 8.75%. That is $4,900/year in interest on the down payment alone — a cost that does not appear on the investment property’s income statement but absolutely belongs in your investment analysis.

This is the most commonly overlooked cost in HELOC-funded property acquisitions. Investors calculate the investment property’s cash flow against its own mortgage but forget to include the HELOC interest cost that funded the down payment. That omission overstates the investment’s profitability by hundreds of dollars per month.

Cost Layer 3: Investment Property Mortgage Payments

The $224,000 mortgage at 7.5% on a 30-year fixed costs $1,566/month — $18,792/year. This is your largest ongoing obligation from the investment.

Cost Layer 4: Investment Property Operating Costs

Every rental property has operating costs beyond the mortgage. A realistic model includes:

- Property taxes: typically 1–1.5% of purchase price annually

- Insurance: $1,000–$2,500/year for a typical rental

- Maintenance and repairs: 1–2% of property value annually (budget more for older properties)

- Property management: 8–12% of gross rent if using a manager

- Vacancy allowance: 5–10% of gross rent (budget for periods without a tenant)

- Capital expenditure reserves: $100–$200/month for roof, HVAC, appliances

For a $280,000 investment property, realistic annual operating costs excluding the mortgage are $8,000–$14,000.

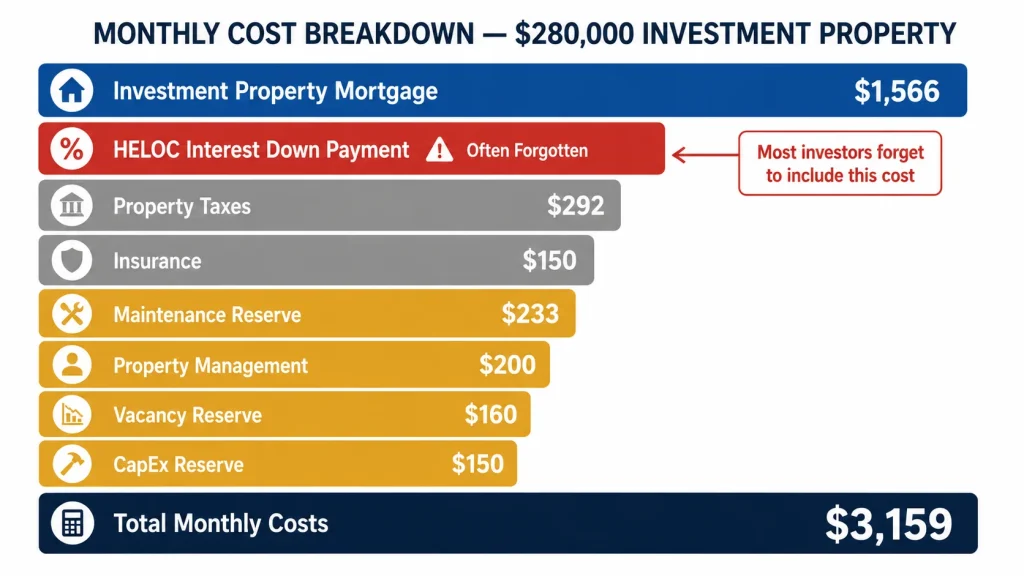

The Complete Monthly Cost Stack

For the $280,000 investment property example:

| Cost | Monthly Amount |

|---|---|

| Investment property mortgage | $1,566 |

| HELOC interest (down payment) | $408 |

| Property taxes | $292 (estimated) |

| Insurance | $150 |

| Maintenance reserve | $233 |

| Property management (10%) | $200 (on $2,000 rent) |

| Vacancy reserve (8%) | $160 |

| CapEx reserve | $150 |

| Total monthly costs | $3,159 |

For this investment to break even, it must generate $3,159/month in gross rent. To produce positive cash flow — the actual goal — it needs to generate meaningfully more than that.

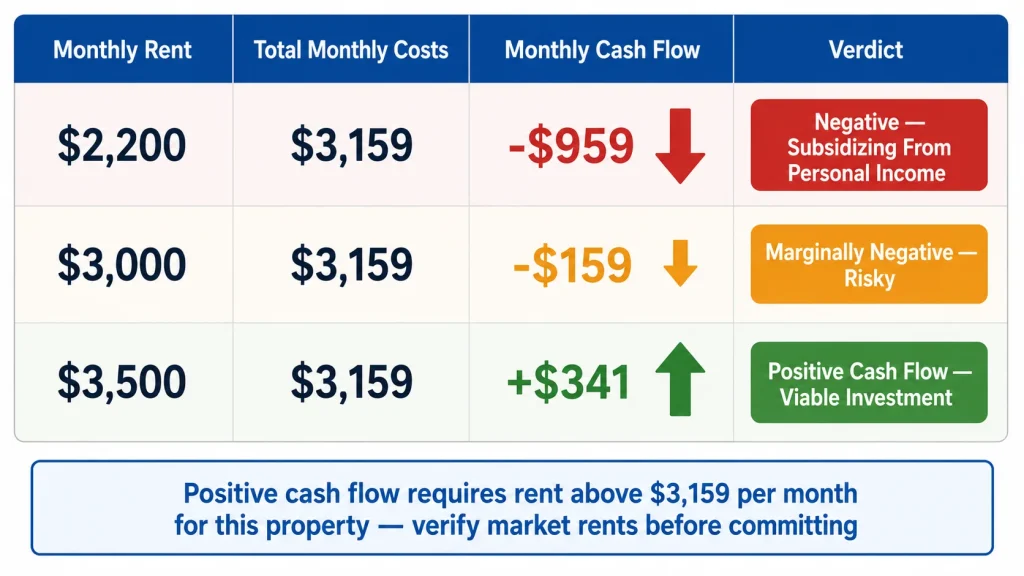

The Cash Flow Calculation: The Most Important Number

Positive cash flow is the foundation of a sound rental property investment. Without it, you are subsidizing the property from your personal income — which is a viable strategy in appreciating markets but a financially stressful one if the appreciation does not materialize as expected.

Cash flow formula:

Monthly Cash Flow = Gross Rent − All Monthly Costs (including HELOC interest)

For the $280,000 property example:

If market rent is $2,200/month: $2,200 − $3,159 = −$959/month negative cash flow

If market rent is $3,000/month: $3,000 − $3,159 = −$159/month marginally negative

If market rent is $3,500/month: $3,500 − $3,159 = +$341/month positive cash flow

This is why property selection and local market rent analysis are critical before committing to this strategy. A property that produces $341/month in positive cash flow is a functional rental investment. A property that loses $959/month requires you to subsidize it from personal income — which means your primary home equity is funding a negative-cash-flow asset.

Use our HELOC Payment Calculator to model your HELOC interest cost at different draw amounts so you can include the correct number in your cash flow analysis.

The Debt-to-Income Challenge: Qualifying for the Investment Mortgage

When you apply for a mortgage on an investment property, lenders evaluate your total debt-to-income ratio — including your primary mortgage, your HELOC payment, and the new investment property mortgage.

Lenders typically allow a maximum DTI of 43–50% for investment property mortgages. If adding the HELOC draw payment and the investment property mortgage pushes your DTI above this threshold, you may not qualify for the investment property mortgage at all — regardless of how strong the investment looks on paper.

Example DTI calculation:

Gross monthly income: $12,000 Existing obligations:

- Primary mortgage: $2,100

- HELOC minimum (interest-only on $56,000): $408

- Credit cards/other debts: $300

- New investment property mortgage: $1,566

Total monthly debt: $4,374 DTI: $4,374 ÷ $12,000 = 36.4% — within most lender limits

If the same borrower had a $3,200 primary mortgage instead of $2,100, the DTI would be 40.4% — still acceptable but leaving little margin.

Many lenders will credit 75% of expected rental income toward your income in the DTI calculation — which can meaningfully improve your qualification numbers. But this credit typically requires a signed lease or, for a property you have not yet rented, an appraiser’s market rent opinion.

Investment Property Mortgage: Higher Rates and Stricter Terms

Investment property mortgages carry higher interest rates than primary residence mortgages — typically 0.50% to 0.875% higher. In 2026, if a primary residence mortgage is available at 7.0%, an investment property mortgage on the same property profile is more likely at 7.50%–7.875%.

Lenders also typically require:

- Minimum 20–25% down payment — no low-down-payment programs like FHA or USDA for investment properties

- Credit score 680+ — most competitive rates require 720+

- 6 months cash reserves — many lenders require documented reserves equal to 6 months of mortgage payments on all properties you own, not just the investment property

- Proof of rental income or market rent appraisal for new purchases

The 6-month reserve requirement is often the tightest constraint. If you draw $56,000 from your HELOC for the down payment and that depletes most of your liquid savings, you may fail the reserve requirement even if your income and credit are strong.

Plan your reserve position carefully before initiating the HELOC draw.

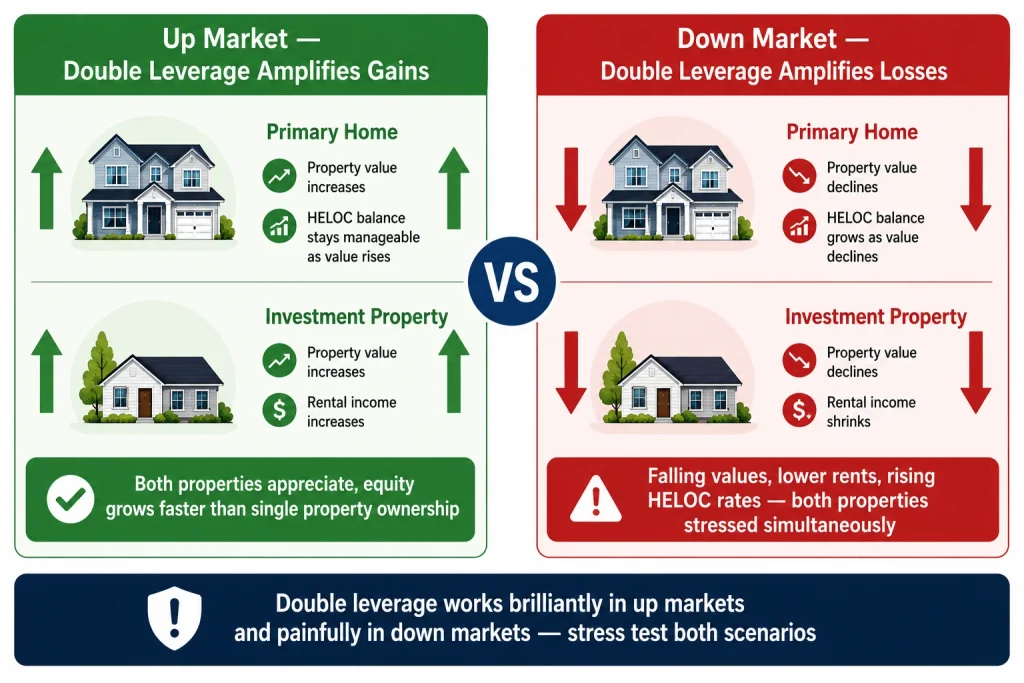

The Double Leverage Risk

This is the most important risk concept to understand when using a HELOC to buy property.

Standard real estate investing involves one layer of leverage — the mortgage on the investment property. Using a HELOC to fund the down payment adds a second layer of leverage on top. You are now leveraged on two properties simultaneously, with one of them (your primary home) serving as collateral for both its own mortgage and the HELOC.

In a normal market, double leverage amplifies your returns. If both properties appreciate, your equity grows faster than it would with either property alone. You built two assets with the equity of one.

In a market downturn, double leverage amplifies your losses. If property values fall and rental income drops, you may face:

- Negative cash flow on the investment property

- Falling value on both properties simultaneously

- HELOC variable rate increasing your interest costs just as income pressure increases

- Potential inability to sell the investment property for enough to cover its mortgage

The 2008–2010 housing crisis included many homeowners in exactly this position — leveraged on multiple properties via home equity lines — who lost both their primary home and their investment properties when values dropped and rental income fell.

The risk is real. Market cycles happen. Double leverage works brilliantly in an up market and painfully in a down market. Your financial plan should include a stress test for the down scenario.

Tax Implications: What Changes When You Use HELOC for Investment Property

The tax picture for a HELOC used to purchase investment property is meaningfully different from a renovation HELOC and worth understanding clearly.

HELOC Interest Deductibility

Under current IRS rules, HELOC interest is deductible only when funds are used to buy, build, or substantially improve the home securing the HELOC — your primary residence. Using HELOC funds to purchase a different investment property does not qualify for the mortgage interest deduction on Schedule A.

However, the HELOC interest used to fund the investment property may be deductible as a business expense on Schedule E (for rental income) — because it is interest paid on money used to acquire a rental asset. This is a different deduction pathway with different rules.

The IRS tracing rules apply: the deductibility of the HELOC interest follows the use of the funds, not the security for the loan. Interest on funds used for investment purposes generally qualifies as investment interest or rental expense.

This is a complex area with significant consequences for your tax return. Work with a CPA or tax advisor who has experience with rental property before making any deductibility assumptions.

Rental Income Taxation

Rental income from the investment property is taxable ordinary income. However, several deductions reduce your taxable rental income:

- Mortgage interest on the investment property mortgage

- HELOC interest attributable to the investment (subject to the tracing rules above)

- Property taxes

- Insurance

- Maintenance and repairs

- Depreciation (a powerful non-cash deduction that reduces taxable income without actual cash outflow)

Depreciation alone — the IRS allows you to depreciate residential rental property over 27.5 years — can shelter a significant portion of rental income from taxation. On a $280,000 property with a land value of $60,000 (structures only depreciate), the annual depreciation deduction is $220,000 ÷ 27.5 = $8,000/year.

This $8,000 annual depreciation deduction directly reduces your taxable rental income — a meaningful tax benefit that does not appear in the cash flow statement but improves the investment’s after-tax economics.

Passive Activity Rules

Rental income and losses are generally classified as passive activity. Passive losses can only offset passive income — you cannot use a rental property’s operating loss to reduce your W-2 income unless you qualify as a real estate professional under IRS rules or your adjusted gross income is below $100,000 (with phase-out between $100,000 and $150,000).

When This Strategy Makes Financial Sense

Using a HELOC to acquire another property makes the strongest financial sense when all of the following conditions apply:

Strong equity position on primary home. You have enough equity that the HELOC draw leaves you with at least 20–25% remaining equity in your primary home — not stretched to the maximum CLTV limit.

Positive or near-positive cash flow on the investment. The rental income, after all costs including HELOC interest, produces positive or break-even monthly cash flow. Negative cash flow investments require ongoing personal income subsidies that may not be sustainable.

Stable, documented income. Your DTI remains within acceptable limits after accounting for all debt obligations including the HELOC and investment mortgage.

Adequate cash reserves. You retain at least 6 months of combined mortgage payments (all properties) in liquid savings after funding the down payment. Do not deplete your reserves to make the deal work.

A specific, researched property in a stable market. Not a speculative purchase in a declining market or a property with significant deferred maintenance that could produce large surprise expenses.

Variable rate tolerance. You can absorb HELOC rate increases of 1–2% without the investment becoming unworkable.

When It Does Not Make Sense

Avoid this strategy when:

- The investment property produces negative cash flow under realistic assumptions — you are counting on appreciation alone

- Drawing the HELOC would leave your primary home with less than 20% equity

- Your DTI would exceed 45% after all obligations

- You do not have 6 months of cash reserves remaining after the down payment

- You are already in or near the HELOC repayment period with a significant balance

- Interest rates on both the HELOC and investment property mortgage significantly exceed the rental yield

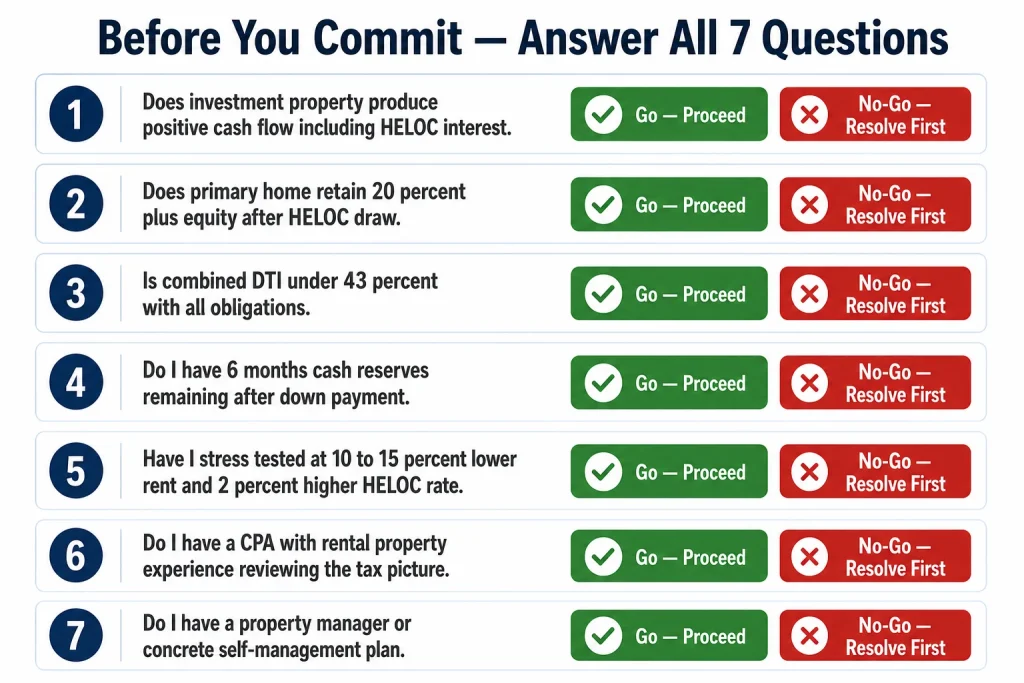

A Simple Go/No-Go Checklist

Before committing to this strategy, work through these seven questions:

- Does the investment property produce positive monthly cash flow after including HELOC interest in the cost stack? → If no, understand what you are subsidizing and why.

- Does my primary home retain 20%+ equity after the HELOC draw? → If no, find a different down payment source or a lower-priced property.

- Is my combined DTI under 43% with all three obligations? → If no, you may not qualify for the investment mortgage.

- Do I have 6 months of cash reserves remaining after the down payment? → If no, rebuild reserves before proceeding.

- Have I stress-tested the investment at 10–15% lower rent and 2% higher HELOC rate? → If the numbers collapse under modest stress, the margin of safety is insufficient.

- Do I have a CPA with rental property experience reviewing the tax picture? → If no, get one before closing.

- Do I have a property manager or a concrete self-management plan? → If no, unmanaged rentals frequently underperform financial projections.

The Bottom Line

Using a HELOC to buy another property is a legitimate real estate investing strategy that experienced investors use successfully — and a strategy that has also produced financial distress for investors who underestimated the risks or over-relied on appreciation to make the numbers work.

The strategy’s success depends almost entirely on property selection, local market rent levels, and the discipline to include all costs — including HELOC interest — in the cash flow analysis. Investors who do that work rigorously can build genuine wealth through this approach. Investors who skip it typically discover the problem after they own the property.

Run the full cost stack. Stress-test the assumptions. Maintain adequate reserves. Consult a tax advisor before closing. And use our HELOC Payment Calculator to calculate the exact HELOC interest cost at your draw amount — that number belongs in every cash flow projection you build.