Can You Have Two HELOCs at the Same Time?

Yes, you can have two HELOCs at the same time — but the real question is not whether it is possible but whether it is practical for your situation, whether you can qualify for both, and whether it actually makes financial sense.

There are two distinct scenarios here. The first is having two HELOCs on two different properties — your primary home and a second home or investment property. The second is having two simultaneous HELOCs on the same property — which is technically possible but faces more lender restrictions. Both scenarios exist in the real world, both have legitimate use cases, and both come with specific challenges worth understanding before you pursue them.

Scenario 1: Two HELOCs on Two Different Properties

This is the more common and more straightforward scenario. You own two properties — a primary residence and a vacation home, rental property, or second home — and you want a HELOC on each.

This is entirely possible and not unusual for investors or homeowners with multiple properties. Each property has its own equity position, each HELOC is secured by the respective property, and each is a separate lending relationship with potentially different lenders.

How It Works

Each HELOC is evaluated independently based on the equity in the property securing it. The lender for the primary home HELOC looks at the primary home’s value and your primary mortgage balance. The lender for the second property HELOC looks at that property’s value and its mortgage balance.

The interaction between the two comes in your debt-to-income ratio — because both HELOC payments count as monthly debt obligations when either lender calculates your DTI. This is often where borrowers run into qualification challenges.

Example:

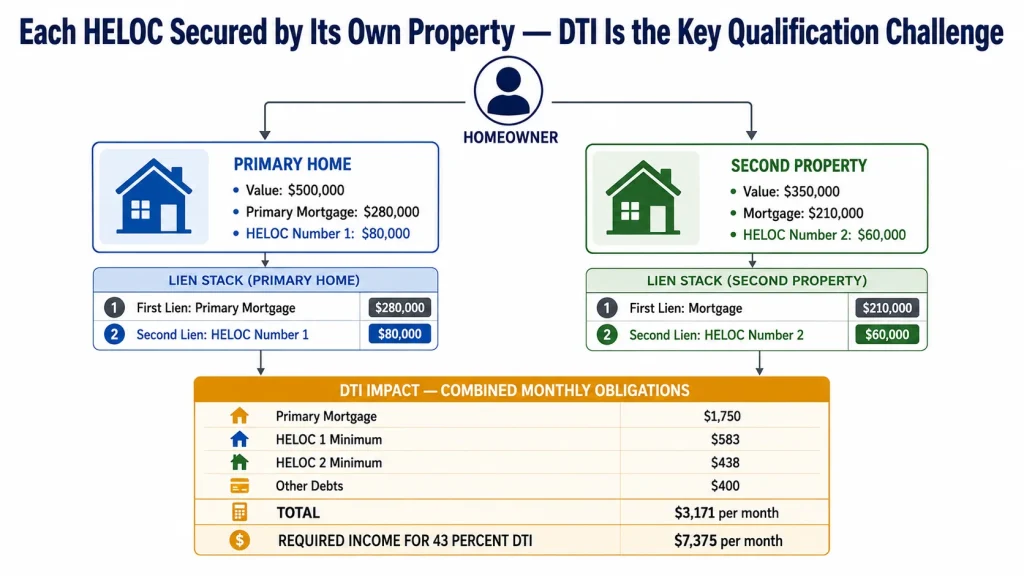

Primary home: worth $500,000, mortgage $280,000, HELOC #1 $80,000 approved Second property: worth $350,000, mortgage $210,000, seeking HELOC #2 $60,000

When you apply for HELOC #2, the lender sees:

- Primary mortgage payment: ~$1,750/month

- HELOC #1 interest-only minimum (on $80,000 at 8.75%): $583/month

- HELOC #2 interest-only minimum (on $60,000 at 8.75%): $438/month

- Other debts: say $400/month

Total monthly debt: $3,171 Required income for 43% DTI: $3,171 ÷ 0.43 = $7,375/month gross ($88,500/year)

For a household earning $100,000+ this is workable. For a household earning $75,000, the DTI may push outside the 43% limit and require renegotiating the amounts or waiting until other debts are reduced.

Qualification Differences for Second Property HELOCs

HELOCs on second homes and investment properties come with stricter terms than primary residence HELOCs:

Lower maximum CLTV: Most lenders cap CLTV at 70–80% for second homes versus 85% for primary residences. Investment property HELOCs are even more restrictive — many lenders cap at 65–75% CLTV and some do not offer them at all.

Higher interest rates: Second home and investment property HELOCs carry rate premiums of 0.25% to 1.00% above primary residence rates. On a large balance over a long draw period, this compounds meaningfully.

Stricter credit requirements: Many lenders require a credit score of 700+ for a second property HELOC versus 680 for a primary residence. Investment properties may require 720+.

No right of rescission on investment properties: The mandatory three-day cancellation window applies only to primary residences. Investment property HELOCs close and fund immediately.

Scenario 2: Two HELOCs on the Same Property

This is the less common scenario and the one that faces more lender restrictions — but it does happen, and there are legitimate reasons to pursue it.

The most typical situation: you have an existing HELOC from several years ago that you opened at a higher rate or with less favorable terms. You have paid it down substantially but you want more credit availability — perhaps your renovation needs grew, or you want a larger emergency reserve. Can you open a new HELOC while the old one still has a balance?

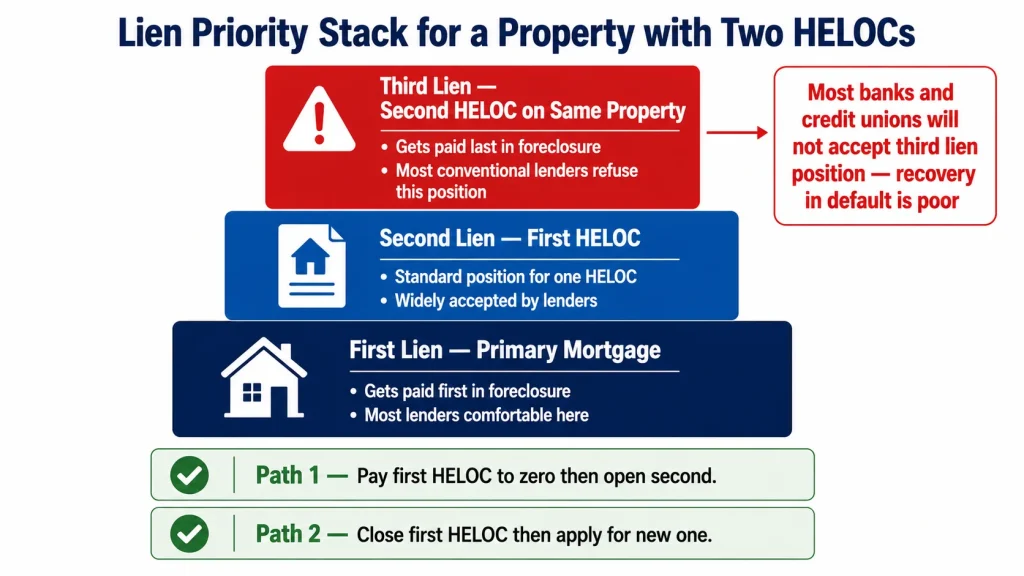

The Lien Position Problem

When a HELOC is placed on your property, the lender records a lien. The position of that lien in the priority order matters enormously for lenders.

Your primary mortgage holds the first lien position. The first HELOC typically holds second lien position. A second HELOC on the same property would need to be in third lien position — which means in a foreclosure, that lender gets paid last, after both the primary mortgage and the first HELOC are satisfied. Most lenders are extremely reluctant to accept third lien position because the recovery prospects in a default scenario are poor.

The result: Most conventional lenders will not open a new HELOC on a property that already has an existing HELOC with an outstanding balance. It is not a hard rule across all institutions but it is the practical reality at most banks and credit unions.

When It Is Possible

When the first HELOC is at zero balance: If you have an existing HELOC that has been paid down to zero — even if it is still open — many lenders will open a new HELOC on the same property. You now have two open HELOCs, but only one has credit available at any time depending on which you draw.

When you close the first HELOC first: The cleanest path to a second HELOC on the same property is to close the first one, then apply for the new one. This returns the property to having only one HELOC lien (second position, behind the first mortgage), which is standard and easy for lenders to work with.

Some lenders will refinance an existing HELOC into a new one: Rather than opening a true “second HELOC,” some lenders will refinance your existing HELOC — paying off the old one and replacing it with new terms, new rate, and potentially a larger credit limit. This appears on title as a single HELOC replacing the prior one, not as two simultaneous liens. This is often the most practical path when you want different terms or a larger credit line.

Specialty and portfolio lenders: A small segment of lenders who hold loans on their own books (rather than selling them to the secondary market) have more flexibility on lien position. Some private lenders and certain credit unions will accept a third lien position for borrowers with exceptional credit and equity. The terms are typically less favorable and rates are higher.

The DTI Challenge: The Real Barrier for Most Borrowers

Whether you are pursuing two HELOCs on different properties or trying to navigate two on the same property, the qualification challenge that trips up most borrowers is not the lien position or the credit score — it is the debt-to-income ratio.

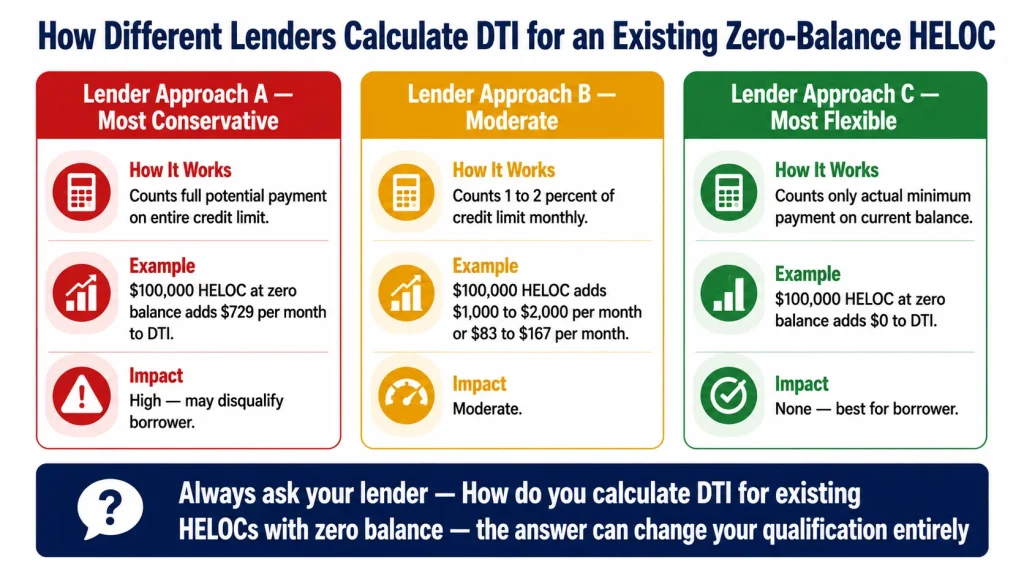

Every open HELOC — whether you have drawn from it or not — may count against your DTI. Different lenders handle unused credit lines differently:

Some lenders count the full potential payment: They calculate your DTI as if every open HELOC is fully drawn. On a $100,000 HELOC that you have not touched, some lenders add the interest-only payment on $100,000 to your monthly debt obligations.

Some lenders count the minimum payment on the actual balance: If your HELOC has a zero balance, they count $0. If it has a $30,000 balance, they count the minimum payment on $30,000.

Some use 1–2% of the credit limit: A rough payment estimate applied regardless of actual balance.

This inconsistency across lenders means it is worth asking specifically: “How do you calculate DTI for a borrower with an existing HELOC that has a low or zero balance?”

At a lender that counts the full potential payment, a $100,000 HELOC with a zero balance might add $729/month to your calculated DTI (interest-only on $100,000 at 8.75%). That could be the difference between qualifying and not qualifying for a second HELOC.

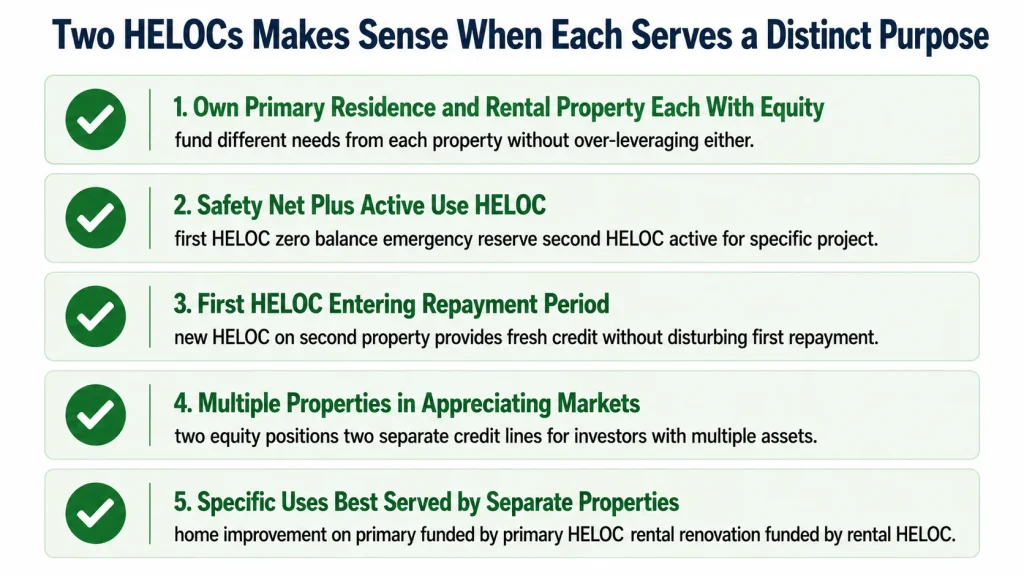

When Having Two HELOCs Makes Practical Sense

Most homeowners do not need two HELOCs. But there are specific situations where having two simultaneously makes genuine financial sense.

You own a primary residence and a rental property, each with significant equity. Using the equity in each property separately allows you to fund different projects or needs from the most appropriate collateral without over-leveraging either property.

You want to keep a safety net HELOC open while using a second HELOC actively. Some financially sophisticated homeowners keep a first HELOC open at zero balance as a pure emergency reserve while drawing from a second HELOC for a specific purpose — an investment, a renovation. The two serve entirely different functions.

Your existing HELOC has reached the end of its draw period. You are now in the repayment period on the first HELOC but you have identified a new funding need. A new HELOC on a second property — or a refinance of the existing HELOC — provides fresh access to equity without disturbing the repayment schedule of the first.

You have a property in an appreciating market and want to capture equity from multiple assets separately. Two properties, two equity positions, two credit lines. For investors with multiple properties, this is a standard part of capital management.

What Happens to Your Credit Score

Opening a second HELOC affects your credit in several ways worth understanding.

Hard inquiry: Each HELOC application generates a hard inquiry on your credit report — a small, temporary score reduction of 3 to 5 points per application. If you apply to multiple lenders for the second HELOC within a 14-to-45-day window, most scoring models treat it as a single inquiry.

New account and average account age: A new HELOC opens a new account, which reduces your average account age. This has a modest negative effect on your score that diminishes over time as the account ages.

Utilization on revolving accounts: HELOCs are revolving credit. Some scoring models factor HELOC utilization into your overall revolving utilization — which means a large drawn balance on a HELOC can affect your score similarly to a large credit card balance.

Payment history: If you manage both HELOCs responsibly — making every payment on time — they contribute positively to your payment history over time, potentially improving your score.

The net credit score impact of opening a second HELOC is typically modest in the short term (a few points lower from the inquiry and new account) and neutral to positive in the medium term if managed well.

Tax Implications of Multiple HELOCs

The tax deductibility rules for multiple HELOCs follow the same principles as for a single HELOC — but the aggregate limits apply across all home equity debt combined.

You can deduct interest on home equity debt up to $750,000 combined (for joint filers) across all qualifying debt — your primary mortgage, any home equity loan or HELOC on your primary residence, and any qualifying debt on a second home.

If you have a $650,000 primary mortgage and two qualifying HELOCs of $60,000 each ($120,000 combined), your total qualifying debt is $770,000 — $20,000 above the $750,000 cap. Your deductible interest is limited to the portion attributable to $750,000 of combined debt.

For homeowners with large primary mortgages in high-cost markets, this cap can limit the deductibility of HELOC interest even when the use of funds qualifies. Run the math with a tax advisor if you are in this position.

Interest on a HELOC secured by an investment property and used to improve or fund that investment property is handled under different rules — typically as a rental expense on Schedule E rather than mortgage interest on Schedule A.

Practical Steps If You Want Two HELOCs

If you have determined that having two HELOCs simultaneously is right for your situation, here is the practical path.

Step 1: Assess the equity position of both properties. Calculate your maximum HELOC on each property at 80% CLTV (use 70–75% for investment properties). This tells you the maximum credit you could access from each.

Step 2: Run your DTI with both HELOCs included. Add both HELOC minimum payments to your existing monthly debt obligations. Divide by gross monthly income. If the result is above 43%, you may need to reduce the credit line on one or both, or pay down other debt before applying.

Step 3: Determine the sequencing. If you are pursuing two HELOCs on different properties, apply for both simultaneously or in close sequence — before drawing on the first one, so neither lender sees active debt from the other. If you are pursuing a second HELOC on the same property, either close the first or pursue a refinance of the first into a new HELOC.

Step 4: Use the same lender for both if possible. Some lenders — particularly those with multiple property HELOC programs — are more willing to approve a borrower for two HELOCs if they hold both. It simplifies their risk management and can smooth the approval process.

Step 5: Model all payments in advance. Use our HELOC Payment Calculator to calculate the combined interest-only minimum payments on both HELOCs, the combined repayment period payments when both enter full amortization, and what the total monthly debt obligation looks like in the worst case — both at full balance in repayment simultaneously.

The Honest Assessment: Do You Actually Need Two?

Before pursuing two HELOCs, honestly ask whether the structure you need requires two separate credit lines.

In many cases, a single larger HELOC on the property with the most equity — or a HELOC plus a home equity loan combination — achieves the same financial goal without the qualification complexity, lien position challenges, and ongoing management of two separate credit lines.

The cases where two HELOCs is clearly the right structure: you own multiple properties, each with meaningful equity, and you want to fund needs from each property independently. The cases where it is probably unnecessary: you want more total credit and one larger HELOC on your primary residence would serve the same purpose.

The Bottom Line

Two HELOCs at the same time is possible and happens regularly — most cleanly when secured by two different properties, and with more complexity when both are on the same property.

The qualification gates are equity, DTI, and lender willingness to accept the lien structure. Of these, DTI is the most frequent practical barrier — both HELOC payments add to your monthly obligations, and the combined burden has to fit within standard lender limits.

If you have two properties with equity, stable high income, and a specific reason each property’s equity serves a different purpose — two HELOCs is a legitimate and manageable capital structure. If you are primarily looking for more total credit access, explore whether a single larger HELOC on your primary home achieves the same goal more simply.

Use our HELOC Payment Calculator to model the payment on each HELOC separately and combined — so you understand the full monthly commitment before you commit.