Interest-Only HELOC Payments: Pros, Cons & Examples

When you open a HELOC, your lender sets a minimum monthly payment during the draw period. For most HELOCs, that minimum is an interest-only payment — meaning you pay the cost of borrowing each month but none of the actual principal you owe.

For many homeowners, this is appealing. The payments are low. Cash flow is preserved. Flexibility feels high.

But interest-only payments are also one of the most misunderstood features of a HELOC. Used well, they are a legitimate financial tool. Used carelessly, they set you up for payment shock, a growing balance, and years of unnecessary interest costs.

This article covers everything you need to know about interest-only HELOC payments — how they work, how to calculate them, what they cost you over time, and when it actually makes sense to pay only the minimum.

What Are Interest-Only HELOC Payments?

During your HELOC draw period — typically the first 5 to 10 years — most lenders require only a minimum monthly payment equal to the interest accrued on your outstanding balance for that month. You are not required to pay down any of the principal.

This is different from a standard mortgage or personal loan, where every payment reduces your balance from day one. With an interest-only HELOC minimum, your balance at the end of month 12 can be identical to your balance at the end of month 1 — if you only ever paid the minimum.

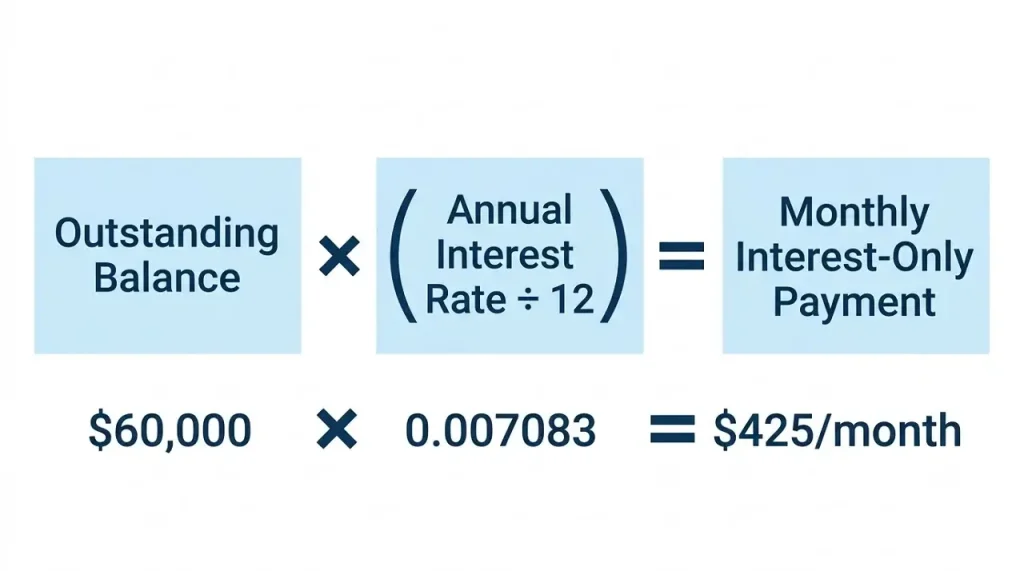

Here is the key formula behind every interest-only HELOC payment:

Monthly Interest Payment = Outstanding Balance × (Annual Interest Rate ÷ 12)

For example, if you have drawn $60,000 on your HELOC at an 8.5% annual interest rate:

$60,000 × (8.5% ÷ 12) = $60,000 × 0.007083 = $425.00/month

That $425 covers your interest obligation for the month. Your balance remains $60,000. Nothing has been paid down.

How Interest-Only Payments Are Calculated: Full Breakdown

Let’s walk through the calculation in detail so you understand exactly where your payment number comes from.

Step 1: Convert your annual rate to a monthly rate

Divide your annual interest rate by 12.

8.5% ÷ 12 = 0.7083% per month (or 0.007083 as a decimal)

Step 2: Multiply by your outstanding balance

This is the amount you have actually drawn, not your total credit limit.

$60,000 × 0.007083 = $425.00

Step 3: Understand that your balance drives your payment

Unlike a fixed mortgage payment, your HELOC interest-only payment changes as your balance changes. Draw more money and your payment goes up. Pay down some principal and your payment goes down.

This is both the flexibility and the trap of interest-only payments — there is always a temptation to draw more and worry about it later.

Interest-Only Payment Examples: $25,000 to $200,000

Here are real interest-only monthly payment calculations across common HELOC draw amounts. We have included three rate scenarios — a lower rate, a mid-range rate, and a higher rate — to show how rate changes affect your payment.

At 7.5% Interest Rate

| Balance Drawn | Monthly Interest-Only Payment | Annual Interest Cost |

|---|---|---|

| $25,000 | $156 | $1,875 |

| $50,000 | $313 | $3,750 |

| $75,000 | $469 | $5,625 |

| $100,000 | $625 | $7,500 |

| $150,000 | $938 | $11,250 |

| $200,000 | $1,250 | $15,000 |

At 8.75% Interest Rate

| Balance Drawn | Monthly Interest-Only Payment | Annual Interest Cost |

|---|---|---|

| $25,000 | $182 | $2,188 |

| $50,000 | $365 | $4,375 |

| $75,000 | $547 | $6,563 |

| $100,000 | $729 | $8,750 |

| $150,000 | $1,094 | $13,125 |

| $200,000 | $1,458 | $17,500 |

At 10% Interest Rate

| Balance Drawn | Monthly Interest-Only Payment | Annual Interest Cost |

|---|---|---|

| $25,000 | $208 | $2,500 |

| $50,000 | $417 | $5,000 |

| $75,000 | $625 | $7,500 |

| $100,000 | $833 | $10,000 |

| $150,000 | $1,250 | $15,000 |

| $200,000 | $1,667 | $20,000 |

Use our HELOC Payment Calculator to calculate your exact interest-only payment based on your specific balance and current rate.

The True Cost of Paying Interest Only for 10 Years

Here is a number that surprises most HELOC borrowers: if you draw $100,000 on your HELOC at 8.75% and pay interest only for the full 10-year draw period, you will have paid $87,500 in interest — and still owe the entire $100,000.

Let that sink in. Nearly $88,000 in payments and your balance has not moved a dollar.

This is the fundamental financial reality of interest-only payments. They are not free. They are a deferral of principal repayment — and that deferral has a compounding cost.

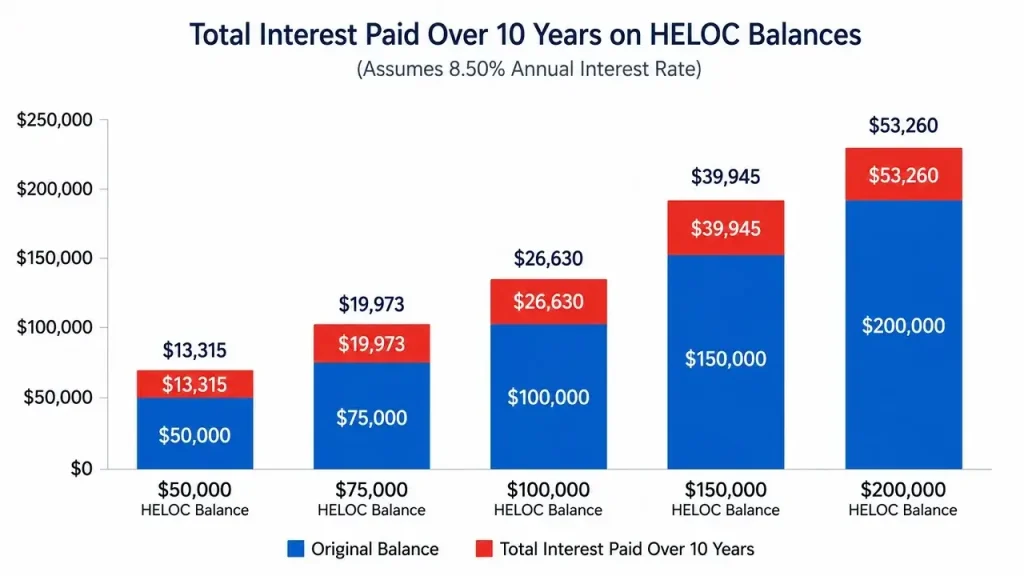

Here is that comparison across common balances over a full 10-year draw period at 8.75%:

| Balance | Total Interest Paid (10 yrs, interest-only) | Balance Remaining at Repayment |

|---|---|---|

| $50,000 | $43,750 | $50,000 |

| $75,000 | $65,625 | $75,000 |

| $100,000 | $87,500 | $100,000 |

| $150,000 | $131,250 | $150,000 |

| $200,000 | $175,000 | $200,000 |

A homeowner who borrowed $200,000 and paid interest-only for 10 years walks into the repayment period having already paid $175,000 — and still owing every cent of the original $200,000. Then the repayment clock starts.

This is why financial advisors consistently recommend paying more than the minimum during the draw period if your budget allows it.

Pros of Interest-Only HELOC Payments

Despite the long-term cost, interest-only payments offer real advantages in the right circumstances. Here is an honest look at the genuine benefits.

1. Maximum Cash Flow Flexibility

The most obvious benefit. When your minimum payment is $365/month instead of $994/month on a $50,000 balance, you have an extra $629 each month to deploy elsewhere — into an investment account, an emergency fund, or another financial priority.

For borrowers who are disciplined and have a deliberate plan for that extra cash flow, this flexibility has real value.

2. Ideal for Staged Projects

If you are using your HELOC for a home renovation that unfolds in phases — foundation in month 2, framing in month 4, kitchen in month 8 — interest-only payments keep your costs low during the months when your drawn balance is still building. You only pay interest on what you have actually used, not the full credit limit.

This is genuinely more efficient than taking out a lump-sum home equity loan upfront and paying interest on the full amount from day one.

3. Supports Short-Term Borrowing Strategies

Some borrowers use a HELOC strategically for short-term liquidity — bridging a gap between selling one home and buying another, for instance. In these cases, the plan is to repay the balance quickly from a specific event (a home sale, a business payout, a maturing investment). Interest-only payments keep costs low during the brief window the balance is outstanding.

4. Lower Payments During Tight Financial Periods

Life is unpredictable. A job change, a medical expense, or a family circumstance can temporarily reduce your available cash. During these periods, having only a minimum interest payment due on your HELOC — rather than a full principal-plus-interest payment — provides genuine breathing room.

Cons of Interest-Only HELOC Payments

The disadvantages are significant and should not be minimized.

1. Your Balance Never Shrinks

The most fundamental problem. Every dollar you borrow stays on the books until you actively pay it down. Ten years of minimum payments leaves you exactly where you started — with the same balance and now fewer years to repay it.

2. Payment Shock at Repayment

We covered this in detail in our article on HELOC Payment Shock, but it bears repeating here. The transition from interest-only to fully amortized payments is the biggest financial risk in a HELOC. Borrowers who coast on minimum payments for the full draw period face the steepest shock.

3. Variable Rate Risk Is Amplified

Because your balance never decreases during interest-only payments, the full original balance is exposed to rate increases for the entire draw period. A borrower who paid down $20,000 in principal has $20,000 less exposed to rising rates. A borrower who paid interest-only has the full balance at risk.

In a rising rate environment — which US borrowers experienced sharply from 2022 through 2024 — this difference is meaningful.

4. Total Interest Cost Is Maximized

As the tables above show clearly, paying interest-only for a full 10-year draw period maximizes the total interest you pay over the life of the HELOC. Every month you delay principal repayment is another month of full-balance interest accrual.

5. False Sense of Affordability

This is perhaps the most dangerous psychological effect. A $365/month payment on a $50,000 HELOC feels manageable — and it is, for now. But it can create a false sense that you have borrowed an affordable amount, when in reality you are sitting on a $50,000 debt that will soon require nearly $500/month to repay.

Borrowers who spend up to their full credit limit based on the comfort of interest-only payments are the most vulnerable to payment shock.

Interest-Only vs. Paying Extra Principal: Side-by-Side Comparison

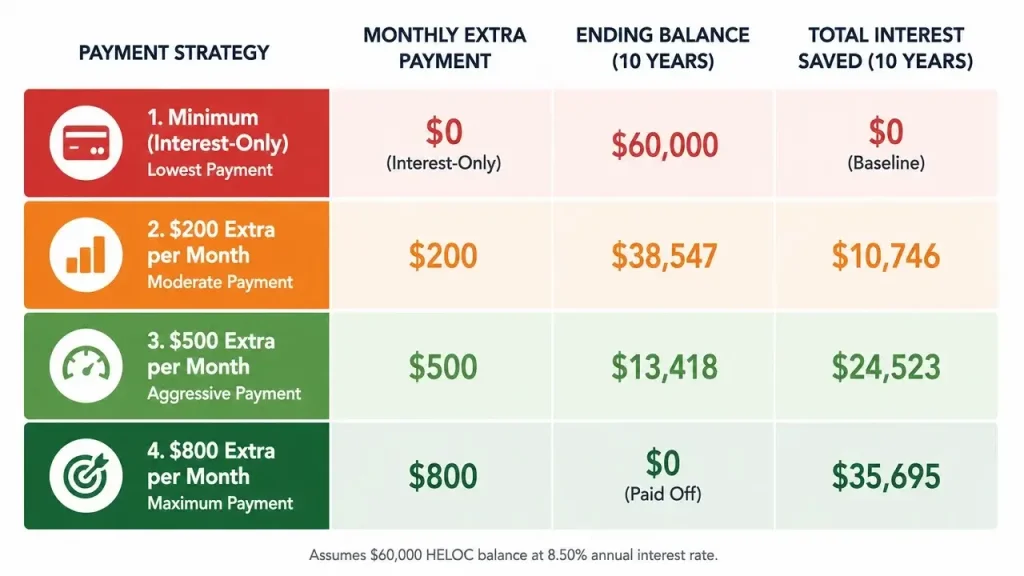

What happens if you pay more than the interest-only minimum? Here is a direct comparison on a $100,000 HELOC at 8.75% over a 10-year draw period, followed by a 15-year repayment period.

| Strategy | Extra Monthly Payment | Balance at End of Draw Period | Repayment Payment | Total Interest Paid |

|---|---|---|---|---|

| Interest-only minimum | $0 extra | $100,000 | $994/month | $179,200 |

| Pay $200 extra/month | $200 extra | $76,000 | $756/month | $152,300 |

| Pay $500 extra/month | $500 extra | $40,000 | $398/month | $112,600 |

| Pay $800 extra/month | $800 extra | $4,000 | $40/month | $85,900 |

The numbers tell a clear story. Adding just $200/month to your draw period payments reduces your total interest cost by over $26,000 and cuts your repayment payment by $238/month. Adding $500/month saves over $66,000 in total interest and slashes your repayment payment by nearly $600.

The cost of paying only the minimum is not just the interest you pay now — it is the compounding cost of carrying a large balance into a higher-payment repayment period.

When Does Paying Interest-Only Actually Make Sense?

Given all the downsides, is there ever a good reason to pay only the minimum? Yes — in specific, deliberate circumstances.

It makes sense when:

- You are using the HELOC for a staged project and your balance is still growing — paying principal on money you have not finished drawing is unnecessary

- You have a specific repayment event coming (a home sale, a maturing CD, a bonus) within 12–24 months and you are managing cash flow until that event

- Your alternative use for the extra cash generates a higher return than your HELOC rate — for example, if you are getting 10% returns investing and your HELOC rate is 8.75%, the math may favor investing over paying down the HELOC

- You are in a genuinely tight financial period and need the breathing room temporarily

It does not make sense when:

- You are paying interest-only simply because it is easy or because you have not thought about repayment

- Your draw period end date is less than 24 months away and you have a large balance

- You have been paying interest-only for years and your balance has not moved

- Your budget could comfortably absorb extra principal payments but you have not made them a priority

How to Make the Most of a HELOC Draw Period

If you currently have a HELOC in the draw period, here is a practical approach that balances the flexibility benefits of interest-only payments with smart long-term financial management:

Month 1–6: Pay interest-only while your project or purpose is active and your balance may still be changing.

Month 6 onward: Once your balance stabilizes, begin adding a fixed principal payment on top of the interest minimum. Even $150–$300/month changes your trajectory significantly over a multi-year draw period.

12 months before draw period ends: Aggressively increase principal payments or explore refinancing. This is your last opportunity to reduce the balance before full amortization kicks in.

Ongoing: Run your numbers in the HELOC Payment Calculator at least once a year. Update your rate if it has changed. See what your repayment payment will be with your current balance. That number should never be a surprise.

Frequently Asked Questions

Can I pay more than the interest-only minimum during the draw period? Yes, absolutely. There is no prepayment penalty on most HELOCs, and any amount above the minimum goes directly toward reducing your principal balance.

Does my interest-only payment change every month? It can, for two reasons. First, if your outstanding balance changes (you draw more or pay down principal), your payment adjusts accordingly. Second, if your variable interest rate changes, your payment changes even if your balance stays the same.

What happens if I only pay interest during the entire draw period? You enter the repayment period with your full original balance intact, face a significantly higher fully amortized payment, and will have paid years of interest with nothing to show in terms of debt reduction.

Is HELOC interest tax deductible? HELOC interest may be deductible if the funds are used to buy, build, or substantially improve the home securing the line of credit, per IRS guidelines. Interest on HELOC funds used for other purposes — debt consolidation, education, general spending — is generally not deductible. Always consult a tax professional for your specific situation.

Can I convert my interest-only HELOC to a fixed payment? Some lenders allow you to lock a portion of your HELOC balance into a fixed-rate sub-account with a set repayment schedule. Ask your lender specifically about this option — it is not universally offered but it is increasingly common among major banks.

The Bottom Line

Interest-only HELOC payments are a feature, not a flaw — but only if you use them intentionally. They offer genuine short-term cash flow benefits and make real sense for staged borrowing situations. Used as a long-term strategy for avoiding repayment, they maximize your interest costs and set you up for payment shock.

The smartest approach for most borrowers: pay interest-only when your balance is active and changing, then shift to principal-plus-interest payments as soon as your balance stabilizes. Treat the interest-only minimum as a floor, not a target.

Use our HELOC Payment Calculator to calculate your exact interest-only payment today, then model what happens when you add extra principal. The difference may surprise you.