HELOC vs. Personal Loan for Home Improvement

You have a home improvement project lined up — a kitchen remodel, a bathroom addition, a new roof, or a deck — and you need to borrow money to fund it. Two of the most commonly considered options are a HELOC and a personal loan.

On the surface they look similar. Both give you access to capital. Both require monthly payments. Both show up in your credit profile. But underneath, they are fundamentally different products with different rates, different risks, different qualification requirements, and different financial outcomes depending on how much you borrow and how quickly you repay.

This guide gives you the complete, honest comparison — with real numbers — so you can choose the right tool for your specific project and financial situation.

The Core Difference in Plain English

A HELOC is a secured loan. Your home is the collateral. Because the lender has a legal claim on your property if you default, the risk to them is lower — which is why HELOC interest rates are significantly lower than most unsecured borrowing options.

A personal loan is unsecured. No collateral. The lender has no claim on any asset if you stop paying — they can only pursue collection actions and damage your credit. That higher lender risk translates directly into higher interest rates for you.

This single difference — secured vs. unsecured — drives most of the practical differences between these two products.

Interest Rates: The Biggest Number in the Comparison

For most borrowers, the interest rate gap between a HELOC and a personal loan is the most important factor in the decision. It directly determines how much your project actually costs you beyond the contractor invoice.

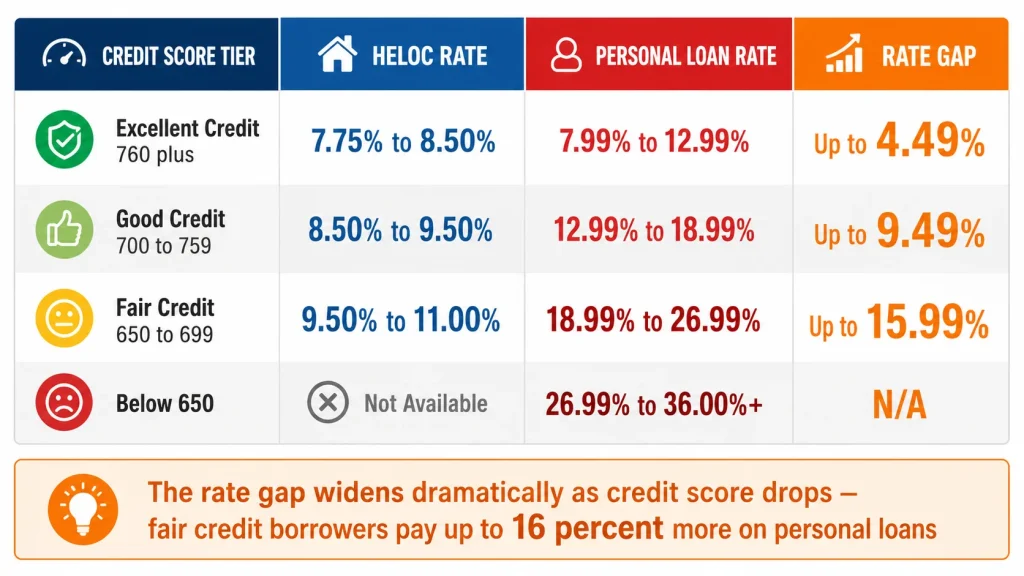

HELOC Rates in 2026

HELOCs carry variable interest rates tied to the Wall Street Journal Prime Rate. In 2026, most well-qualified borrowers can expect HELOC rates in the range of:

- Excellent credit (760+): 7.75% – 8.50%

- Good credit (700–759): 8.50% – 9.50%

- Fair credit (650–699): 9.50% – 11.00%

- Below 650: Most lenders will not approve a HELOC

Personal Loan Rates in 2026

Personal loan rates depend heavily on your credit score and income, but carry a significant premium over secured borrowing because of the unsecured nature. In 2026, typical personal loan rates are:

- Excellent credit (760+): 7.99% – 12.99%

- Good credit (700–759): 12.99% – 18.99%

- Fair credit (650–699): 18.99% – 26.99%

- Below 650: 26.99% – 36.00%+ (if approved at all)

The gap is substantial. A borrower with excellent credit might get a personal loan at 9.99% versus a HELOC at 8.25% — a 1.74% difference. A borrower with good credit might face a personal loan at 16.99% versus a HELOC at 9.00% — a 7.99% difference that compounds dramatically over time.

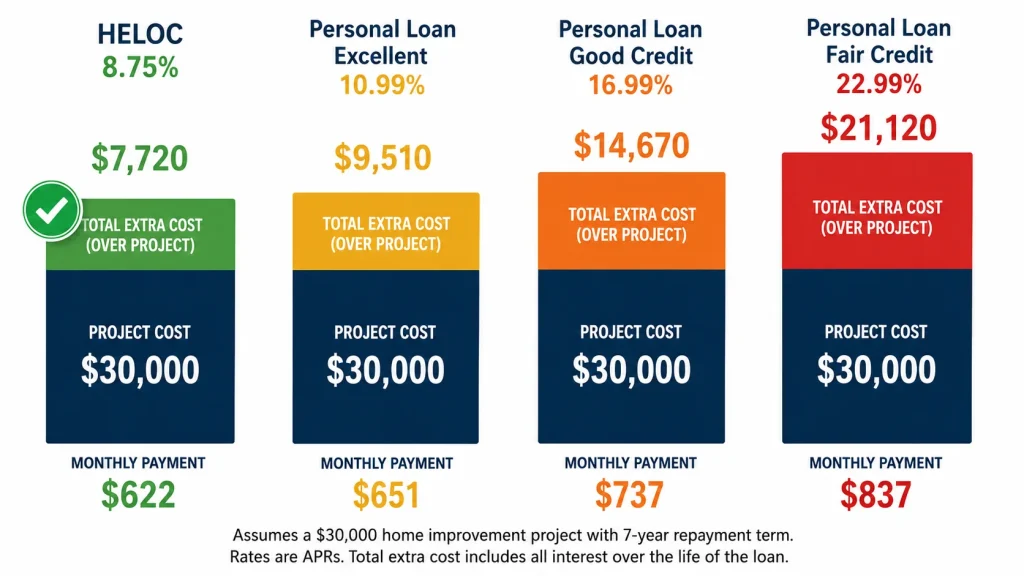

The Real Cost Difference: $30,000 Home Improvement Project

Let us make the rate difference concrete with a $30,000 kitchen renovation financed over 5 years under both products.

HELOC: $30,000 at 8.75%, 5-Year Repayment

| Amount | |

|---|---|

| Monthly payment | $622 |

| Total paid over 5 years | $37,320 |

| Total interest paid | $7,320 |

| Closing costs | $400 (estimated) |

| Total project cost above renovation | $7,720 |

Personal Loan: $30,000 at 12.99%, 5-Year Term (Good Credit)

| Amount | |

|---|---|

| Monthly payment | $681 |

| Total paid over 5 years | $40,860 |

| Total interest paid | $10,860 |

| Origination fee (1–5%) | $450 (estimated at 1.5%) |

| Total project cost above renovation | $11,310 |

Personal Loan: $30,000 at 18.99%, 5-Year Term (Fair Credit)

| Amount | |

|---|---|

| Monthly payment | $773 |

| Total paid over 5 years | $46,380 |

| Total interest paid | $16,380 |

| Origination fee (1–5%) | $900 (estimated at 3%) |

| Total project cost above renovation | $17,280 |

Summary for a $30,000 project:

| Product | Rate | Monthly Payment | Total Interest | Total Extra Cost |

|---|---|---|---|---|

| HELOC | 8.75% | $622 | $7,320 | $7,720 |

| Personal loan (excellent credit) | 10.99% | $651 | $9,060 | $9,510 |

| Personal loan (good credit) | 16.99% | $737 | $14,220 | $14,670 |

| Personal loan (fair credit) | 22.99% | $837 | $20,220 | $21,120 |

For a borrower with good credit, the personal loan costs $6,950 more in total financing cost than a HELOC on the same $30,000 renovation. For fair credit, the gap is $13,400.

Use our HELOC Payment Calculator to calculate your exact HELOC payment and total interest cost for your specific project amount.

Qualification Requirements: Who Can Actually Get Each Product

This is the critical factor that determines which option is even available to you — and it is where the two products diverge most sharply.

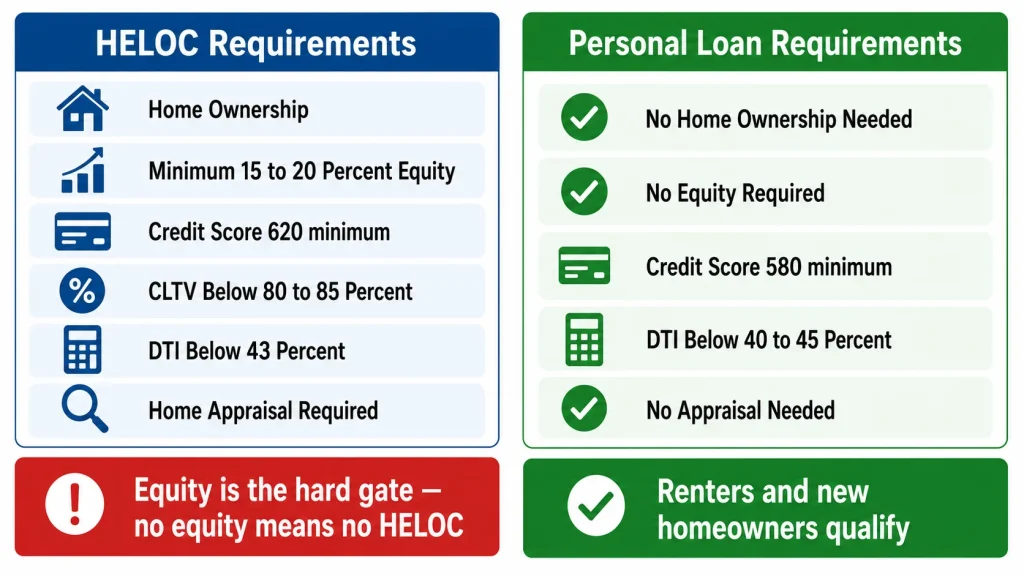

HELOC Qualification Requirements

To qualify for a HELOC, you need:

- Home ownership with sufficient equity: At least 15–20% equity in your property. No equity, no HELOC — full stop.

- Credit score: Minimum 620 at most lenders, though 680+ gets meaningfully better rates and 720+ gets the best available rates.

- Combined LTV ratio: Your mortgage plus the HELOC must stay at or below 80–85% of your home’s value.

- Debt-to-income ratio: Generally below 43%, including the projected HELOC payment.

- Stable documented income: Pay stubs, W-2s, or tax returns. Self-employed borrowers face additional documentation requirements.

- Home appraisal: Most lenders require a current valuation of your property.

The equity requirement is the hard gate. If you bought your home recently with a small down payment, or if your home’s value has not appreciated significantly, you may not have enough equity to qualify for a meaningful HELOC credit line.

Personal Loan Qualification Requirements

Personal loans have a completely different qualification profile:

- No home ownership required: Renters qualify. New homeowners with no equity qualify. Anyone with sufficient income and credit history qualifies.

- Credit score: Most lenders require 580–600 minimum, though rates below 670 are punishingly high.

- Income documentation: Pay stubs or bank statements typically sufficient. Self-employed borrowers generally have an easier time than with mortgage products.

- Debt-to-income ratio: Most lenders look for below 40–45%.

- No appraisal required: No collateral means no property valuation needed.

- No closing process: Many online lenders fund personal loans in 1–3 business days.

The key insight: personal loans are accessible to people who cannot qualify for a HELOC — renters, new homeowners, those with limited equity, or those with irregular income who struggle with mortgage-style documentation requirements.

Approval Speed and Funding Timeline

This practical factor matters more than many borrowers anticipate when a project has a start date.

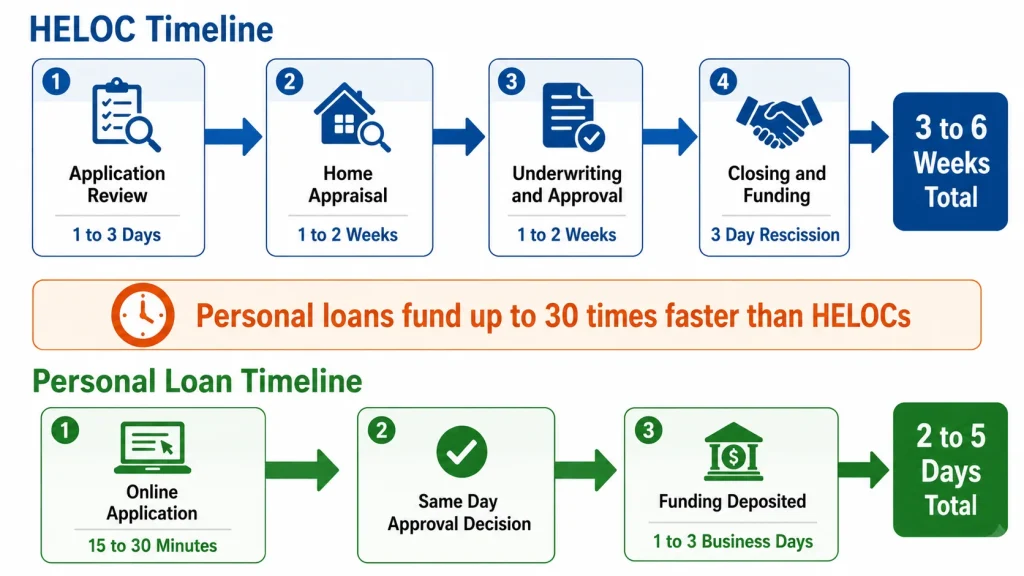

HELOC Timeline

Opening a HELOC is similar to getting a mortgage. The process typically involves:

- Application review: 1–3 days

- Home appraisal: 1–2 weeks to schedule and complete

- Underwriting and approval: 1–2 weeks

- Closing and funding: 3-day right of rescission required after closing

- Total typical timeline: 3 to 6 weeks

If your contractor needs a deposit next week, a HELOC may not be fast enough. If your project starts in two months, the timeline is perfectly workable.

Personal Loan Timeline

Personal loans — particularly from online lenders like SoFi, LightStream, Marcus by Goldman Sachs, and Discover — are dramatically faster:

- Application: 15–30 minutes online

- Approval decision: Same day in most cases

- Funding: 1–3 business days for most lenders

- Total typical timeline: 2–5 business days

For urgent projects, unexpected repairs, or situations where speed matters, personal loans have a decisive practical advantage.

Loan Amounts: What Each Product Can Deliver

The range of amounts available differs significantly between the two products.

HELOC Loan Amounts

Your HELOC credit limit is determined by your equity, not your income alone. Most lenders allow you to borrow up to 80–85% of your home’s value minus your existing mortgage balance.

For a home worth $350,000 with a $240,000 mortgage: $350,000 × 85% = $297,500 − $240,000 = $57,500 maximum HELOC

For a home worth $600,000 with a $300,000 mortgage: $600,000 × 85% = $510,000 − $300,000 = $210,000 maximum HELOC

HELOCs can deliver very large credit lines for homeowners with substantial equity. They are typically less useful for small projects under $10,000 — the closing costs and process overhead do not justify the effort for small amounts.

Personal Loan Amounts

Personal loans are available in amounts from $1,000 to $100,000 at most major lenders, with typical limits of $35,000–$50,000 for standard borrowers. Some lenders — including LightStream and SoFi — offer personal loans up to $100,000 for highly qualified borrowers.

Personal loans work well for small to mid-size projects. For very large renovations exceeding $75,000–$100,000, a HELOC or home equity loan typically delivers better rates and higher available amounts.

Risk Profile: What You Are Putting on the Line

This is the most psychologically significant difference between these two products — and one that deserves honest consideration.

HELOC: Your Home Is Collateral

When you sign for a HELOC, you are pledging your home as security for the debt. If you default — stop making payments — your lender has the legal right to foreclose on your property to recover what you owe.

This is not a theoretical risk to wave away. It is the fundamental nature of secured debt. In practice, foreclosure is a last resort that lenders pursue only after extended delinquency and failed workout attempts. But the risk is real and it belongs in your decision.

For a home improvement project, using your home as collateral to improve that same home is a logical, generally accepted use of secured debt. The project adds value to the collateral securing the loan. But using a HELOC to fund a project on a home you are not confident you can afford to keep, or during a period of financial instability, introduces risk that a personal loan does not.

Personal Loan: No Asset at Risk

If you default on a personal loan, the lender cannot seize your home, your car, or any other specific asset. They can damage your credit, pursue collection actions, and potentially sue you for the balance — but your home is not on the line.

For borrowers in volatile financial situations, those who are self-employed with variable income, or those who simply want to ring-fence their home from any borrowing risk, the unsecured nature of a personal loan is a genuine benefit that justifies paying a higher interest rate.

Tax Deductibility: HELOC Has a Potential Advantage

Under current IRS rules, HELOC interest may be tax deductible when funds are used to buy, build, or substantially improve the home securing the line of credit. A kitchen remodel, bathroom addition, or structural improvement funded by a HELOC may qualify.

Personal loan interest is never tax deductible, regardless of how the funds are used.

For a borrower in the 22% federal tax bracket with a $30,000 HELOC at 8.75%, the tax deductibility of interest reduces the effective rate:

8.75% × (1 − 0.22) = 6.83% effective after-tax rate

This after-tax rate further widens the cost advantage of the HELOC over a personal loan. Always consult a tax professional to confirm whether your specific project qualifies for the deduction.

The Flexibility Factor: Revolving vs. Installment

A HELOC is a revolving credit line. Once you repay drawn funds during the draw period, that credit becomes available again. For a multi-phase renovation — demo this spring, structural work in summer, finishes in fall — this revolving structure means you draw as costs arrive, repay what you can between phases, and re-draw for the next phase without opening a new loan.

A personal loan is a closed installment loan. You receive the full amount at closing, make fixed monthly payments, and when it is paid off it is done. There is no re-draw capability. If your renovation costs more than anticipated, you would need to apply for a second personal loan — a separate application, a separate hard credit inquiry, and potentially a higher rate if your debt load has increased.

For multi-phase or open-ended renovation projects, the HELOC’s revolving structure is a meaningful practical advantage.

When a Personal Loan Makes More Sense

Despite the higher rate, there are clear situations where a personal loan is the right choice for a home improvement project.

You are a renter or new homeowner with limited equity. No equity means no HELOC. A personal loan is your primary unsecured option for meaningful home improvement financing.

You need money fast. A contractor deposit due in 3 days, an urgent repair that cannot wait 4–6 weeks for a HELOC to close. Personal loans from online lenders fund in 1–3 business days.

Your project is small — under $15,000. The closing costs, appraisal, and process overhead of a HELOC are harder to justify for small amounts. A personal loan with no origination fee from a lender like LightStream or Marcus is simpler and comparably priced for small projects.

You do not want to put your home at risk. If your financial situation is uncertain or you strongly value keeping your home out of the collateral equation, the higher personal loan rate may be worth the peace of mind.

You have excellent credit. At 760+ credit scores, personal loan rates from the best lenders (LightStream offers rates as low as 6.99% for home improvement with autopay) can actually compete with HELOC rates — particularly when HELOC closing costs are factored in for small loan amounts.

Your renovation is on a rental property or a property you do not own. You cannot get a HELOC on a property you do not own. Landlords improving tenant-occupied rentals sometimes use personal loans for smaller projects.

When a HELOC Makes More Sense

Your project exceeds $20,000–$25,000. Above this threshold, the rate difference between a HELOC and a personal loan produces interest savings that far exceed HELOC closing costs. The larger the project, the more compelling the HELOC becomes.

You have substantial equity. If you have 30–40%+ equity in your home, you have a large, low-cost credit line available. Using it for home improvement — which typically adds value to the collateral — is a financially sound deployment of that equity.

Your renovation is multi-phase or cost-uncertain. Staged draws, re-draw capability, and interest paid only on what you use make the HELOC structurally superior for complex projects.

You have good to excellent credit. The rate gap between HELOC and personal loan widens significantly as credit quality drops. At 700+ credit scores, the HELOC rate advantage is compelling. At 750+, it is decisive for any meaningful loan amount.

You want the potential tax deduction. For projects that qualify under IRS rules, the after-tax cost of a HELOC can be 1–2 percentage points lower than the nominal rate suggests.

Your project timeline is not urgent. If you have 4–6 weeks before the project starts, the HELOC’s slower approval process is not a barrier.

Side-by-Side Comparison Summary

| Factor | HELOC | Personal Loan |

|---|---|---|

| Interest rate (good credit) | 8.50% – 9.50% | 12.99% – 18.99% |

| Secured or unsecured | Secured — home as collateral | Unsecured — no collateral |

| Home ownership required | Yes — and equity required | No |

| Approval timeline | 3–6 weeks | 2–5 business days |

| Closing costs | $200 – $2,000 | $0 – 5% origination |

| Loan amounts | Up to $100,000+ (equity-limited) | Up to $100,000 (credit-limited) |

| Fixed or variable rate | Variable | Fixed |

| Tax deductible interest | Potentially (home improvement use) | Never |

| Revolving credit | Yes — re-draw available | No — one-time disbursement |

| Home foreclosure risk | Yes | No |

| Best project size | $20,000+ | Under $20,000 |

| Best credit profile | 680+ | Any, but rate spikes below 700 |

A Quick Decision Rule

Run through these three questions to reach a fast, reliable answer:

Do you own your home and have at least 15–20% equity? No → Personal loan is your primary option. Yes → Continue.

Is your project over $20,000 and not urgently time-sensitive? No (under $20,000 or urgently needed) → Personal loan may be simpler and comparable in cost. Yes → Continue.

Is your credit score above 680? No → Personal loan rates may be very high; HELOC rates with fair credit are also elevated — compare both carefully. Yes → HELOC almost certainly delivers a lower total cost for a project over $20,000.

The Bottom Line

For most homeowners with solid equity and a renovation project above $20,000, a HELOC delivers meaningfully lower total financing costs than a personal loan — often saving $5,000 to $15,000 in interest on a mid-size renovation. The lower rate, potential tax deductibility, and revolving flexibility make it the superior tool when you qualify.

Personal loans earn their place for renters, new homeowners with limited equity, small projects, urgent timelines, and borrowers who want to keep their home entirely out of the collateral picture. At excellent credit scores, top-tier personal loan lenders also close the rate gap enough to compete for smaller amounts.

The decision is not about which product is better in the abstract — it is about which product fits your equity position, project size, timeline, and risk tolerance.

Use our HELOC Payment Calculator to model your exact HELOC cost for your project amount, then compare it to the best personal loan rate you can qualify for. The total interest difference over your repayment timeline will make the right answer clear.