HELOC Requirements: Credit Score, LTV & Income (2026)

Getting approved for a HELOC is not complicated — but it is more nuanced than most lender websites make it sound. Every bank has a checklist of requirements, and those requirements vary more than people expect. One lender’s minimum credit score is another’s hard cutoff. One lender’s maximum LTV is another’s starting point for negotiation.

This guide cuts through the vague marketing language and gives you the actual numbers lenders use in 2026 — what they look at, what they want to see, and where the real flexibility exists.

The Five Things Lenders Evaluate

When you apply for a HELOC, every lender is essentially asking the same five questions:

- Do you have enough equity in your home?

- Is your credit history reliable enough to trust?

- Can your income support the payments?

- Is your existing debt load manageable?

- Is the property itself acceptable collateral?

Everything on the application — your credit score, your pay stubs, your tax returns, the appraisal — feeds into one of these five questions. Understanding them as questions, not just numbers, helps you see why lenders weight them the way they do.

Requirement 1: Home Equity — The Hard Gate

Before anything else, you need equity. This is the one requirement that cannot be compensated for by a strong credit score or high income. No equity means no HELOC — full stop.

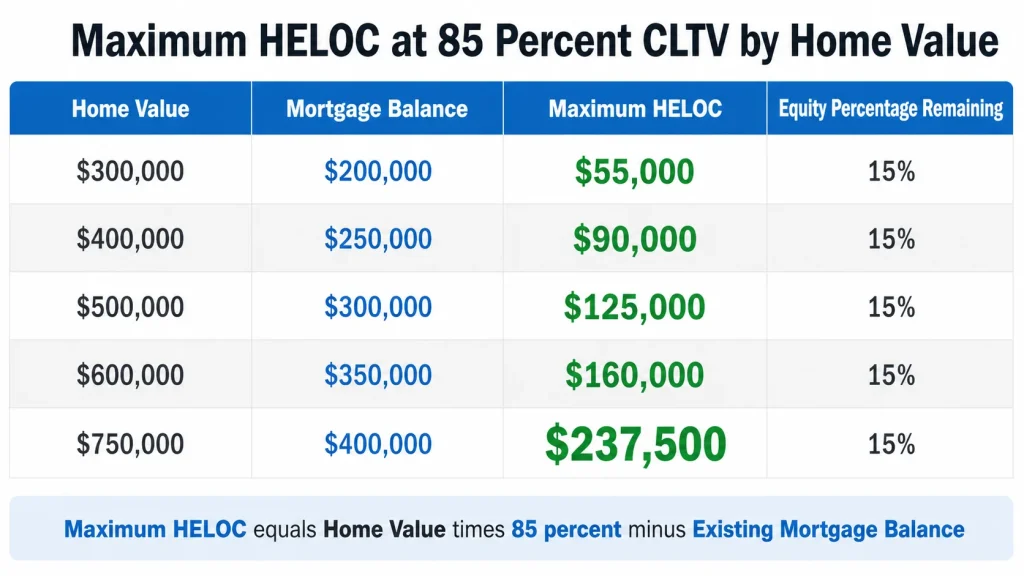

Most lenders set a maximum combined loan-to-value (CLTV) ratio of 80% to 85%. CLTV is the total of all debt secured by your home — your existing mortgage plus the requested HELOC — expressed as a percentage of the home’s appraised value.

How to calculate your maximum HELOC:

Maximum HELOC = (Home Value × Lender’s Max CLTV%) − Existing Mortgage Balance

Example at 85% CLTV:

| Home Value | Mortgage Balance | Max HELOC |

|---|---|---|

| $300,000 | $200,000 | $55,000 |

| $400,000 | $250,000 | $90,000 |

| $500,000 | $300,000 | $125,000 |

| $600,000 | $350,000 | $160,000 |

| $750,000 | $400,000 | $237,500 |

The equity requirement is not just a lender preference — it reflects genuine collateral value. A lender extending credit against a home needs confidence that if you default and they foreclose, the sale proceeds will cover both the first mortgage and the HELOC. At 85% CLTV, there is a 15% equity cushion absorbing any decline in property value before the lender’s position is threatened.

What If You Do Not Have Enough Equity?

Three realistic paths:

Wait for more appreciation. In markets with consistent price growth, a homeowner who is close to the 15–20% equity threshold may reach it within 12 to 24 months through natural appreciation.

Pay down your mortgage. Extra principal payments on your first mortgage directly increase your equity position. A $500/month extra principal payment on a $280,000 mortgage at 6.5% reduces the balance by about $6,000 in year one — pushing your CLTV ratio lower.

Improve the home’s appraised value. Cosmetic improvements before the appraisal — landscaping, fresh paint, minor repairs — can support a higher appraised value, improving your CLTV position. Do not over-invest here, but a home that photographs and presents well often appraises better than an identical neglected one.

Requirement 2: Credit Score — The Range That Actually Matters

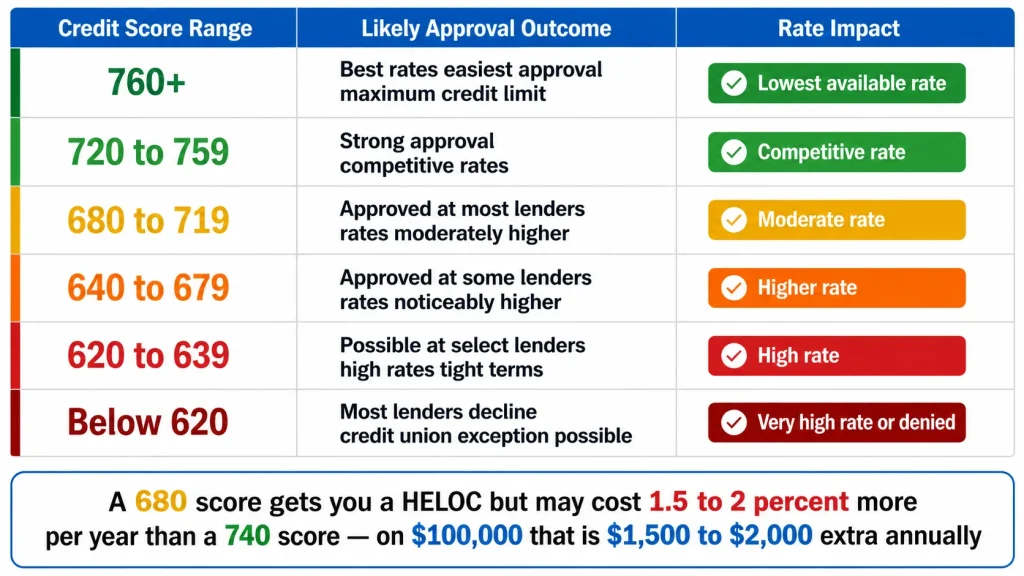

The most commonly cited HELOC credit score minimum is 620. That number is technically accurate for some lenders but misleading as a planning target. Here is the more useful breakdown:

| Credit Score | Likely Outcome |

|---|---|

| 760+ | Best available rates, easiest approval, maximum credit limit |

| 720–759 | Strong approval odds, competitive rates, minor exceptions possible |

| 680–719 | Approved at most lenders, rates moderately higher |

| 640–679 | Approved at some lenders, rates noticeably higher, lower credit limits |

| 620–639 | Possible approval at select lenders, high rates, tight terms |

| Below 620 | Most lenders decline; some credit unions make exceptions |

The practical implication: a 680 score gets you a HELOC at many institutions, but the rate you receive might be 1.5 to 2 percentage points higher than what a 740-score borrower pays from the same lender. On a $100,000 balance, that rate difference costs $1,500 to $2,000 per year in additional interest.

If your score is between 640 and 680, it is worth spending three to six months improving it before applying. The interest savings over the life of the HELOC will far exceed the cost of waiting.

What Lenders Actually Pull

Most HELOC lenders pull a tri-merge credit report — all three major bureaus (Equifax, Experian, TransUnion) — and use the middle of your three scores. If your scores are 698, 712, and 724, the lender uses 712.

Knowing this matters when you are close to a threshold. If your middle score is 679, improving it by a single point to 680 may unlock a meaningfully better rate at many lenders.

What Actually Moves Your Score

The two biggest factors in your FICO score are payment history (35%) and credit utilization (30%). If you are preparing to apply for a HELOC:

Pay every bill on time for at least six months. A single 30-day late payment can drop a good score by 60 to 100 points and stays on your report for seven years. There is no shortcut around this.

Pay down revolving balances. Getting your total credit card utilization below 30% of available limits has an immediate effect on your score. Getting it below 10% is even better. If you have a $10,000 credit card limit and owe $7,000, your utilization is 70% — a significant score drag. Paying it down to $2,500 before applying can add 20 to 50 points.

Do not open new credit accounts before applying. Each new application adds a hard inquiry and temporarily reduces your average account age — both negative factors. The three to six months before a HELOC application is not the time to open a new credit card or auto loan.

Requirement 3: Income — What Lenders Want to See and Why

Lenders need confidence that you can make monthly payments. Income documentation is how they verify that confidence.

Most HELOC lenders require:

W-2 employees: Two years of W-2s and the most recent 30 days of pay stubs. Straightforward and the path of least resistance.

Self-employed borrowers: Two years of personal tax returns (1040s) including all schedules, and two years of business tax returns if the business is structured as an S-corp, partnership, or LLC. Lenders typically average your net income over two years and use the lower of the two years if income has declined.

Retirees: Social Security award letters, pension statements, retirement account distribution statements, and investment account statements showing sustainable withdrawal capacity.

Rental income: Schedule E from your federal returns. Most lenders credit 75% of gross rental income toward qualifying income to account for vacancy and expenses.

Bonus and commission income: Averaged over two years if consistent. If your bonus was exceptional in one year and absent the next, lenders typically exclude it entirely or average it conservatively.

The most common income documentation problem is the self-employed borrower whose tax returns show low net income due to legitimate deductions — depreciation, home office, business expenses — but whose actual cash flow is healthy. This is a genuine challenge: lenders qualify you on reported income, not actual cash flow. If you are self-employed and planning to apply for a HELOC, talk to your accountant about whether your prior-year returns show enough net income to qualify before you apply.

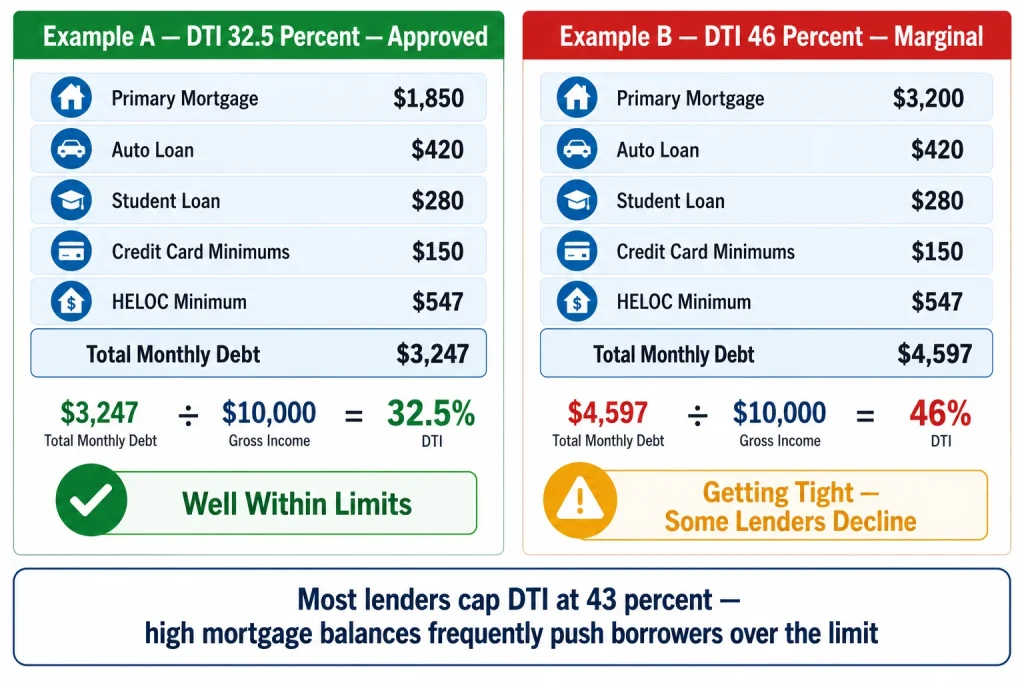

Requirement 4: Debt-to-Income Ratio — The Number That Often Surprises People

Your debt-to-income ratio (DTI) is total monthly debt payments divided by gross monthly income. Most HELOC lenders want this at or below 43%, though some allow up to 50% for well-qualified borrowers.

DTI = Total Monthly Debt Payments ÷ Gross Monthly Income

The “total monthly debt payments” number includes everything that shows up on your credit report — mortgage, car loans, student loans, credit card minimums, and the projected HELOC payment.

Example:

Gross monthly income: $10,000 Monthly obligations:

- Primary mortgage: $1,850

- Auto loan: $420

- Student loan: $280

- Credit card minimums: $150

- Proposed HELOC minimum (interest-only on $75,000 at 8.75%): $547

Total monthly debt: $3,247 DTI: $3,247 ÷ $10,000 = 32.5% — well within limits

Now the same profile with a higher mortgage:

Primary mortgage: $3,200 instead of $1,850 Total monthly debt: $4,597 DTI: $4,597 ÷ $10,000 = 46% — getting tight, marginal at many lenders

This is why homeowners with large primary mortgages in high-cost markets sometimes cannot qualify for meaningful HELOC credit lines even with strong income and good credit. The mortgage itself consumes most of the DTI capacity.

Front-End vs. Back-End DTI

Some lenders distinguish between front-end DTI (housing costs only) and back-end DTI (all debt). Most HELOC lenders focus primarily on back-end DTI. A few require front-end DTI to stay below 28%. If the lender you are working with asks about front-end DTI, it refers to your housing costs — mortgage principal, interest, taxes, and insurance — divided by gross monthly income.

How to Improve Your DTI Before Applying

Pay off or pay down installment loans and credit cards before applying. Eliminating a $420/month auto payment drops your DTI by 4.2 percentage points on a $10,000/month income. That swing can be the difference between approval and denial at a lender with a 43% cap.

Requirement 5: Property Type and Condition

Your home itself has to qualify — not just your financials.

Property types that typically qualify:

- Single-family homes (primary or secondary residence)

- Condominiums (FHA-approved condos qualify at most lenders; non-warrantable condos are more restrictive)

- Townhouses

- Two-to-four unit properties if you occupy one unit

- Some manufactured homes (lender-specific)

Property types that typically do not qualify:

- Investment properties or rentals you do not occupy (some lenders offer investment property HELOCs, but they are less common, carry higher rates, and have stricter LTV requirements)

- Raw land

- Commercial properties

- Cooperatives (co-ops) in most cases

Property condition matters too. A lender will not extend credit against a home with serious structural issues — foundation problems, significant water damage, roof in severe disrepair. The appraisal process will flag these issues and they can either delay or prevent approval until addressed.

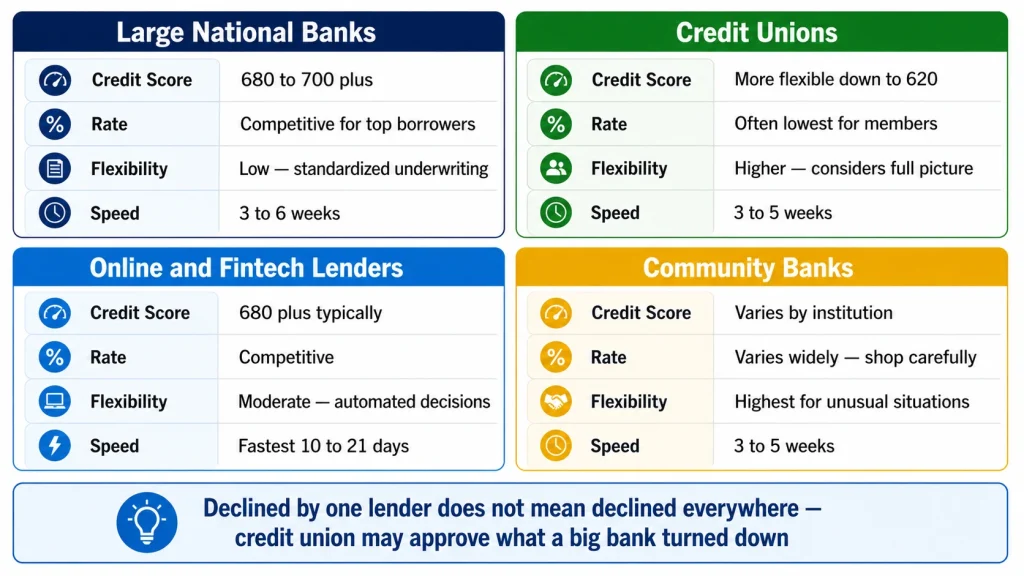

How Requirements Vary by Lender Type

One of the most practically useful things to know: HELOC requirements are not uniform across all lenders. The same borrower profile can produce dramatically different results at different institutions.

Large national banks (Wells Fargo, Bank of America, Chase, Citibank):

- Tend toward stricter credit score minimums (680–700+)

- Offer competitive rates for well-qualified borrowers

- Have standardized underwriting that is less flexible for edge cases

- Often have higher minimum draw amounts

Credit unions:

- Frequently more flexible on credit scores (down to 620 more willingly)

- Often have lower rates for members

- More willing to consider the full picture of a borderline application

- Membership requirement applies but is often easy to meet

Online and fintech lenders (Figure, Spring EQ, Aven):

- Fully digital application and closing process

- Often faster turnaround (some close in 5 to 10 days vs. 3 to 6 weeks at banks)

- Generally competitive rates for qualified borrowers

- Some use automated valuations instead of full appraisals, which speeds the process

Community banks and regional lenders:

- Often most flexible for unusual property types or borrower situations

- More human underwriting judgment in edge cases

- Rates and terms vary widely — shop carefully

The practical implication: if you are declined at one lender or offered unfavorable terms, apply elsewhere before accepting that result as final. A credit union may approve the same application a large bank turned down.

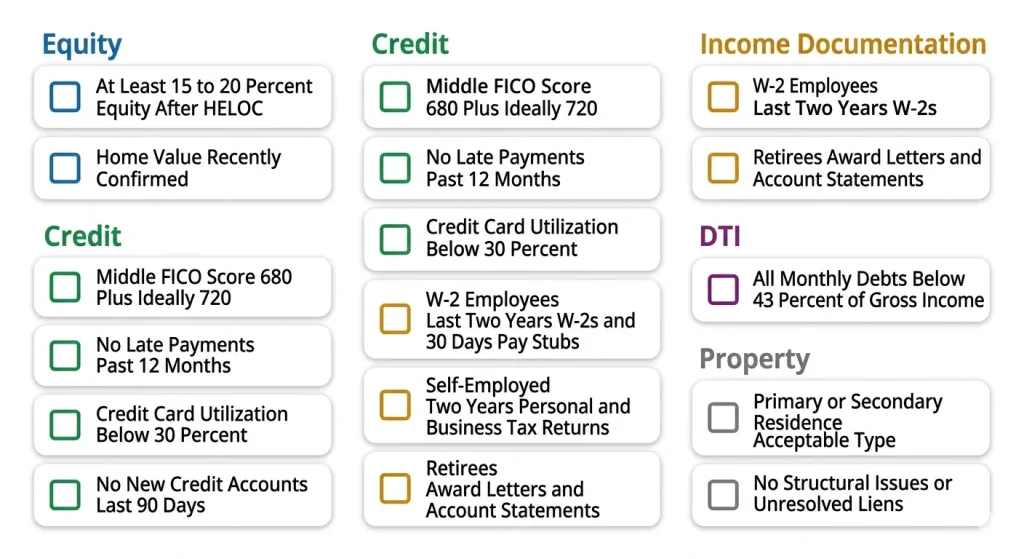

The Full Qualification Checklist

Here is a practical summary of what you need to have in order before applying:

Equity:

- At least 15–20% equity remaining after the HELOC (ideally 20%+)

- Home value confirmed by a recent comparable sale or automated estimate

Credit:

- Middle FICO score of at least 680 (720+ for competitive rates)

- No late payments in the past 12 months

- Credit card utilization below 30%

- No recent new credit accounts (last 90 days)

Income documentation:

- W-2 employees: last two years of W-2s plus 30 days of pay stubs

- Self-employed: last two years of personal and business tax returns

- Retirees: Social Security and pension award letters, account statements

DTI:

- All monthly debt payments below 43% of gross monthly income including projected HELOC payment

Property:

- Primary or secondary residence

- Acceptable property type and condition

- No unresolved liens or title issues

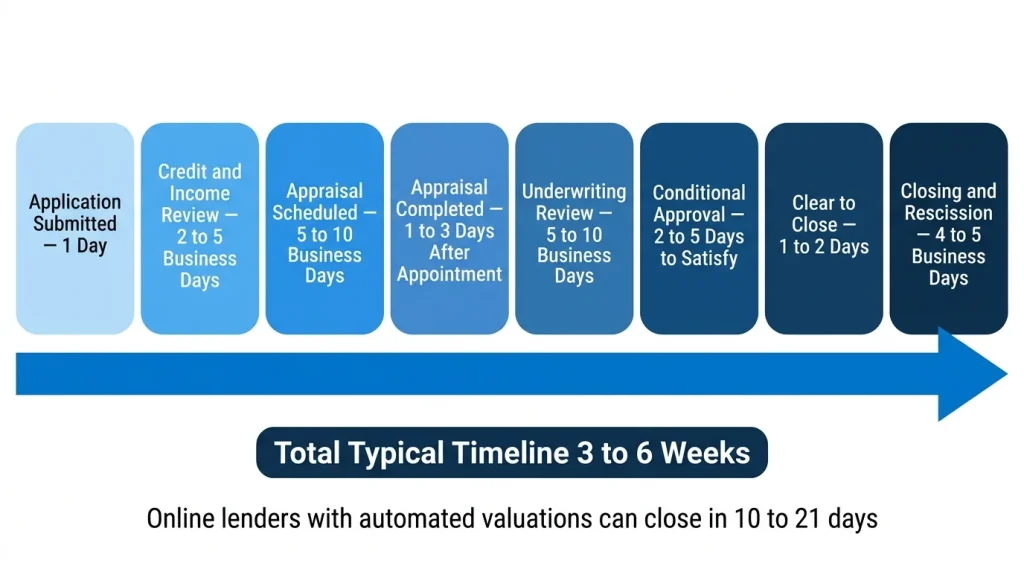

A Realistic Timeline From Application to Approval

Understanding the timeline helps you plan around the process rather than being surprised by it.

| Stage | Typical Duration |

|---|---|

| Application submission | 1 day |

| Initial credit and income review | 2–5 business days |

| Home appraisal scheduled | 5–10 business days |

| Appraisal completed | 1–3 business days after appointment |

| Underwriting review | 5–10 business days |

| Conditional approval (if applicable) | 2–5 days to satisfy conditions |

| Clear to close | 1–2 days |

| Closing and 3-day rescission period | 4–5 business days |

| Total typical timeline | 3 to 6 weeks |

Online lenders using automated valuations and digital closing can compress this to 10 to 21 days for qualifying applications. Traditional bank processes at the slower end run 5 to 7 weeks.

Plan your HELOC application 6 to 8 weeks before you need the funds. Waiting until the last minute and hoping for a fast close is a recipe for stress.

Common Reasons Applications Get Denied

Knowing why applications fail is as useful as knowing what lenders want.

Insufficient equity (CLTV too high): The most common reason. Your home has not appreciated enough, or you put down a small down payment and have not built meaningful equity yet.

Credit score below threshold: Usually correctable with time and focused effort on utilization and payment history.

DTI too high: Either income is lower than the monthly debt load supports, or existing debts are consuming too much of the DTI capacity.

Income documentation problems: Self-employed borrowers with aggressive deductions, borrowers whose income changed significantly between tax years, or borrowers with undocumented income sources.

Property issues: Appraisal comes in lower than expected, reducing available equity. Or the property has condition issues the appraisal flags.

Recent derogatory credit events: A bankruptcy within the last two years, a foreclosure within the last three to seven years (lender-dependent), or a recent collection account can result in denial regardless of current score.

The Bottom Line

Qualifying for a HELOC in 2026 comes down to five things: enough equity, a credit score above 680 ideally, income you can document, a DTI below 43%, and an acceptable property. Most homeowners who have been in their homes for three or more years and have kept up with mortgage payments will meet most of these requirements without significant preparation.

The borrowers who run into trouble are usually dealing with one specific issue — often DTI, sometimes credit score — that can be addressed with focused effort over three to six months before applying.

Shop multiple lenders. Requirements vary more than most people realize, and the difference between the right lender and the wrong one for your specific profile can mean the difference between approval and denial — or a rate difference worth thousands of dollars over the life of the HELOC.

Use our HELOC Payment Calculator to calculate your projected monthly payment and make sure the HELOC you are applying for fits comfortably within your budget — before the lender’s underwriter does the math for you.