How to Compare HELOC Lenders: What to Look For

Most homeowners apply to one or two HELOC lenders and take the best offer they get. That approach leaves real money on the table. The difference between a well-shopped HELOC and a hastily chosen one can be $10,000 to $20,000 in interest over the life of the loan — from the same borrower profile, often from lenders just a few miles apart.

The challenge is knowing what to compare. Rate is obvious, but it is not the only thing that matters — and sometimes it is not even the most important thing. A lender with a great rate but a $500 annual fee and a punitive early termination clause may cost more than a lender with a rate 0.25% higher and no ongoing fees.

This guide walks you through every meaningful comparison point — what to ask, what to watch for, and how to make a decision that reflects the full cost and quality of the relationship, not just the teaser rate.

Why Lender Comparison Matters More Than Most People Think

Before getting into the specifics, a quick illustration of what is at stake.

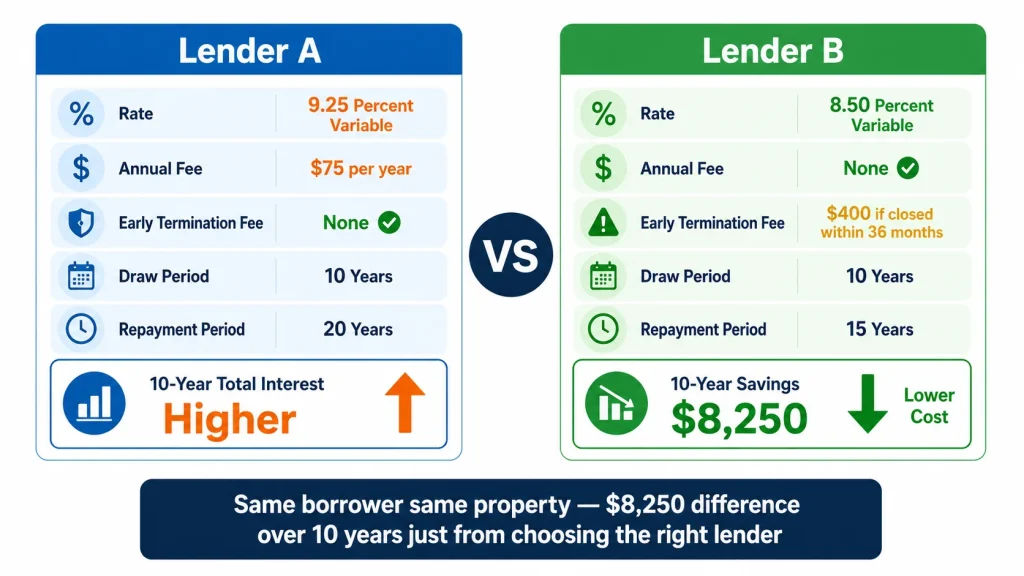

Two lenders, same $100,000 HELOC, same borrower:

Lender A: 9.25% variable rate, $75 annual fee, no early termination fee, 10-year draw / 20-year repayment

Lender B: 8.50% variable rate, no annual fee, $400 early termination fee if closed within 36 months, 10-year draw / 15-year repayment

Over a 10-year draw period at average balances and rates, the rate difference alone saves approximately $7,500 in interest with Lender B. Add the $75/year annual fee from Lender A and the gap grows to $8,250 over 10 years.

But if the borrower closes the HELOC after 18 months, Lender B’s $400 early termination fee reduces the advantage. Context matters.

This is exactly why you need to compare the full picture — not just the rate.

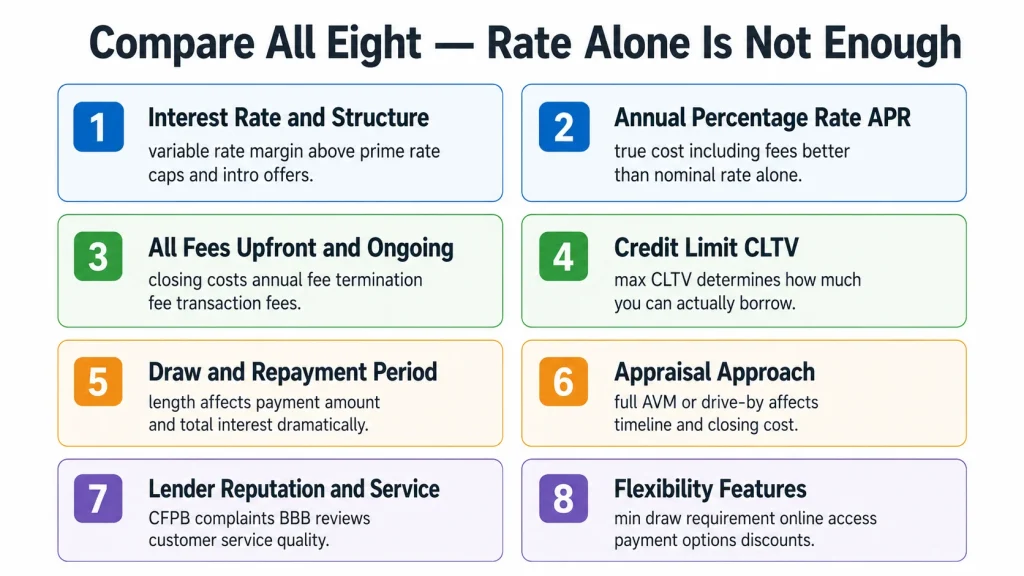

The Eight Things That Actually Matter When Comparing HELOC Lenders

1. Interest Rate and Rate Structure

The interest rate is the starting point of any comparison — but it comes with important nuances.

Variable rate tied to what index?

Most HELOC rates are tied to the Wall Street Journal Prime Rate. But confirm this with each lender. Some lenders tie to SOFR (Secured Overnight Financing Rate) or another index. The index itself matters less than whether you understand what moves your rate.

Margin (the spread above the index):

Your HELOC rate = Prime Rate + Lender Margin. If the prime rate is 7.50% and your lender’s margin is 1.25%, your rate is 8.75%. A lender with a 0.50% margin charges 8.00% — a 0.75 point difference that compounds significantly on a large balance.

Ask every lender: “What is your current margin above prime for my credit profile?” This lets you compare apples to apples even when the quoted rate temporarily reflects a promotional structure.

Rate caps:

Does the lender offer rate caps — a maximum the rate can rise per year or over the lifetime of the loan? Rate caps are not universal on HELOCs but some lenders offer them. On a large balance over a long draw period, a lifetime cap of prime + 6% (for example) can be genuinely valuable protection against extended rate-hiking environments.

Introductory rate offers:

Many lenders offer promotional rates — “prime minus 1% for the first 12 months” — to attract applicants. These are not necessarily bad, but understand exactly when the promotional rate ends and what the margin resets to. An attractive six-month teaser that resets to a 2.5% margin is often less favorable over the full draw period than a lender offering a consistent 1.0% margin from day one.

Fixed-rate conversion option:

Some lenders allow you to lock a portion of your outstanding HELOC balance into a fixed-rate sub-loan — effectively converting part of your variable-rate debt to a fixed installment. This feature has real value during periods of rising rates. Ask each lender whether this is available and what the conversion terms are.

2. Annual Percentage Rate (APR) vs. Nominal Rate

The APR accounts for fees rolled into the cost of the loan and gives a more complete comparison than the nominal rate alone. Request the APR from every lender — not just the rate — and use that for your primary comparison.

On a HELOC with no fees, the APR and rate are the same. On a HELOC with an origination fee or annual fee, the APR will be slightly higher than the nominal rate and reveals the true cost of borrowing more accurately.

3. All Fees — Upfront and Ongoing

This is where many borrowers do the comparison wrong. They compare rates and ignore fees — which can easily change which lender is actually cheaper over the relevant time horizon.

Fees to ask about at every lender:

Upfront closing costs:

- Application fee ($0–$500)

- Origination fee (0%–1% of credit limit)

- Appraisal fee ($0–$700)

- Title search and insurance ($100–$1,500)

- Recording fee ($25–$250)

- Attorney fee if required by state ($150–$500)

Ongoing fees:

- Annual fee ($0–$100/year) — over a 10-year draw period, a $75 annual fee adds $750 to your total cost

- Inactivity fee ($0–$50/year) — charged if you have no draws for 12+ months at some lenders

- Early termination fee ($0–$500) — triggered if you close the account within 2–3 years

Transaction fees:

- Wire transfer fee ($15–$30 per draw)

- Minimum draw requirement — some lenders require a minimum initial draw or minimum per draw (e.g., $10,000 minimum) that affects how you access the credit

Build a total cost model:

For each lender you are seriously considering, build a simple total cost estimate:

Total cost = Closing costs + (Annual fee × draw period years) + Estimated interest at quoted rate

This makes the comparison concrete rather than impression-based.

4. Credit Limit — How They Calculate It

You may qualify for different credit limits at different lenders for the same property — because lenders use different maximum CLTV ratios.

- Most lenders cap at 80–85% CLTV

- Some credit unions allow up to 90% CLTV for well-qualified members

- Some lenders apply stricter caps (75% CLTV) for certain property types or credit profiles

On a $500,000 home with a $300,000 mortgage:

- At 80% CLTV: max HELOC = $100,000

- At 85% CLTV: max HELOC = $125,000

- At 90% CLTV: max HELOC = $150,000

If you need $120,000 and one lender offers 80% CLTV while another offers 85%, the second lender is the only one that can actually serve your need — regardless of rate.

Ask each lender their maximum CLTV before spending time on the full application.

5. Draw Period and Repayment Period Length

Not all HELOCs have the same structure. The length of the draw period and repayment period affects both your payment and your total interest cost.

Draw period:

- 5-year draw period: Less time to access funds, faster transition to repayment

- 10-year draw period: Standard and most common

- Some lenders offer no formal draw period — essentially treating the HELOC like a revolving line

Repayment period:

- 10-year repayment: Higher monthly payment, less total interest

- 15-year repayment: Balanced — standard at most lenders

- 20-year repayment: Lower monthly payment, significantly more total interest

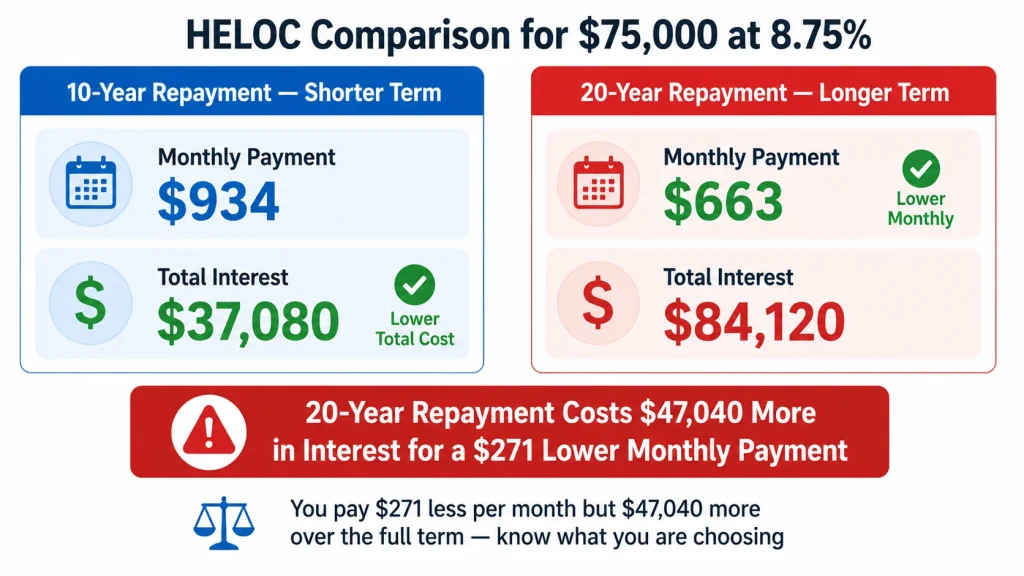

On a $75,000 balance at 8.75%, the difference between 10-year and 20-year repayment is:

- 10-year: $934/month, $37,080 total interest

- 20-year: $663/month, $84,120 total interest — $47,040 more in interest for a lower payment

Know what structure each lender offers and model the total cost in our HELOC Payment Calculator before deciding which term fits your situation.

6. Appraisal Approach — Full vs. AVM

As discussed in the timeline article, the appraisal approach affects both your timeline and your closing costs. Lenders who use automated valuations close faster and often waive the appraisal fee. Lenders requiring full interior appraisals add two to three weeks and $300–$700 in cost.

If your property is a standard single-family home in a market with clear comparable sales data, an AVM is likely accurate and the speed and cost savings are real advantages.

If your property is unusual — significant recent renovation, rural location, unique design, limited comparable sales — a full appraisal may actually serve you better because it can support a higher value that an AVM might underestimate.

Ask each lender upfront: “What type of appraisal do you use for my property type, and what is the cost?”

7. Lender Reputation and Service Quality

Rate and fees are quantifiable. Service quality is harder to measure but genuinely matters — particularly for a product that may involve multiple draws, rate change notifications, payment questions, and potentially a modification or workout conversation down the road.

Where to research:

Consumer Financial Protection Bureau (CFPB) complaint database: The CFPB maintains a public database of consumer complaints against financial institutions. Search your lender candidates. Look for patterns — many complaints about incorrect payment application, poor customer service during repayment period, or difficulty making draws are signals worth noting.

Better Business Bureau (BBB): Not perfect as a measure of quality but useful for spotting lenders with unresolved complaint patterns.

Google and Trustpilot reviews: Read the one-star and two-star reviews specifically. Positive reviews are often generic; negative reviews tend to contain specific, actionable information about where a lender falls short.

State banking regulator: Each state has a banking regulator (e.g., California Department of Financial Protection and Innovation, New York Department of Financial Services) that licenses and oversees lenders. You can check whether a lender is properly licensed and whether any regulatory actions have been taken.

Specific service questions to ask:

- How do I contact customer service if I have a question about my balance or rate?

- What is the process for requesting a draw? How quickly are funds available?

- If I want to make extra principal payments, is that applied immediately?

- Do you offer online account management with real-time balance and rate visibility?

- If I encounter financial difficulty during the repayment period, what modification or hardship programs do you offer?

A lender who struggles to answer these questions clearly during the sales process is telling you something about what the service relationship will look like after you close.

8. Flexibility Features

Beyond the core economics, several features differentiate lenders in ways that may matter for your specific situation.

Minimum draw requirements:

Some lenders require a minimum initial draw — often $10,000 or 25% of the credit line — at closing. Others have no minimum. If you want to open the HELOC now and draw only when needed, a minimum draw requirement forces you to start paying interest before you are ready.

Draw frequency limits:

A few lenders limit how often you can make draws — monthly or quarterly only. If you need flexible access for an ongoing renovation, a lender with daily draw capability is more practical.

Online draw access:

Can you initiate draws through an online portal or mobile app, or do you need to call or visit a branch? For most borrowers, online draw access is a basic expectation — but not all lenders, particularly smaller community banks, have fully built out digital HELOC management.

Payment methods accepted:

Can you make extra principal payments online? Are there any fees or restrictions on paying more than the minimum? A lender that makes extra payments difficult or charges fees for them is effectively penalizing the behavior that most benefits you.

Relationship discounts:

Many banks offer rate discounts (typically 0.25%–0.50%) if you have a checking or savings account with them and set up automatic payment from that account. If you already bank with an institution, this discount is essentially free rate reduction — factor it into your comparison.

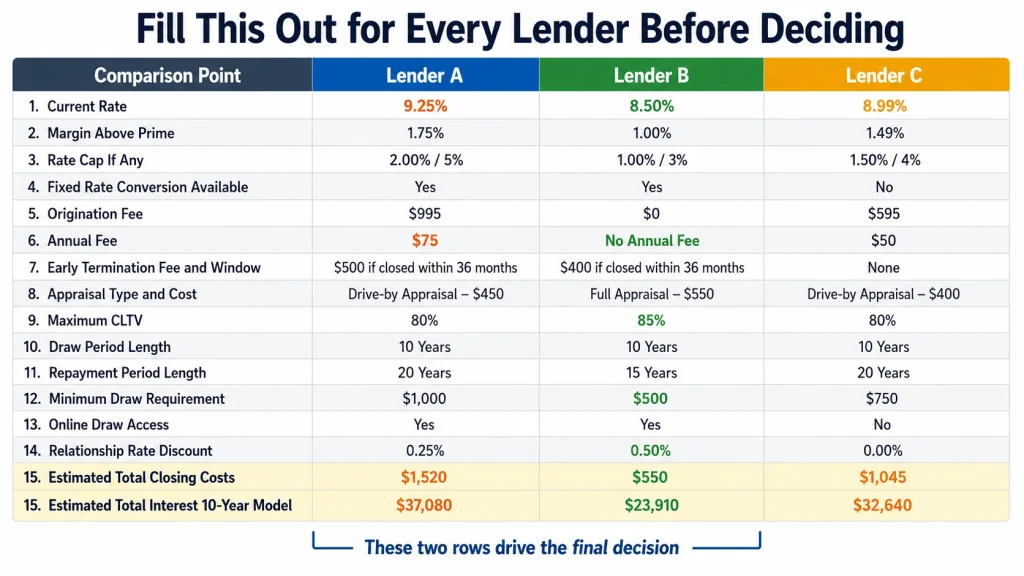

The Comparison Worksheet: How to Organize Your Research

When comparing multiple lenders, organize the information consistently so you are comparing equivalent data points. Here is a simple framework:

| Comparison Point | Lender A | Lender B | Lender C |

|---|---|---|---|

| Current rate | |||

| Margin above prime | |||

| Rate cap (if any) | |||

| Fixed rate conversion available? | |||

| Origination fee | |||

| Annual fee | |||

| Early termination fee / window | |||

| Appraisal type and cost | |||

| Maximum CLTV | |||

| Draw period length | |||

| Repayment period length | |||

| Minimum draw requirement | |||

| Online draw access? | |||

| Relationship rate discount available? | |||

| Estimated total closing costs | |||

| Estimated total interest (10-year model) |

Fill this out for every lender you are seriously considering. The bottom two rows — estimated total closing costs and estimated total interest — are the ones that should drive the final decision.

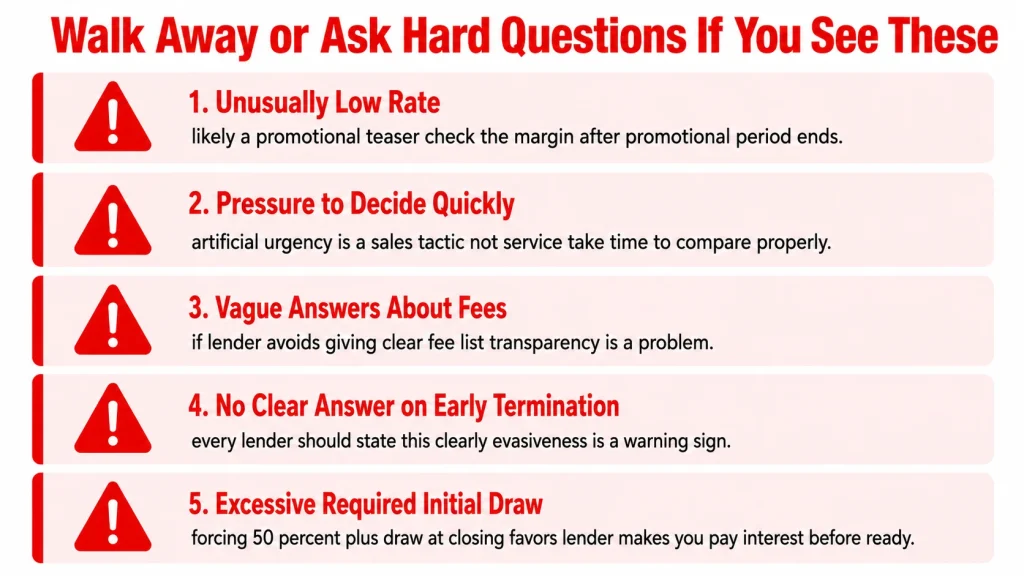

Red Flags to Watch For

As you shop, certain things should give you pause.

Rates that seem unusually low. If a lender is advertising a rate 1.5% below everyone else, read the fine print carefully. Often the advertised rate is a promotional teaser, requires a large initial draw, or requires automatic payment from an account at that institution. The margin after the promotional period may be significantly less attractive.

Pressure to decide quickly. A lender who creates artificial urgency — “this rate is only available through Friday” or “we are seeing a lot of applications this week” — is using sales tactics, not providing service. Take the time you need to compare properly.

Vague answers about fees. If a lender is reluctant to provide a clear written list of all fees before you submit an application, that is a signal about transparency more broadly. Good lenders are transparent about fees from the first conversation.

No clear answer on the early termination clause. Every lender should be able to tell you clearly whether an early termination fee applies and under what specific conditions. A vague or evasive answer here is worth noting.

Excessive required initial draw. A lender requiring you to draw 50% or more of the credit line at closing is essentially forcing you to start paying interest before you are ready. This favors the lender, not you.

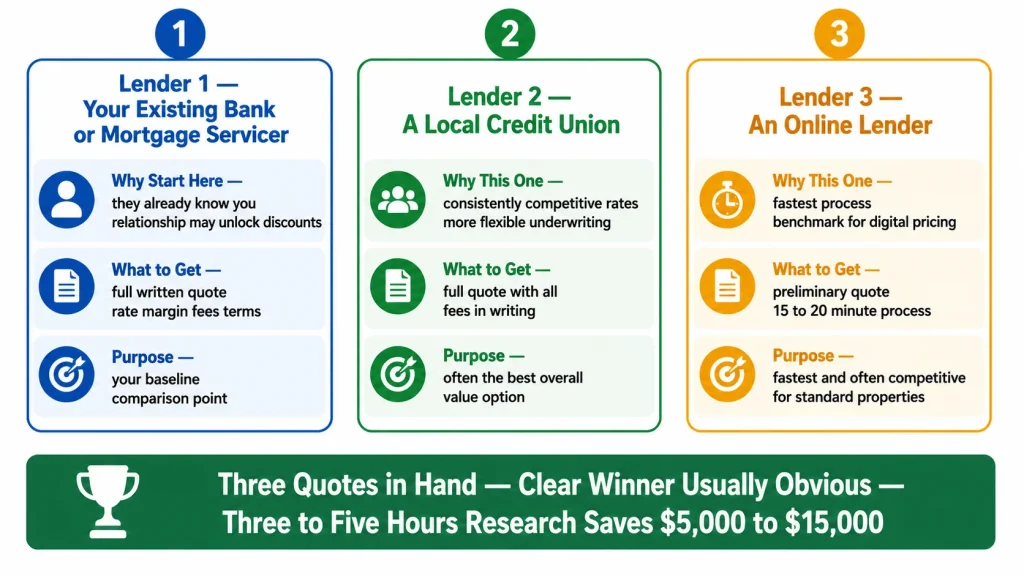

A Practical Three-Lender Approach

You do not need to contact ten lenders to get a well-shopped outcome. Three well-chosen lenders typically give you enough comparison data to make a confident decision.

Lender 1: Your existing bank or mortgage servicer. Start here because they already know you. Get their current offer — rate, margin, fees, and terms — in writing. This is your baseline.

Lender 2: A local credit union. Credit unions consistently offer competitive HELOC terms. If you are not already a member, check eligibility for credit unions serving your area, employer, or profession. Get a full quote with all fees in writing.

Lender 3: An online lender. Figure, Spring EQ, or a similar digital HELOC lender gives you a benchmark for the fastest and often most competitively priced option for standard property types. Their online quote process is fast — 15 to 20 minutes to get preliminary numbers.

With quotes from these three in hand, you have a genuine comparison. The best overall offer across rate, fees, terms, and service quality is usually clear.

The Bottom Line

Shopping HELOC lenders properly takes three to five hours of research and comparison. On a $100,000 HELOC over 10 years, that time is worth $5,000 to $15,000 in interest savings for many borrowers — one of the highest hourly returns available in personal finance.

The most common mistake is comparing only rates. The second most common is applying at only one lender and accepting whatever terms they offer. The fix for both is simple: gather complete information from at least three lenders, build a total cost comparison including fees, and make the decision based on the full 10-year picture rather than the headline number.

Use our HELOC Payment Calculator to model the total interest cost at each lender’s rate — so you can convert rate differences into actual dollar differences and make the comparison concrete.