How to Pay Off a HELOC Faster: Extra Principal Strategies

A HELOC gives you flexibility. But that flexibility comes with a cost that most borrowers underestimate — the longer you carry a balance, the more you pay in interest, and the harder the eventual repayment period hits.

The good news: you are not locked into the minimum payment schedule. Unlike some loan types, most HELOCs have no prepayment penalty. Every extra dollar you put toward principal reduces your balance, lowers your interest charges, and shortens the time until your HELOC is completely paid off.

This guide covers eight concrete strategies for paying off your HELOC faster, with real numbers showing exactly how much time and money each approach saves. Whether you are in the draw period or already in repayment, there is a strategy here that fits your situation.

Why Paying Off Your HELOC Faster Matters More Than You Think

Before diving into strategies, it helps to understand the full financial picture of carrying a HELOC balance long-term.

Most borrowers focus on the monthly payment. The more revealing number is the total interest cost over the life of the HELOC — and that number is often shocking when you see it laid out.

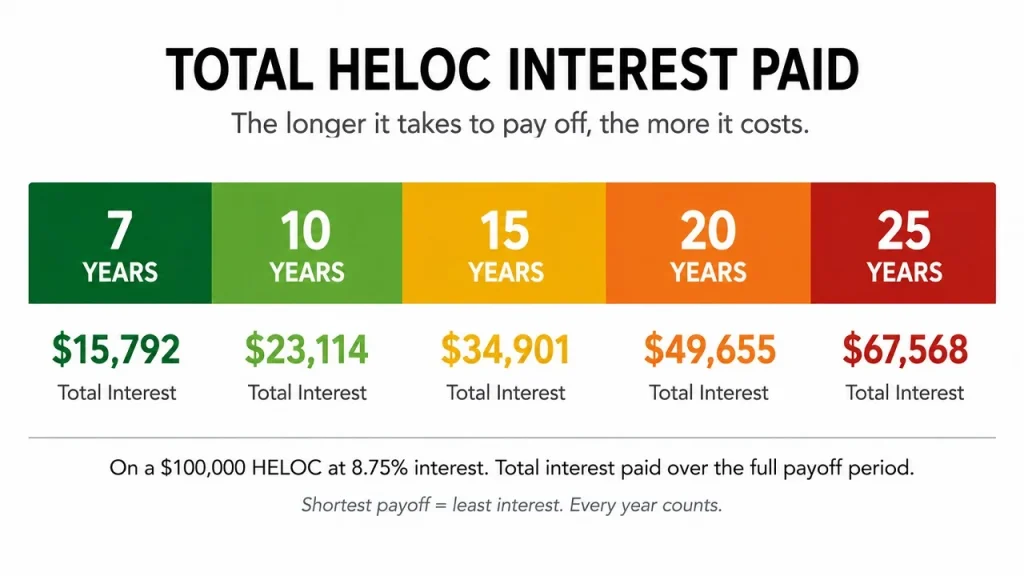

Here is what a $100,000 HELOC at 8.75% costs in total interest under different payoff timelines:

| Payoff Timeline | Monthly Payment (approx.) | Total Interest Paid | Interest Saved vs. Full Term |

|---|---|---|---|

| 25 years (full draw + repayment) | $729 interest-only → $994 amortized | $179,200 | — |

| 20 years total | $994/month from day one | $138,600 | $40,600 |

| 15 years total | $1,242/month | $123,600 | $55,600 |

| 10 years total | $1,244/month | $49,300 | $129,900 |

| 7 years total | $1,565/month | $31,460 | $147,740 |

Paying off a $100,000 HELOC in 10 years instead of 25 saves nearly $130,000 in interest. That is not a rounding error — that is a car, a college education, or a significant retirement contribution.

The monthly payment difference between a 25-year and 10-year payoff is roughly $515/month. The interest savings are $129,900. For every extra dollar you put toward your HELOC principal, you get a guaranteed, risk-free return equal to your interest rate.

In 2026, with most HELOCs carrying variable rates between 7.5% and 10%, that is a hard return to beat elsewhere.

First: Check for Prepayment Penalties

Before executing any early payoff strategy, read your HELOC agreement or call your lender to confirm there is no prepayment penalty.

Most modern HELOCs — particularly those issued by major banks and credit unions — have no prepayment penalty. However, many lenders include an early termination fee if you close the HELOC entirely within the first 2–3 years of opening it. This fee is typically $200–$500 and is triggered only if you close the account, not if you simply pay down or pay off the balance while keeping the line open.

Paying off your balance and leaving the HELOC open (with a zero balance) avoids early termination fees while still eliminating your interest costs. This is usually the smartest approach if you are within the early termination window.

Strategy 1: Fixed Extra Monthly Principal Payment

The simplest and most sustainable strategy. Pick a fixed dollar amount above your minimum payment and pay it every single month without exception. Treat it like a bill — non-negotiable, automatic, done.

The consistency matters more than the amount. A smaller extra payment made reliably every month beats a larger irregular payment every time, because consistent principal reduction compounds across the full life of the loan.

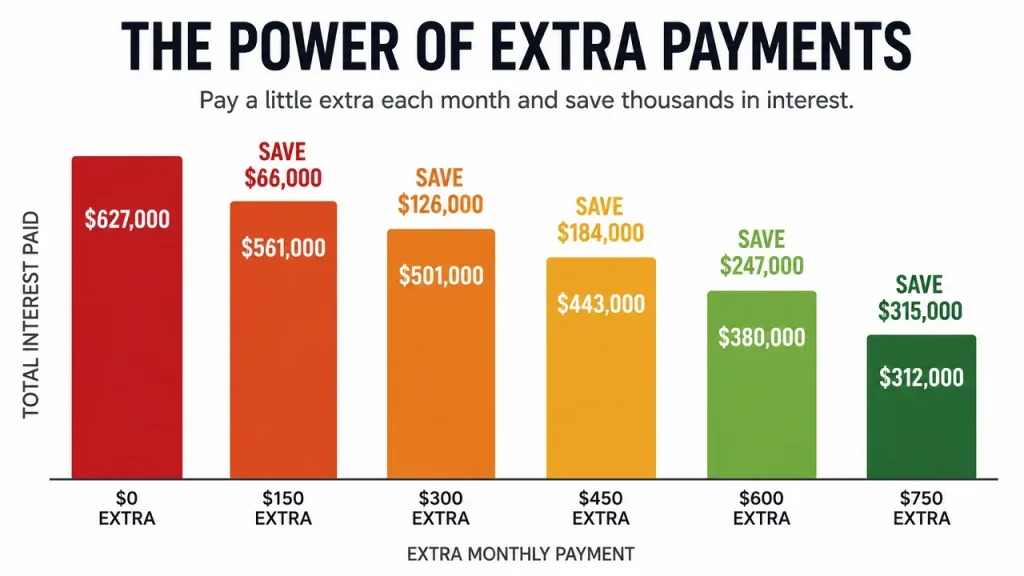

Here is what different fixed extra monthly payments do to a $100,000 HELOC at 8.75% with a 15-year repayment period:

| Extra Monthly Payment | New Monthly Total | Payoff Time | Total Interest | Interest Saved |

|---|---|---|---|---|

| $0 (minimum only) | $994 | 15 years | $79,000 | — |

| $100 extra | $1,094 | 12 yrs 8 mos | $64,800 | $14,200 |

| $200 extra | $1,194 | 11 yrs 1 mo | $56,800 | $22,200 |

| $300 extra | $1,294 | 9 yrs 11 mos | $51,200 | $27,800 |

| $500 extra | $1,494 | 8 yrs 4 mos | $42,600 | $36,400 |

| $750 extra | $1,744 | 6 yrs 10 mos | $35,700 | $43,300 |

Adding just $200/month saves over $22,000 in interest and cuts 3 years and 11 months off your repayment timeline. Adding $500/month saves $36,400 and cuts the timeline nearly in half.

Use our HELOC Payment Calculator to model your own balance, rate, and extra payment amount to see your specific payoff date and interest savings.

How to implement: Set up an automatic extra payment through your bank’s bill pay system on the same day your regular payment posts. Automating removes the temptation to skip it in tight months.

Strategy 2: Make Biweekly Payments Instead of Monthly

Instead of making one monthly payment, split your payment in half and pay every two weeks. Because there are 52 weeks in a year, biweekly payments result in 26 half-payments — equivalent to 13 full monthly payments instead of 12.

That one extra monthly payment per year goes entirely toward principal, quietly accelerating your payoff without requiring a significant budget change.

On a $100,000 HELOC at 8.75% with a 15-year repayment:

- Monthly payments: 15 years, $79,000 total interest

- Biweekly payments: 13 years 4 months, $68,400 total interest

- Savings: $10,600 and 1 year 8 months

This strategy works best during the repayment period when you have a fixed amortizing payment. During the draw period, biweekly payments still reduce your balance faster but the mechanics are slightly different since your payment is interest-only and variable.

How to implement: Contact your lender to confirm they accept biweekly payments and apply them immediately rather than holding the first half-payment until the due date. Some lenders hold partial payments until the full amount is received, which defeats the purpose. If your lender does not accommodate true biweekly application, simply make 13 full payments per year instead — one extra payment in a month of your choosing.

Strategy 3: Apply Lump Sum Payments When Available

Any time you receive a financial windfall — a tax refund, work bonus, inheritance, commission, freelance income, or proceeds from selling an asset — applying all or a substantial portion directly to your HELOC principal delivers an outsized impact.

Lump sum payments are powerful because they reduce the principal balance immediately and permanently. Every subsequent month’s interest calculation is based on the lower balance, so the savings compound forward through the entire remaining loan term.

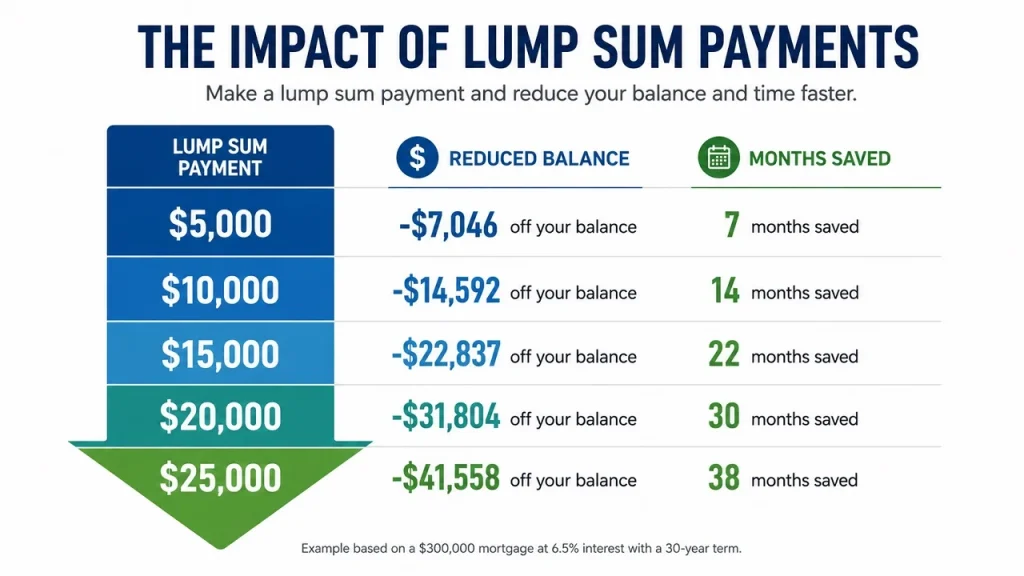

Here is the impact of a single lump sum payment on a $100,000 HELOC at 8.75% with 15 years remaining:

| Lump Sum Payment | New Balance | New Monthly Payment | Interest Saved | Time Saved |

|---|---|---|---|---|

| $5,000 | $95,000 | $944 | $4,750 | 7 months |

| $10,000 | $90,000 | $895 | $9,500 | 14 months |

| $15,000 | $85,000 | $845 | $14,250 | 22 months |

| $20,000 | $80,000 | $795 | $19,000 | 30 months |

| $25,000 | $75,000 | $745 | $23,750 | 38 months |

A single $10,000 lump sum payment saves $9,500 in interest and cuts 14 months off your payoff timeline. That is a nearly 1-to-1 return on the payment in interest savings alone — before accounting for the time savings and reduced stress.

How to implement: When a lump sum arrives, transfer it to your HELOC account immediately — before it sits in a checking account long enough to be spent on something else. Contact your lender or log into your online account to confirm the payment was applied to principal and not held as a future scheduled payment.

Strategy 4: Use the Debt Avalanche During the Draw Period

If you have multiple debts — credit cards, auto loans, student loans, a mortgage, and a HELOC — the debt avalanche method directs extra payments to the highest-interest debt first while maintaining minimums on everything else.

In most households, credit card debt carries rates of 20–28% APR — significantly higher than a HELOC at 8.75%. Under a true debt avalanche, you would eliminate the credit card debt first, then redirect those freed-up payments to your HELOC.

However, if your HELOC is your highest-rate debt, or if your other debts are at similar rates, the avalanche points directly at the HELOC.

Example: A homeowner has:

- HELOC: $80,000 at 8.75%

- Auto loan: $18,000 at 6.9%

- Credit card: $4,500 at 24.99%

Debt avalanche order: Credit card first ($4,500 at 24.99%), then HELOC ($80,000 at 8.75%), then auto loan ($18,000 at 6.9%).

Once the credit card is paid off, the $150/month minimum credit card payment gets redirected to the HELOC as an extra principal payment — no new money required from the budget.

This strategy does not require finding new money. It systematically redirects existing payments as each debt is eliminated.

Strategy 5: Round Up Your Payment Every Month

A simple, low-friction strategy that adds up over time. Every month, round your payment up to the nearest $50 or $100.

If your minimum payment is $729, pay $750 or $800. If it is $994, pay $1,000 or $1,050.

On a $100,000 HELOC at 8.75% with a 15-year repayment, rounding up by $50/month:

- Saves approximately $8,200 in interest

- Cuts approximately 10 months off the repayment timeline

It is not a dramatic strategy, but it is one that almost any borrower can implement immediately without straining their budget. And it requires zero discipline after the first setup — just pay the rounded number every month.

Strategy 6: Apply Rental or Side Income Directly to the HELOC

If you have a rental property, a side business, freelance income, or any irregular income stream, create a rule that a fixed percentage — say 50% or 100% — of that income goes directly to your HELOC principal every time it arrives.

This works particularly well because side and rental income often feels like “extra” money that tends to get absorbed into general spending without a deliberate plan. Routing it automatically to your HELOC gives it a purpose before it can disappear.

A homeowner who earns $800/month in rental income and routes half to their HELOC is effectively making a $400/month extra principal payment — equivalent to the $500 extra scenario in Strategy 1, which saved $36,400 in interest on a $100,000 balance.

Strategy 7: Refinance to a Shorter Repayment Term

If you are in the repayment period and want to lock in a faster payoff with a fixed rate, refinancing your HELOC balance into a home equity loan with a shorter term is worth exploring.

This strategy trades the variable rate risk of a HELOC for the payment certainty of a fixed-rate installment loan, while also giving you a defined payoff date.

For example, refinancing a $75,000 HELOC balance into a 10-year fixed home equity loan at 8.25% results in:

- Monthly payment: $921

- Total interest paid: $35,520

- Definite payoff: 10 years from closing

Compare that to continuing on a 15-year HELOC repayment at 8.75%:

- Monthly payment: $745

- Total interest paid: $59,100

- Interest premium for the longer term: $23,580

The home equity loan payment is $176/month higher, but saves $23,580 in total interest and gives you a guaranteed payoff date with no variable rate risk.

Closing costs for a home equity loan are typically $500–$2,000. Factor those in when calculating whether refinancing makes financial sense for your specific balance and timeline.

Strategy 8: The HELOC Payoff Sprint (Final 24 Months)

If you are within two years of your HELOC payoff date — or you want to set a target payoff date — consider a structured payoff sprint. This means temporarily redirecting every available dollar from discretionary spending directly to your HELOC principal for a defined 24-month period.

This is not a permanent lifestyle change. It is a time-limited intensity that eliminates the debt entirely and then frees up all those payments permanently.

What a 24-month sprint might look like for a homeowner with a $40,000 remaining HELOC balance at 8.75%:

- Minimum repayment payment: $400/month

- Sprint payment (including redirected discretionary): $1,800/month

- Payoff timeline: 23 months

- Interest saved vs. minimum payment schedule: $18,400

The psychological benefit of a sprint is significant too. Having a defined end date makes temporary sacrifice feel purposeful rather than open-ended.

Combining Strategies: The Maximum Impact Approach

No rule says you can only use one strategy. The borrowers who eliminate HELOC debt fastest typically combine two or three approaches simultaneously.

A practical combination for most homeowners:

Base: Fixed extra monthly payment of $200–$300 (Strategy 1) Add: Biweekly payment schedule (Strategy 2) Add: Any tax refund or bonus as lump sum (Strategy 3) Add: Round up to nearest $50 (Strategy 5)

This combination on a $100,000 HELOC at 8.75% with 15 years remaining could realistically cut the payoff timeline to 8–9 years and save $45,000–$55,000 in total interest — without requiring a dramatic change to your monthly budget.

What to Do After Your HELOC is Paid Off

When your HELOC balance hits zero, you have a decision to make: close the line or keep it open.

Keeping it open gives you a zero-cost financial safety net. A HELOC with a zero balance costs you nothing (beyond any small annual fee your lender charges) and gives you immediate access to funds if a true emergency arises — job loss, major home repair, medical expense. Many financial advisors recommend keeping it open for exactly this reason.

Closing it simplifies your financial picture and removes any temptation to re-borrow. If your lender charges an annual fee and you are confident you will not need the credit line, closing makes sense. Just be aware of the early termination fee window if your HELOC is relatively new.

If you decide to keep it open, make a firm commitment about what circumstances would justify drawing from it again — and stick to that commitment.

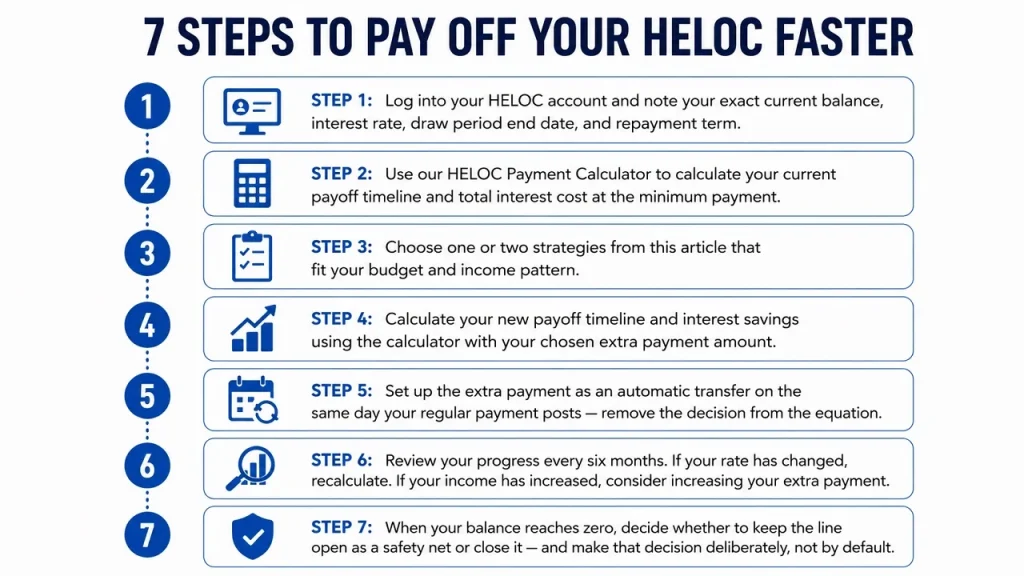

Your HELOC Payoff Action Plan

Here is a simple step-by-step plan to start paying off your HELOC faster starting this month:

Step 1: Log into your HELOC account and note your exact current balance, interest rate, draw period end date, and repayment term.

Step 2: Use our HELOC Payment Calculator to calculate your current payoff timeline and total interest cost at the minimum payment.

Step 3: Choose one or two strategies from this article that fit your budget and income pattern.

Step 4: Calculate your new payoff timeline and interest savings using the calculator with your chosen extra payment amount.

Step 5: Set up the extra payment as an automatic transfer on the same day your regular payment posts — remove the decision from the equation.

Step 6: Review your progress every six months. If your rate has changed, recalculate. If your income has increased, consider increasing your extra payment.

Step 7: When your balance reaches zero, decide whether to keep the line open as a safety net or close it — and make that decision deliberately, not by default.

The Bottom Line

Paying off a HELOC faster is one of the highest-return financial moves available to a homeowner. Your interest rate is your guaranteed return — every extra dollar applied to principal saves you that same rate in future interest charges, with zero risk.

You do not need a dramatic budget overhaul to make meaningful progress. An extra $200/month, a biweekly payment schedule, and one lump sum from a tax refund can together cut years off your timeline and save tens of thousands of dollars.

The key is starting now. Every month you delay is another month of full-balance interest accrual that you will never get back.

Use our HELOC Payment Calculator to see your exact payoff date and total interest cost today — then run the numbers with extra payments to see how quickly the picture changes.