HELOC Amortization Schedule Explained (With Examples)

If you have ever looked at a mortgage statement, you have seen an amortization schedule — the table that shows exactly how much of each payment goes toward interest, how much reduces your principal, and what your remaining balance is after every payment.

A HELOC amortization schedule works on the same principle, but with one important difference: a HELOC has two distinct phases — the draw period and the repayment period — and the math works differently in each one.

Most HELOC borrowers never look at their amortization schedule in detail. That is a mistake. Understanding exactly how your payments are applied month by month is what separates borrowers who manage their HELOC strategically from those who get blindsided by payment shock, unexpected interest costs, or a balance that never seems to move.

This article explains how HELOC amortization works, walks through real month-by-month examples for both periods, and shows you how extra principal payments reshape the entire schedule in your favor.

What is an Amortization Schedule?

An amortization schedule is a complete table of every payment over the life of a loan. For each payment period it shows:

- Payment number — which month you are in

- Beginning balance — what you owed at the start of the period

- Payment amount — your total payment for the month

- Interest portion — how much of your payment covers interest charges

- Principal portion — how much of your payment reduces your balance

- Ending balance — what you owe after the payment is applied

In a traditional fixed mortgage, every payment is the same dollar amount from month one to month 360, but the split between interest and principal shifts over time. Early payments are mostly interest. Late payments are mostly principal. That shift is what amortization means — the gradual paydown of debt through scheduled payments.

A HELOC amortization schedule is more complex because your balance can change throughout the draw period as you draw and repay funds, and because your payment type changes completely when the repayment period begins.

How HELOC Amortization Works in the Draw Period

During the draw period — typically the first 5 to 10 years — most HELOCs require interest-only minimum payments. This means the amortization schedule during the draw period looks very different from a traditional loan schedule.

In a standard loan amortization, every payment chips away at the principal. In a HELOC draw period with interest-only payments, the principal does not move unless you deliberately pay extra. Your amortization schedule during this phase essentially shows the same ending balance month after month — with 100% of your payment going to interest.

Here is what the draw period amortization schedule looks like for a $75,000 HELOC draw at 8.75% with interest-only minimum payments:

Draw Period Schedule — $75,000 Balance at 8.75% (Interest-Only Minimum)

| Month | Beginning Balance | Payment | Interest | Principal | Ending Balance |

|---|---|---|---|---|---|

| 1 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 2 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 3 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 6 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 12 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 24 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 60 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

| 120 | $75,000.00 | $546.88 | $546.88 | $0.00 | $75,000.00 |

The table is stark and intentional. After 120 months — a full 10-year draw period — of paying $546.88 every single month, the balance is exactly where it started: $75,000.

Total paid over 10 years: $65,625 in interest. Balance remaining: $75,000.

This is the financial reality of interest-only draw period payments laid out in black and white. You have paid $65,625 and own nothing more of your home than when you started.

How HELOC Amortization Works in the Repayment Period

When the draw period ends, the amortization schedule changes dramatically. Your outstanding balance is now fully amortized over the repayment term — typically 10, 15, or 20 years — with each payment covering both principal and interest.

This is where the schedule starts to look like a traditional mortgage amortization. Early payments are still weighted toward interest, but principal reduction begins immediately and grows with every passing month.

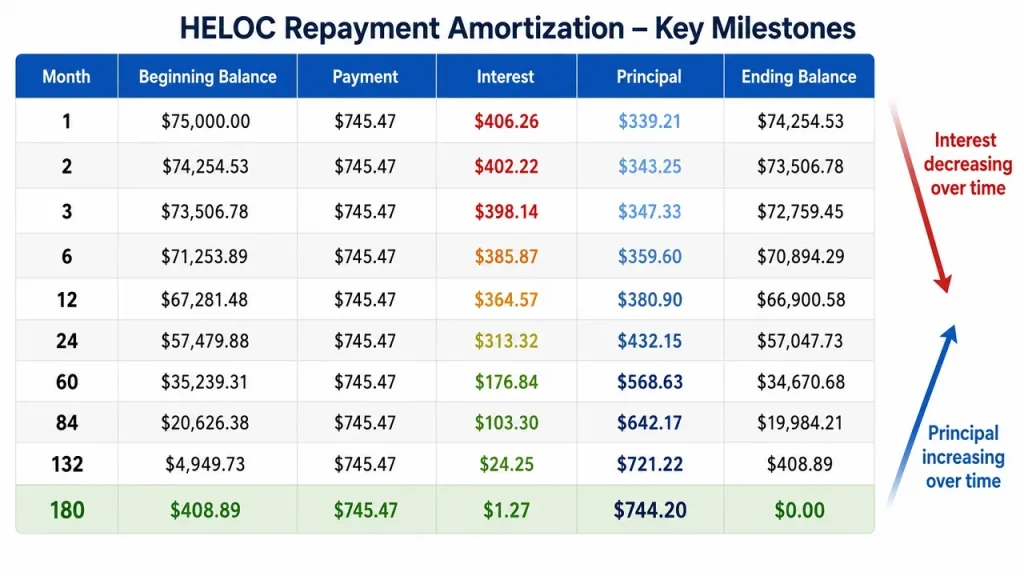

Here is the repayment period amortization schedule for the same $75,000 balance at 8.75% over a 15-year repayment term:

Repayment Period Schedule — $75,000 at 8.75%, 15-Year Term

| Month | Beginning Balance | Payment | Interest | Principal | Ending Balance |

|---|---|---|---|---|---|

| 1 | $75,000.00 | $745.47 | $546.88 | $198.60 | $74,801.40 |

| 2 | $74,801.40 | $745.47 | $545.43 | $200.04 | $74,601.36 |

| 3 | $74,601.36 | $745.47 | $543.97 | $201.50 | $74,399.86 |

| 6 | $73,789.00 | $745.47 | $538.07 | $207.40 | $73,581.60 |

| 12 | $72,132.00 | $745.47 | $526.13 | $219.34 | $71,912.66 |

| 24 | $68,622.00 | $745.47 | $500.44 | $245.03 | $68,376.97 |

| 36 | $64,798.00 | $745.47 | $472.57 | $272.90 | $64,525.10 |

| 60 | $55,698.00 | $745.47 | $406.26 | $339.21 | $55,358.79 |

| 84 | $44,618.00 | $745.47 | $325.51 | $419.96 | $44,198.04 |

| 108 | $31,189.00 | $745.47 | $227.57 | $517.90 | $30,671.10 |

| 132 | $15,012.00 | $745.47 | $109.51 | $635.96 | $14,376.04 |

| 180 | $744.06 | $745.47 | $5.43 | $740.04 | $0.00 |

Several things stand out in this schedule worth understanding closely.

Month 1 of repayment: Your $745.47 payment splits as $546.88 interest and only $198.60 principal. That means 73% of your first repayment payment still goes to interest — almost identical to what you were paying in interest-only minimums during the draw period.

Month 60 (year 5 of repayment): The split has improved — $406.26 interest, $339.21 principal. You are now putting 45% of each payment toward actual debt reduction.

Month 120 (year 10 of repayment): $227.57 interest, $517.90 principal. Now 69% of your payment reduces the balance.

Month 180 (final payment): $5.43 interest, $740.04 principal. Your last payment is almost entirely principal. The debt is gone.

This gradual shift from interest-heavy to principal-heavy is the defining characteristic of amortization — and it explains why extra principal payments made early in the repayment period have such an outsized impact on total interest costs.

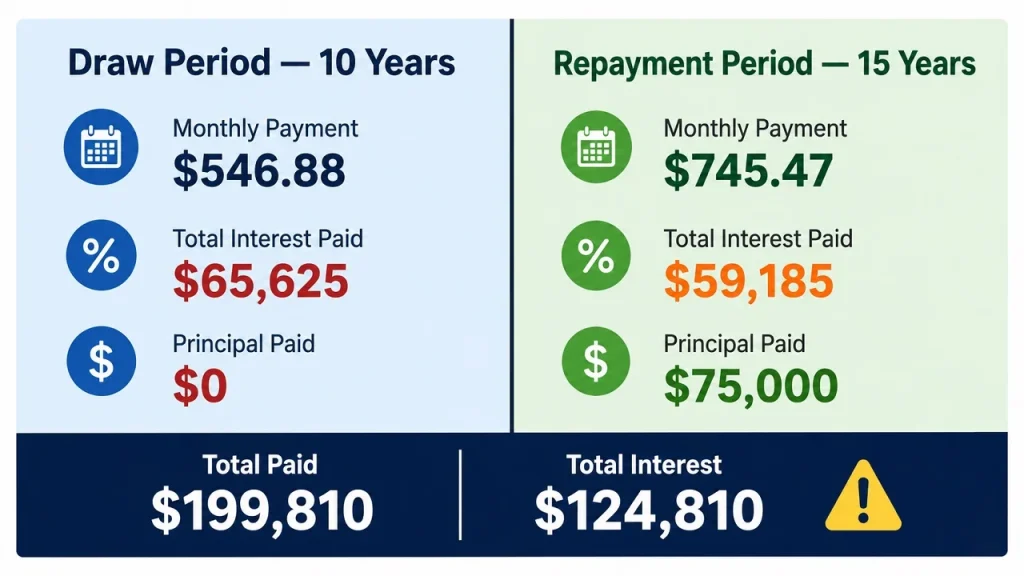

The Full Picture: Draw Period + Repayment Period Combined

Now let us look at the complete financial picture of this $75,000 HELOC from opening day to final payment — assuming interest-only minimums throughout the draw period followed by full amortization in repayment.

| Phase | Duration | Monthly Payment | Total Paid | Principal Paid | Interest Paid |

|---|---|---|---|---|---|

| Draw period (interest-only) | 10 years | $546.88 | $65,625 | $0 | $65,625 |

| Repayment period | 15 years | $745.47 | $134,185 | $75,000 | $59,185 |

| Total | 25 years | — | $199,810 | $75,000 | $124,810 |

A borrower who took out $75,000 and paid minimums throughout will have paid $199,810 total — $124,810 in interest alone — before the debt is eliminated. They paid more in interest than they originally borrowed.

This is not a scare tactic. It is the straightforward math of long-term variable-rate borrowing, and it is exactly why understanding your amortization schedule — and acting on it — matters so much.

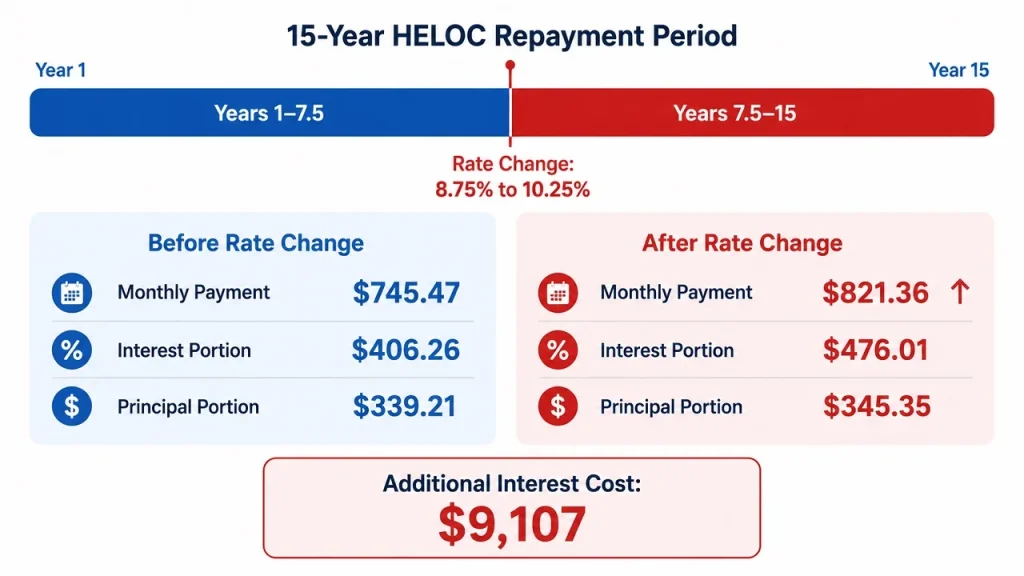

How a Variable Rate Affects Your Amortization Schedule

Unlike a fixed mortgage, a HELOC’s variable rate means your amortization schedule is not static. Every time your interest rate changes — which happens whenever the prime rate moves — your payment amount, interest portion, and payoff timeline all shift.

Most lenders recalculate your payment based on your current balance and current rate at the start of each billing cycle. This means your amortization schedule is technically recalculated every month that your rate changes.

Here is what a rate change does to the $75,000 repayment schedule mid-stream:

Scenario: 5 years into the 15-year repayment period, with a remaining balance of $55,698, the interest rate increases from 8.75% to 10.25%.

| Before Rate Change | After Rate Change | |

|---|---|---|

| Remaining balance | $55,698 | $55,698 |

| Interest rate | 8.75% | 10.25% |

| Monthly payment | $745.47 | $821.36 |

| Monthly interest portion | $406.26 | $476.01 |

| Monthly principal portion | $339.21 | $345.35 |

| Remaining payoff timeline | 10 years | 10 years 3 months |

A 1.5% rate increase on a $55,698 balance adds $75.89/month to the payment and $9,107 to the total interest cost over the remaining term. This is the compounding impact of variable rate exposure — and it reinforces why tracking your amortization schedule actively, not just at closing, is important.

Use our HELOC Payment Calculator to recalculate your schedule whenever your rate changes.

How Extra Principal Payments Reshape the Amortization Schedule

This is where understanding your amortization schedule becomes genuinely empowering rather than just informative. Extra principal payments do not just save you interest — they restructure your entire schedule by reducing every future month’s interest calculation.

Here is a direct comparison of three payment strategies on a $75,000 HELOC entering repayment at 8.75% with a 15-year term:

Strategy A: Minimum Payment Only ($745.47/month)

| Milestone | Timeline |

|---|---|

| Balance below $60,000 | Month 38 |

| Balance below $40,000 | Month 87 |

| Balance below $20,000 | Month 142 |

| Paid off | Month 180 (15 years) |

| Total interest paid | $59,185 |

Strategy B: $200 Extra Per Month ($945.47/month)

| Milestone | Timeline |

|---|---|

| Balance below $60,000 | Month 28 |

| Balance below $40,000 | Month 65 |

| Balance below $20,000 | Month 105 |

| Paid off | Month 133 (11 years 1 month) |

| Total interest paid | $43,820 |

| Interest saved | $15,365 |

| Time saved | 3 years 11 months |

Strategy C: $500 Extra Per Month ($1,245.47/month)

| Milestone | Timeline |

|---|---|

| Balance below $60,000 | Month 20 |

| Balance below $40,000 | Month 47 |

| Balance below $20,000 | Month 75 |

| Paid off | Month 100 (8 years 4 months) |

| Total interest paid | $29,600 |

| Interest saved | $29,585 |

| Time saved | 6 years 8 months |

Adding $200/month saves nearly $15,400 in interest and cuts almost four years off the repayment timeline. Adding $500/month cuts the timeline by more than six and a half years and saves $29,585 — nearly 40% of the original loan amount saved in interest alone.

Model your own extra payment scenarios using our HELOC Payment Calculator.

Reading Your Own HELOC Amortization Schedule

Most lenders provide access to your amortization schedule through your online account portal. If yours does not display it automatically, you can request it directly from your lender — they are required to provide it upon request.

When you pull up your schedule, here is what to look for:

Current balance vs. original draw amount. If you have been paying interest-only and your balance matches your original draw, your schedule confirms you have made zero progress on principal. That is your baseline.

Interest-to-principal ratio in the current month. Look at your most recent payment row. What percentage went to interest vs. principal? If the number is above 60% interest, you are still in the early stages of amortization where extra payments have the highest impact.

Projected payoff date. Your schedule should show the month and year your balance reaches zero under the minimum payment scenario. That is your starting point for planning.

Total remaining interest. Sum the interest column from today to the final payment. That number represents the maximum interest you will pay if you never make an extra payment. It also represents your maximum possible savings from extra principal payments.

Once you have these four numbers, you have everything you need to make an informed decision about how aggressively to pay down your HELOC.

Draw Period Amortization With Extra Principal Payments

The amortization benefit of extra payments is not limited to the repayment period. Paying extra principal during the draw period is actually even more powerful — because it reduces the balance that enters repayment, which in turn reduces every single repayment period payment for the next 15–20 years.

Here is what happens to the $75,000 draw period example when the borrower adds $300/month in extra principal payments during the 10-year draw period:

| Interest-Only Minimum | $300/Month Extra Principal | |

|---|---|---|

| Draw period payments | $546.88/month | $846.88/month |

| Balance at end of draw period | $75,000 | $39,000 |

| Repayment period payment | $745.47/month | $387/month |

| Total interest (full term) | $124,810 | $72,400 |

| Total savings | — | $52,410 |

Adding $300/month during the draw period — before repayment even begins — saves over $52,000 in total interest and cuts the repayment payment nearly in half. That is the compounding power of early principal reduction captured in a single comparison.

HELOC Amortization Schedule FAQ

Can I get my HELOC amortization schedule from my lender? Yes. Log into your online account and look for a “payment schedule,” “loan details,” or “amortization schedule” section. If it is not available online, call your lender and request it in writing. They are required to provide it.

Does my HELOC amortization schedule change when rates change? Yes. Because HELOCs carry variable rates, your schedule recalculates whenever your rate changes. The new schedule will reflect your current balance, current rate, and remaining term.

What happens to my amortization schedule if I make a large lump sum payment? Your lender recalculates the schedule based on your new lower balance. Your monthly payment may decrease, or your payoff date may move earlier — depending on how your lender applies the payment. Always confirm with your lender whether a lump sum payment reduces your required monthly payment or shortens your term.

Why does so much of my early repayment payment go to interest? This is how amortization works with any interest-bearing loan. Interest is calculated on the outstanding balance — which is highest at the beginning of repayment. As your balance decreases, the interest portion of each payment shrinks and the principal portion grows. It is not a lender trick; it is the mathematics of compound interest working against you early and for you later.

Can I ask my lender to recast my HELOC after a large payment? Some lenders offer recasting — recalculating your required monthly payment based on your new lower balance — after a significant lump sum payment. Not all lenders offer this. Ask specifically whether recasting is available and whether there is a fee to do it.

The Bottom Line

A HELOC amortization schedule is not just a bureaucratic document — it is a financial roadmap that shows you exactly where your money goes every month, how long until you are debt-free, and how much you can save by changing your payment behavior.

The most important things to take away:

- Interest-only draw period payments produce a flat amortization schedule where your balance never moves — understand this before you commit to minimum payments for years

- Early repayment period payments are still heavily weighted toward interest — extra principal payments at this stage have their highest impact

- A variable rate means your schedule is not fixed — recalculate whenever your rate changes

- Extra principal payments during the draw period are the single most powerful way to reduce your total interest cost because they shrink the balance that enters full amortization

Use our HELOC Payment Calculator to build your own amortization schedule, model extra payment scenarios, and see your exact payoff date and total interest cost under any scenario you choose.