Using a HELOC for Home Renovation: A Financial Guide (2026)

Home renovation is the most common reason American homeowners open a HELOC — and often the most financially sound one. You are borrowing against an asset to improve that same asset. Done right, the project adds value to your home, the interest may be tax deductible, and the flexible draw structure of a HELOC matches how renovation costs actually arrive: in stages, over months, not all at once.

Done carelessly, a renovation HELOC can saddle you with a large balance, a payment shock you were not prepared for, and improvements that cost far more than the value they added.

This guide covers the complete picture — how to fund a renovation with a HELOC intelligently, which projects make financial sense, which ones do not, what the real costs look like, and how to manage the borrowing so you come out ahead.

Why a HELOC Is Well-Suited for Home Renovation

Of all the ways to finance a home renovation — credit cards, personal loans, cash-out refinancing, home equity loans — a HELOC matches the nature of renovation spending better than any other product.

Here is why.

Renovation costs rarely arrive as a single invoice. A kitchen remodel unfolds in phases: demolition, rough plumbing and electrical, framing, drywall, cabinets, countertops, appliances, finishing. Each phase has its own contractor, its own timeline, and its own cost. The total spend might be $65,000 — but that $65,000 arrives over 8 to 14 months in uneven chunks.

A HELOC lets you draw exactly what you need, when you need it. In month one you draw $8,000 for demo and rough work. In month four you draw $22,000 for cabinets. In month nine you draw $15,000 for countertops and appliances. You pay interest only on what you have actually drawn — not on the full $65,000 from day one.

Compare that to a home equity loan, where you would receive the full $65,000 at closing and pay interest on all of it from month one — including the $40,000 sitting in your bank account for months two through twelve waiting to be spent.

On a $65,000 renovation unfolding over 12 months, the staged HELOC drawing typically saves $2,500 to $4,500 in interest compared to a lump-sum home equity loan — purely from borrowing only what you need, when you need it.

What Renovation Projects Make Financial Sense to Fund With a HELOC

Not all home improvements deliver equal value. The financial case for using a HELOC is strongest when the project either increases your home’s market value meaningfully, reduces ongoing costs, or both.

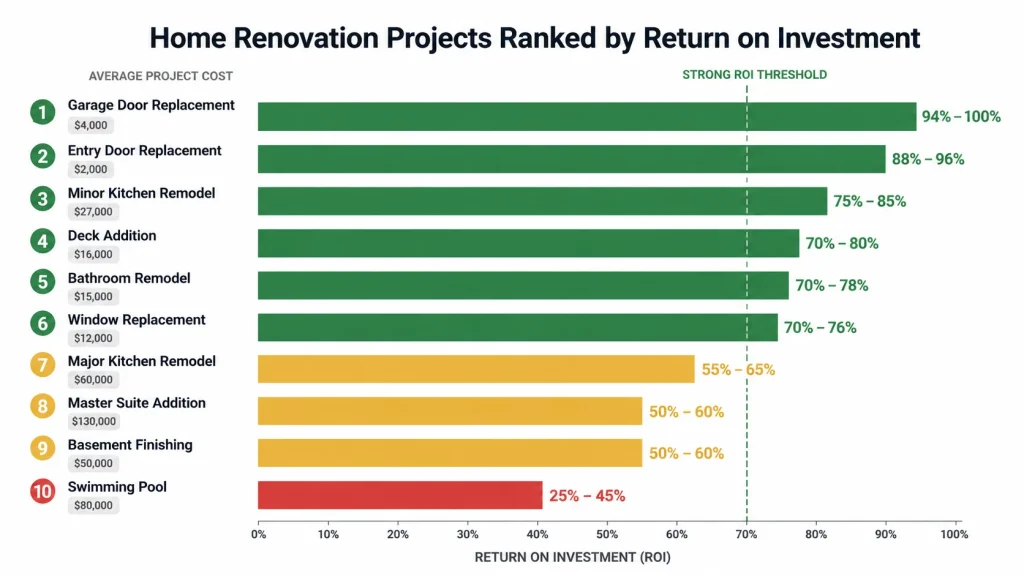

Here are the renovations with the best return on investment (ROI) based on Remodeling Magazine’s 2026 Cost vs. Value report and general market data:

High ROI Projects (Recoup 70–100%+ of Cost)

Minor kitchen remodel: A cosmetic refresh — new cabinet faces, updated hardware, new countertops, modern appliances — rather than a full gut renovation. Average cost: $28,000–$35,000. Average resale value added: $21,000–$28,000. ROI: 75–85%.

Garage door replacement: One of the highest ROI projects year after year. Average cost: $4,500–$6,000. Average resale value added: $4,000–$6,000. ROI: 90–100%.

Entry door replacement (steel): A new front entry door consistently adds curb appeal and perceived value. Average cost: $2,500–$4,500. ROI: 80–95%.

Deck addition (wood): Outdoor living space adds significant perceived and appraised value in most markets. Average cost: $18,000–$25,000. Average value added: $13,000–$18,000. ROI: 65–75%.

Bathroom remodel (midrange): Updated fixtures, new tile, modern vanity. Average cost: $25,000–$35,000. Average value added: $18,000–$25,000. ROI: 65–75%.

Window replacement: Energy efficiency and curb appeal combined. Average cost: $20,000–$30,000 for whole-house. ROI: 65–75%.

Moderate ROI Projects (Recoup 50–70% of Cost)

Major kitchen remodel: Full gut renovation with custom cabinets, premium appliances, structural changes. Average cost: $75,000–$130,000. ROI: 50–65%. The major kitchen remodel consistently underperforms the minor remodel on ROI despite costing 3–4x more.

Master suite addition: Adding a primary bedroom and bathroom. Average cost: $130,000–$200,000+. ROI: 50–60%.

Basement finishing: Converting unfinished basement to livable space. Average cost: $40,000–$75,000. ROI: 55–70% depending on market.

Lower ROI Projects (Recoup Under 50% of Cost)

Swimming pool: Highly market-dependent. In hot climates (Florida, Arizona, Texas), pools add meaningful value. In cold-weather markets, they often add very little and can reduce marketability. Average cost: $55,000–$100,000. ROI: 25–50% nationally.

Sunroom addition: Popular but rarely adds equivalent appraised value. Average cost: $35,000–$75,000. ROI: 40–55%.

Luxury bathroom additions: High-end fixtures, custom tile, heated floors. The premium over a standard bathroom remodel rarely translates to equivalent value increase. ROI: 40–55%.

The important caveat: ROI is relevant if you plan to sell within 5 years. If you plan to stay in the home for 10–20 years, personal enjoyment of the improvement has real value that pure ROI calculations do not capture. A pool you use every summer for 15 years may be worth it even at 35% ROI. A kitchen you love cooking in for 20 years may justify a 55% ROI.

Real Cost Example: $60,000 Kitchen Renovation

Let us walk through a complete financial picture of a $60,000 kitchen renovation funded by a HELOC.

Homeowner profile:

- Home value: $480,000

- Mortgage balance: $290,000

- HELOC credit limit approved: $118,000 (85% CLTV)

- HELOC rate: 8.75% variable

- Draw timeline: 10 months

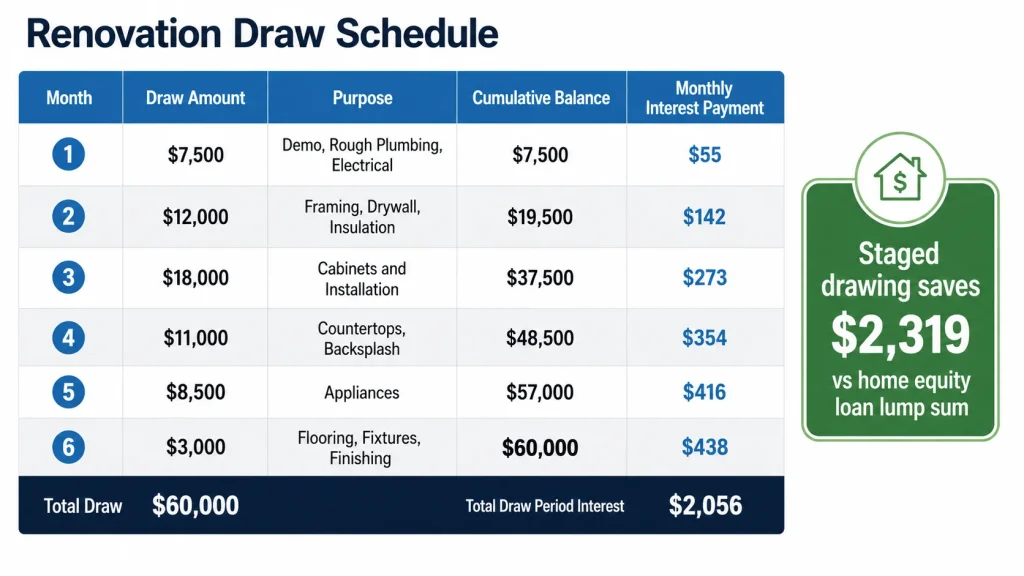

Draw schedule:

| Month | Draw Amount | Purpose | Cumulative Balance |

|---|---|---|---|

| Month 1 | $7,500 | Demo, rough plumbing, electrical | $7,500 |

| Month 3 | $12,000 | Framing, drywall, insulation | $19,500 |

| Month 5 | $18,000 | Cabinets and installation | $37,500 |

| Month 7 | $11,000 | Countertops and backsplash | $48,500 |

| Month 9 | $8,500 | Appliances | $57,000 |

| Month 10 | $3,000 | Flooring, fixtures, finishing | $60,000 |

Interest-only payments during draw period (10 months):

| Month | Balance | Monthly Interest Payment |

|---|---|---|

| Month 1–2 | $7,500 | $55 |

| Month 3–4 | $19,500 | $142 |

| Month 5–6 | $37,500 | $273 |

| Month 7–8 | $48,500 | $354 |

| Month 9 | $57,000 | $416 |

| Month 10 | $60,000 | $438 |

Total interest paid during draw phase (10 months): approximately $2,056

Compare this to a home equity loan for the full $60,000 from day one at 8.75%: Interest on $60,000 for 10 months: $4,375

The staged HELOC draw saves $2,319 in interest during the renovation phase alone.

Repayment period (15 years at 8.75% on $60,000 balance):

- Monthly payment: $596

- Total interest over 15-year repayment: $47,280

- Total financing cost including draw period interest: $49,336

Home value impact:

- Pre-renovation value: $480,000

- Estimated post-renovation value: $528,000–$540,000 (conservative 10–12.5% increase)

- Renovation cost: $60,000

- Net equity gain: $8,000–$20,000

The renovation adds more value than it costs — even before accounting for the quality-of-life improvement over the years of living in the renovated space.

Use our HELOC Payment Calculator to model your own renovation draw schedule and repayment costs.

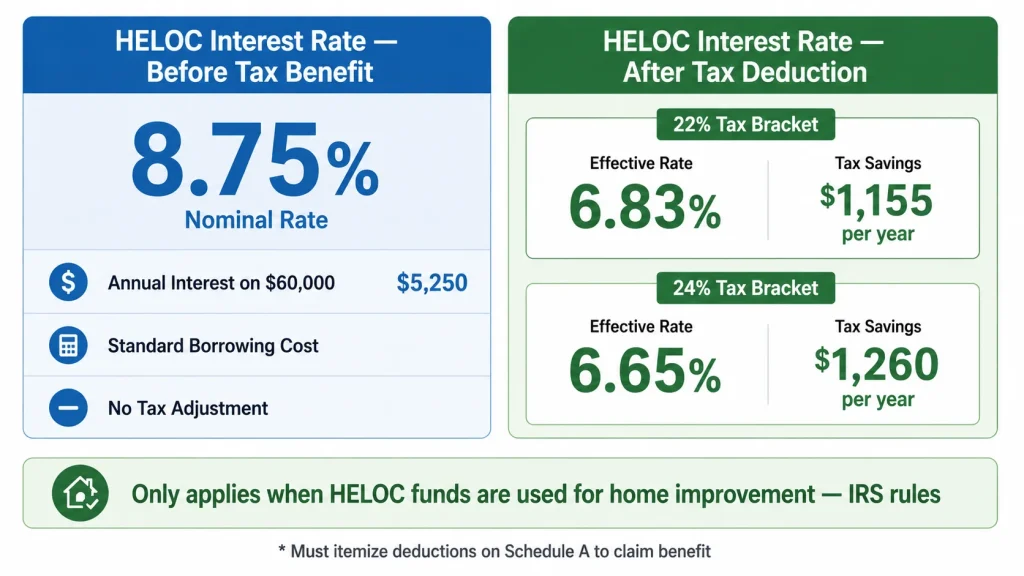

The Tax Deductibility Advantage

One of the strongest financial arguments for using a HELOC specifically for home renovation — rather than for other purposes — is the potential tax deductibility of the interest.

Under current IRS rules (Tax Cuts and Jobs Act of 2017, currently extended), HELOC interest is tax deductible when the funds are used to buy, build, or substantially improve the home that secures the loan. Home renovation clearly qualifies under this standard.

The deduction applies to the first $750,000 of combined home acquisition and improvement debt for joint filers ($375,000 for married filing separately).

What this means in dollars:

For a homeowner in the 22% federal tax bracket with $60,000 drawn on a HELOC at 8.75%:

- Annual interest cost: $5,250

- Tax deduction value (22%): $1,155

- Effective after-tax interest rate: 6.83%

For a homeowner in the 24% bracket:

- Tax deduction value (24%): $1,260

- Effective after-tax rate: 6.65%

This after-tax rate advantage does not apply to credit cards, personal loans, or HELOC funds used for non-home purposes. It is specific to home improvement use — which makes a renovation HELOC one of the most tax-efficient ways to borrow money available to homeowners.

You must itemize deductions on Schedule A to claim this benefit. For many homeowners, the standard deduction ($29,200 for joint filers in 2026) exceeds their itemized deductions, making the HELOC interest deduction effectively unavailable. Confirm your specific situation with a tax advisor.

How to Structure Your Renovation HELOC Smartly

Opening a HELOC for renovation is straightforward. Managing it well over the project timeline requires a little more intention.

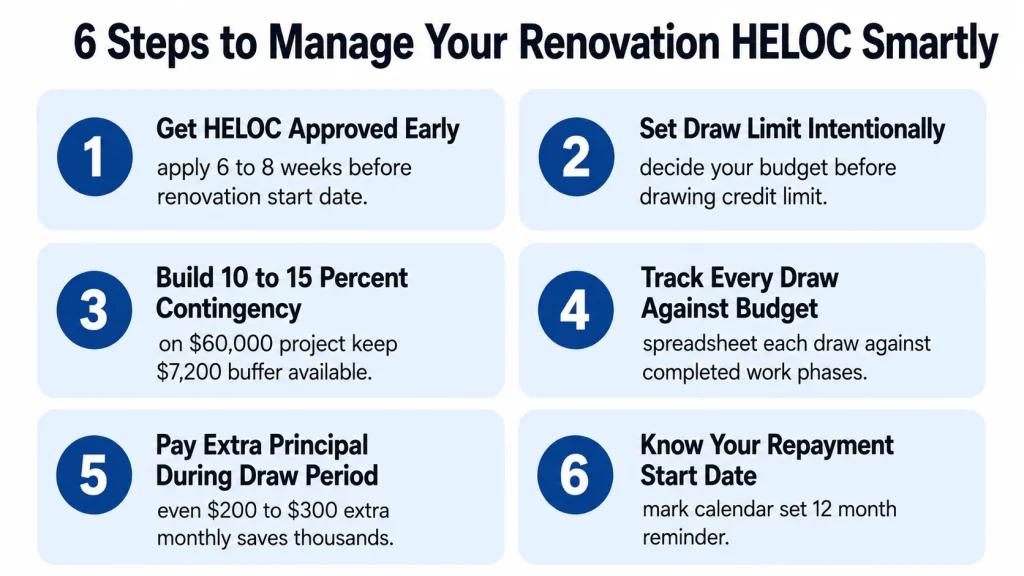

Get the HELOC Approved Before You Need It

Apply for the HELOC 6 to 8 weeks before your renovation start date. HELOC approval takes 3 to 6 weeks — if you wait until your contractor is ready to start, you may be scrambling. Approval lead time also gives you leverage to negotiate with contractors when you have confirmed financing ready.

Set Your Draw Limit Intentionally

Your approved credit limit may be $120,000 — but that does not mean you should plan to use $120,000 on a $60,000 renovation. Decide upfront what your renovation budget is and treat that as your actual limit. The availability of more credit is not a reason to expand the scope of the project beyond what you planned and can afford.

Build a 10–15% Contingency Into Your Budget

Renovation projects almost always encounter unexpected costs — hidden water damage, electrical issues that do not meet code, materials delays requiring substitutions. A 10–15% contingency buffer built into your HELOC draw plan keeps the project on track without requiring emergency re-budgeting mid-project.

On a $60,000 renovation, a 12% contingency is $7,200 — meaning you should have $67,200 of credit available, not exactly $60,000.

Track Every Draw Against Your Budget

Maintain a simple spreadsheet tracking each HELOC draw against the corresponding work phase. This discipline does two things: it confirms that draws match actual completed work (not just contractor invoices), and it catches scope creep early before it becomes a financial problem.

Start Paying Down Principal During the Draw Period

This is the most financially impactful thing you can do. Once your balance stabilizes — when the major project phases are complete and you are not drawing new funds — begin adding extra principal payments above the interest-only minimum.

Even $200–$300/month in extra principal during the final months of the draw period meaningfully reduces the balance entering repayment. On a $60,000 balance, paying $300/month extra for 6 months before repayment begins reduces your balance by $1,800 — saving approximately $1,795 in total repayment interest and cutting nearly 3 months off the payoff timeline.

Know Your Repayment Start Date

Mark your HELOC draw period end date on your calendar the day you close. Set a reminder 12 months before that date to evaluate your repayment readiness. The draw period end date is not an abstract future event — it is a specific date when your minimum payment increases by 35–40%.

What to Watch Out For: Common HELOC Renovation Mistakes

Over-Improving for the Neighborhood

The most reliable way to destroy a renovation’s ROI is to spend more than the market will support. A $150,000 kitchen in a neighborhood where comparable homes sell for $350,000 will not produce $150,000 in added value — because buyers in that price range are not paying for a kitchen at that level.

Before budgeting a major renovation, research recent sales of comparable homes in your neighborhood. If the upgrades you are planning push your home significantly above the median sale price in your immediate area, expect a lower ROI — and factor that into whether the project makes financial sense at the budget you are considering.

Confusing Wants With Investments

Not every renovation is an investment. A $40,000 home theater, a custom wine cellar, or a dedicated pet spa are personal luxury improvements that add little to no market value. There is nothing wrong with funding personal enjoyment — but be honest with yourself about whether you are borrowing for value creation or personal preference. The financial math looks very different for each.

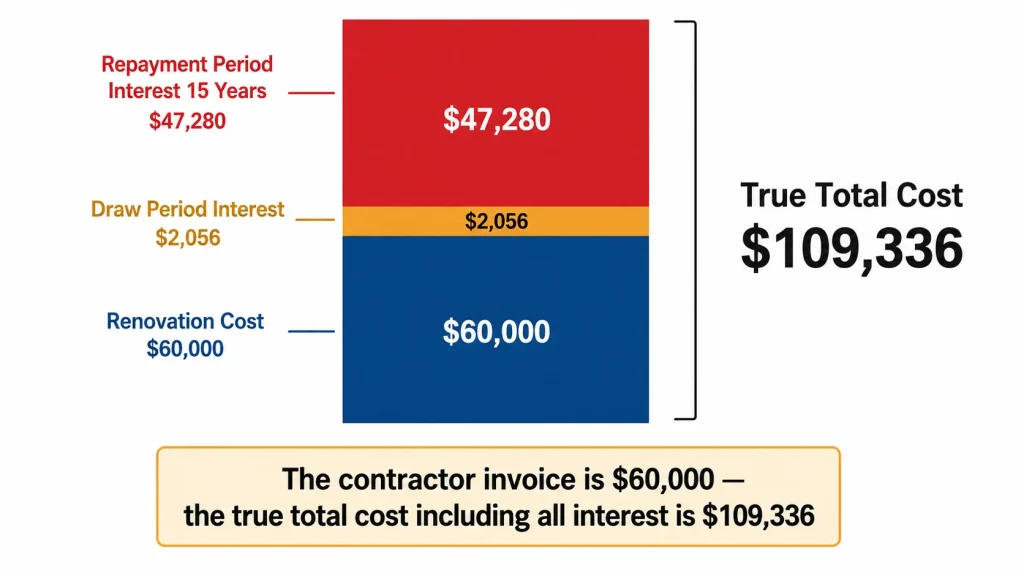

Ignoring the Repayment Period Cost

The renovation feels complete in month 10. The HELOC repayment period runs for another 15 years. Many homeowners mentally close out the renovation when the last contractor leaves and stop thinking about the ongoing financial obligation.

The $60,000 HELOC balance at 8.75% over 15 years costs $47,280 in repayment interest. That is a real, ongoing cost of the renovation that belongs in any honest total project cost calculation.

True total cost of a $60,000 renovation funded by HELOC:

- Renovation cost: $60,000

- Draw period interest: $2,056

- Repayment period interest: $47,280

- Total true cost: $109,336

That does not make the renovation a bad decision — if it adds $40,000+ in home value and provides 15 years of enjoyment. But the $60,000 invoice from the contractor is not the full number.

Not Comparing Contractor Quotes

A HELOC approval for $100,000 can create a psychological sense of having $100,000 to spend. The discipline of getting three contractor quotes for every major work phase — and choosing based on quality and references, not on the fact that the credit line can cover the highest bid — is especially important when borrowing against your home.

HELOC vs. Other Renovation Financing: Quick Comparison

| Method | Rate (2026) | Closing Cost | Best For |

|---|---|---|---|

| HELOC | 8.25%–10.50% variable | $200–$2,000 | Multi-phase projects over $20,000 |

| Home equity loan | 7.50%–9.50% fixed | $500–$3,000 | Single known cost, fixed payment preferred |

| Cash-out refinance | 6.75%–7.50% fixed | $3,000–$6,000+ | Large amounts, high existing mortgage rate |

| Personal loan | 7.99%–22.99% fixed | $0–5% origination | Under $20,000, no home equity, fast funding |

| Credit card (0% promo) | 0% for 12–21 months | None | Under $10,000, paid off within promo period |

| Credit card (standard) | 19.99%–32.99% | None | Avoid for anything carried more than 30 days |

For most homeowners with adequate equity and a renovation project over $20,000 unfolding over multiple months, the HELOC wins on total cost. The home equity loan makes more sense for a single defined cost. The personal loan covers smaller projects or situations without equity access.

The Bottom Line

A HELOC is one of the most financially efficient ways to fund a home renovation when you have the equity to support it, the income to manage the payments, and the discipline to borrow only what the project requires.

The staged draw structure matches how renovations actually spend. The lower rate compared to credit cards and personal loans saves thousands. The potential tax deductibility reduces the effective cost further. And when the project adds genuine value to the home, you are improving the collateral securing the very loan you used to pay for it.

The risks are real too — payment shock, over-improvement, treating the credit line as a blank check, and ignoring the full repayment cost. Managing those risks requires planning and discipline, not just good contractor selection.

Before you draw the first dollar, know your draw schedule, know your contingency budget, know your repayment start date, and know what your monthly payment will be when full amortization begins. Those four pieces of information are what separates a renovation that builds wealth from one that quietly erodes it.

Use our HELOC Payment Calculator to model your renovation draw schedule, see your interest costs during the draw period, and calculate your exact repayment payment when the project is complete.