Using a HELOC for College Tuition: Pros & Cons

College is expensive. In 2026, the average annual cost of a four-year public university for in-state students is approximately $28,000 — including tuition, fees, room, and board. Private universities average $60,000 or more per year. For a family with limited savings, the math is stark: four years at a public university is $112,000. At a private school, it can easily reach $240,000 or more.

When savings and financial aid fall short, families look for ways to bridge the gap. A HELOC is one option that comes up regularly — and with good reason. The interest rates are lower than most private student loans and many personal loans, the credit line can cover costs year by year as tuition bills arrive, and for families with significant home equity, the credit limit can be substantial.

But using your home equity to fund education is a more complex decision than it first appears — with financial trade-offs, tax implications, and risks that are genuinely different from other HELOC uses. This guide covers the complete picture so you can make an informed decision.

How a HELOC Works for College Funding

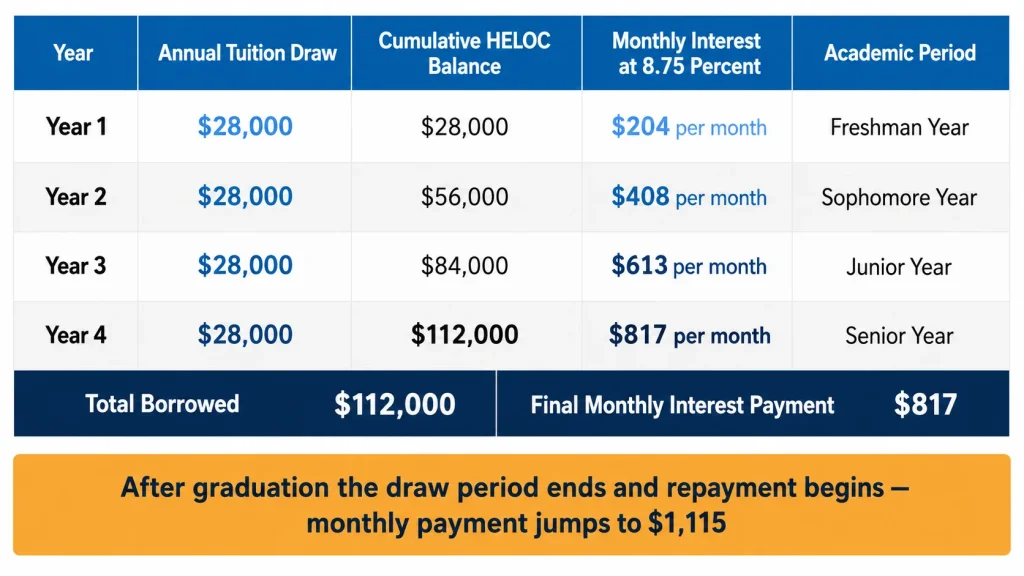

The mechanics are straightforward. You open a HELOC secured by your home equity, draw funds each semester or academic year as tuition bills arrive, and make interest-only minimum payments during the draw period while your child is in school.

This matches the tuition billing cycle well. Rather than borrowing the full four-year cost upfront, you draw in stages — year one tuition in fall, spring costs in spring, year two in the following fall. You pay interest only on what you have drawn, not on the entire projected four-year cost.

Example: Four-year public university at $28,000/year

| Year | Annual Tuition Draw | Cumulative HELOC Balance | Monthly Interest (8.75%) |

|---|---|---|---|

| Year 1 | $28,000 | $28,000 | $204 |

| Year 2 | $28,000 | $56,000 | $408 |

| Year 3 | $28,000 | $84,000 | $613 |

| Year 4 | $28,000 | $112,000 | $817 |

By graduation, the HELOC balance is $112,000 with a monthly interest-only payment of $817. After the draw period ends, the repayment period begins — and on a 15-year term at 8.75%, the monthly payment jumps to approximately $1,115.

That is the baseline. Everything else in this analysis builds on these numbers.

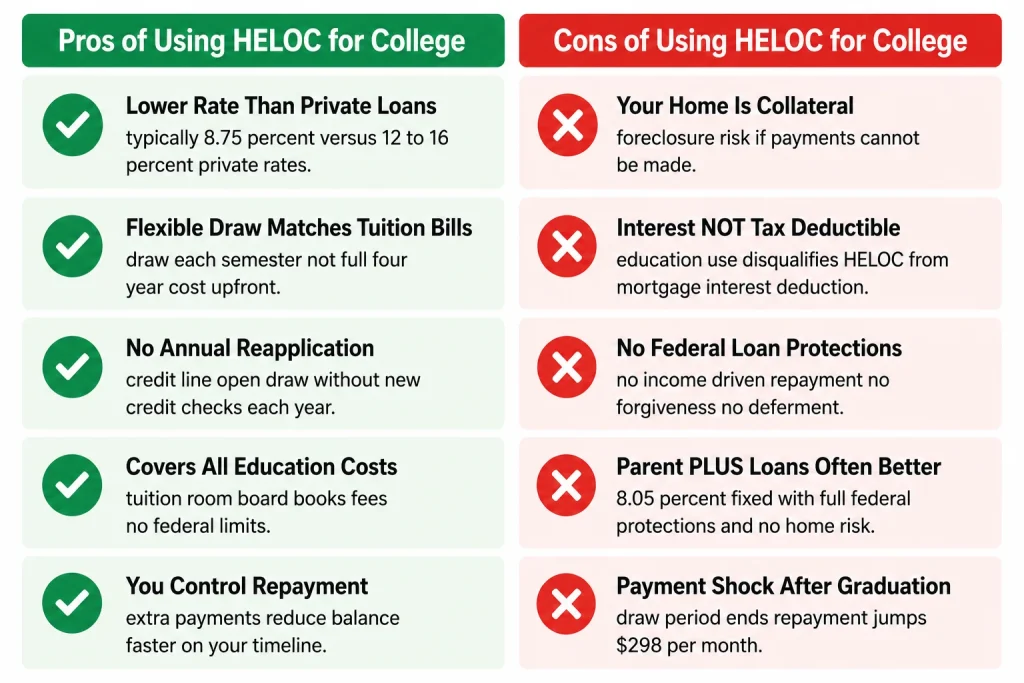

The Pros: Where a HELOC Genuinely Helps

Lower Interest Rate Than Private Student Loans

This is the most compelling argument for the HELOC approach. Private student loan interest rates in 2026 range from approximately 8.5% to 16.99% depending on the lender, the borrower’s credit, and whether a cosigner is involved. For families with less-than-excellent credit, private student loan rates can push toward 14%–16%.

A HELOC at 8.75% for a family with good credit is cheaper than most private student loan options — sometimes by 5 to 8 percentage points. On a $112,000 balance over 15 years, a 6-point rate difference saves approximately $58,000 in total interest.

Flexible Draw Timing Matches Tuition Bills

College costs arrive in predictable installments — fall semester, spring semester, year after year. A HELOC’s draw-as-needed structure matches this perfectly. You are not borrowing four years of tuition upfront and paying interest on the full amount while your child is still in freshman year.

This staged drawing reduces your interest cost during the college years significantly compared to taking a lump-sum loan for the full estimated cost.

No Application Required Each Year

Once the HELOC is open, you draw each year without reapplying. There are no annual credit checks, no new loan origination fees, and no waiting for approval each September. The credit line is there when you need it.

This is meaningfully more convenient than applying for new private student loans each academic year — a process that requires credit checks, cosigner agreements, and new documentation every time.

Can Cover All Education-Related Costs

Federal student loans have annual and lifetime limits. A dependent undergraduate student can borrow a maximum of $27,000 total in federal Direct Loans over four years — not enough to cover four years at most universities. A HELOC has no education-specific limits — it can cover tuition, room, board, books, fees, and any other education-related expense up to your credit limit.

You Control the Repayment Structure

Unlike student loans — which have specific repayment plans, deferment options, and servicer requirements — a HELOC gives you direct control over how aggressively you repay. If your income allows extra principal payments during or after the college years, you can reduce the balance quickly. If cash flow is tight, the interest-only minimum keeps obligations manageable.

The Cons: Serious Risks That Demand Honest Consideration

Your Home Is the Collateral — Not Your Child’s Future Income

This is the most important difference between using a HELOC and using student loans for college.

Federal and private student loans are the student’s debt — or the parent’s, in the case of Parent PLUS Loans — but they are unsecured. If repayment becomes impossible due to income disruption, disability, or other hardship, there are remedies: income-driven repayment plans, deferment, forbearance, and in some cases forgiveness programs.

A HELOC is secured by your home. If you cannot repay, your lender can foreclose. You are betting your primary residence on your child’s education — and on your own ability to service that debt for 15+ years after the draw period ends.

This is not a reason to automatically say no. It is a reason to make the decision with full awareness of what is at stake.

HELOC Interest on Education Expenses Is NOT Tax Deductible

This is one of the most significant financial disadvantages of using a HELOC for college — and one that most families do not realize until after the fact.

Under current IRS rules, HELOC interest is deductible only when funds are used to buy, build, or substantially improve the home securing the loan. Education expenses are explicitly non-qualifying. There is no exception for tuition, books, or room and board.

Compare this to federal student loan interest — which is deductible up to $2,500 per year for borrowers below the income phase-out threshold ($80,000 single / $165,000 joint in 2026). The student loan interest deduction is available without itemizing, making it accessible to far more families than the mortgage interest deduction.

Federal student loans also carry interest that stops accruing during periods of authorized deferment or forbearance — another tax-adjacent benefit a HELOC cannot provide.

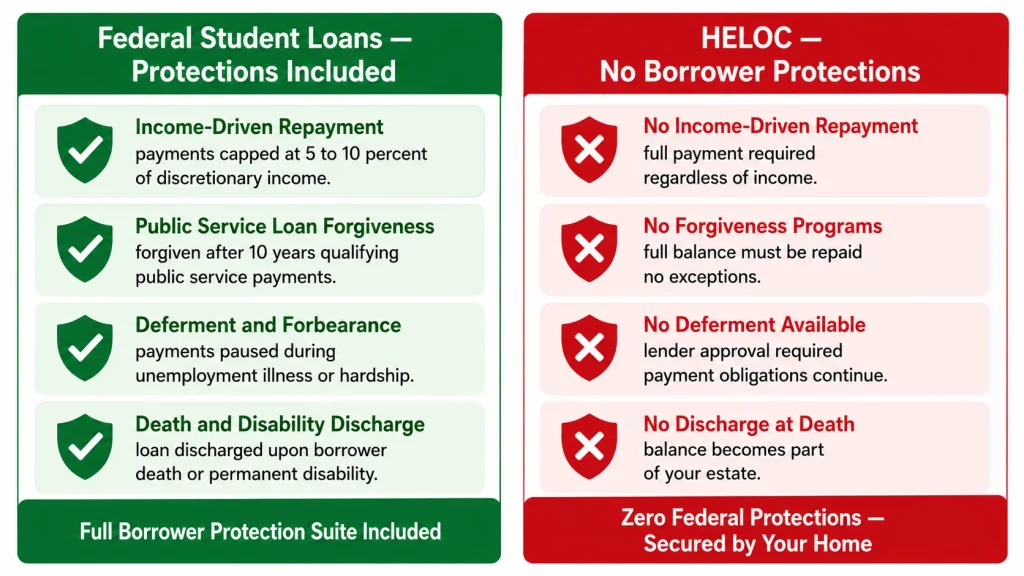

Federal Student Loans Have Protections a HELOC Does Not

Federal Direct Loans come with a suite of borrower protections that simply do not exist for HELOC debt:

Income-driven repayment (IDR): Monthly payments capped at 5–10% of discretionary income. If your graduate earns less than expected, payments adjust automatically.

Public Service Loan Forgiveness (PSLF): Federal loans can be forgiven after 10 years of qualifying payments for borrowers in public service careers — government, nonprofits, education, healthcare. A HELOC provides no forgiveness of any kind.

Deferment and forbearance: Payments can be temporarily paused during unemployment, illness, or financial hardship. HELOC payments cannot be paused without lender approval and potential credit consequences.

Death and disability discharge: Federal student loans are discharged upon the borrower’s death or permanent disability. A HELOC balance becomes part of your estate.

These protections have real monetary value — particularly for families whose student will enter lower-paying careers, public service, or face uncertain post-graduation income.

Parent PLUS Loans May Be More Appropriate Than a HELOC

Many families immediately compare a HELOC to private student loans — where the HELOC often wins on rate. But the more relevant comparison for most families is a HELOC versus a Parent PLUS Loan.

Parent PLUS Loans are federal Direct Loans available to parents of dependent undergraduate students. In 2026, the Parent PLUS rate is 8.05% fixed — comparable to or slightly below many HELOC rates. They come with all federal loan protections, income-driven repayment options (via consolidation), and no home collateral requirement.

For many families, Parent PLUS Loans are strictly better than a HELOC for college funding — similar rate, federal protections, no home at risk. Always exhaust Parent PLUS Loan eligibility before drawing a HELOC for education expenses.

Payment Shock Hits When Your Financial Flexibility May Already Be Stretched

The HELOC draw period for a four-year college funding strategy ends 5 to 10 years after you opened the line — which may coincide with approaching retirement, your child potentially returning home post-graduation, or other financial demands.

On a $112,000 balance at 8.75% entering a 15-year repayment period, the monthly payment jumps from $817 (interest only) to approximately $1,115 (fully amortized) — a $298/month increase. If this transition happens as you are entering peak earning years with other financial goals, it is manageable. If it arrives as you are transitioning to retirement income, it can be genuinely difficult.

The Complete Cost Comparison: HELOC vs. Federal vs. Private

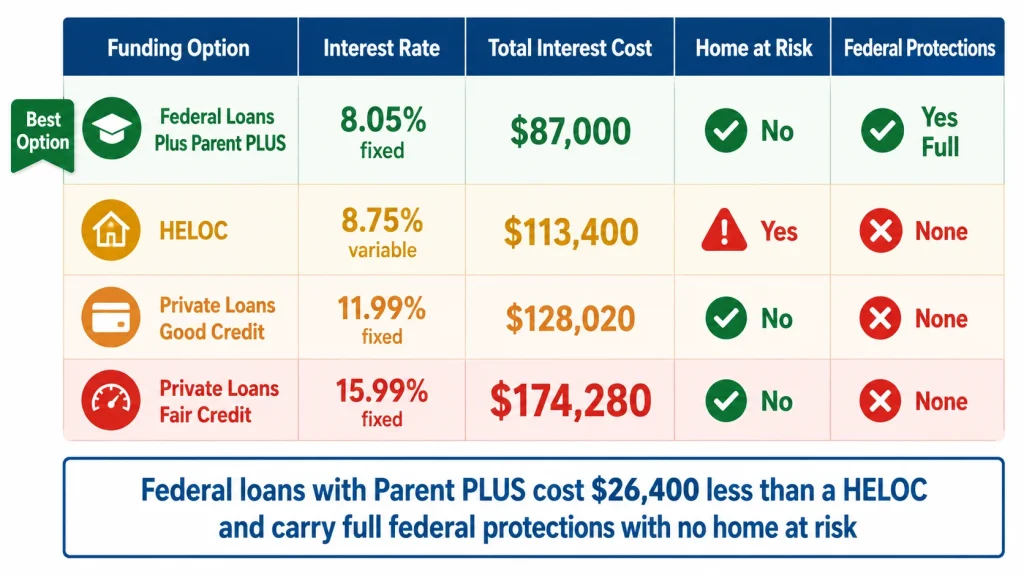

Let us run the full cost comparison for funding a $112,000 four-year education.

Option 1: HELOC at 8.75% Variable

- Draw period payments (4 years): $204 → $817/month, approximately $24,700 total interest during school

- Repayment period (15 years at 8.75%): $1,115/month

- Repayment interest: $88,700

- Total interest over full term: $113,400

- Tax deductibility: None

- Home at risk: Yes

Option 2: Federal Direct Loans + Parent PLUS at 8.05% Fixed

- Student borrows maximum federal ($27,000 over 4 years)

- Parent PLUS covers remaining $85,000 at 8.05%

- Student loan interest during school: ~$5,400

- Parent PLUS interest during school: ~$17,000

- Combined repayment (10-year standard): approximately $1,100/month

- Total interest over full term: ~$87,000

- Student loan interest deduction: Up to $2,500/year for the student

- Home at risk: No

- Federal protections: Full

Option 3: Private Student Loans at 11.99% (Good Credit)

- Borrowing $112,000 at 11.99% over 15 years

- Monthly payment: $1,339

- Total interest: $128,020

- Tax deductibility: $2,500/year for qualifying borrowers

- Home at risk: No

Option 4: Private Student Loans at 15.99% (Fair Credit)

- Borrowing $112,000 at 15.99% over 15 years

- Monthly payment: $1,596

- Total interest: $174,280

- Tax deductibility: Limited

- Home at risk: No

Cost Summary:

| Option | Rate | Total Interest | Home at Risk | Federal Protections |

|---|---|---|---|---|

| Federal loans + Parent PLUS | 8.05% fixed | ~$87,000 | No | Yes — full |

| HELOC | 8.75% variable | ~$113,400 | Yes | None |

| Private loans (good credit) | 11.99% fixed | ~$128,020 | No | None |

| Private loans (fair credit) | 15.99% fixed | ~$174,280 | No | None |

The comparison is clear: federal loans with Parent PLUS are the cheapest option at the most favorable rate, with full protections and no home collateral. The HELOC is second on cost but first on risk. Private loans at good credit are comparable to HELOC cost but without home risk. Private loans at fair credit are dramatically more expensive than everything else.

When Does a HELOC for College Actually Make Sense?

Given the federal loan comparison, a HELOC for college funding makes sense in a narrower set of circumstances than most families initially assume.

When federal aid and loans are maxed out and costs remain unpaid. If your student has exhausted federal Direct Loan limits, Parent PLUS is not available to you due to adverse credit history, and private loan rates are significantly higher than your HELOC rate — a HELOC bridges the gap at a lower cost than available alternatives.

When the family’s credit does not qualify for favorable private loan rates. A family with a credit score of 650 faces private student loan rates of 16%–20%. Their HELOC at 9.5% (fair credit HELOC rate) is still significantly cheaper — despite the home collateral risk.

When the education investment has a clear, high-probability return. Medical school, dental school, law school, engineering programs at well-ranked institutions — degrees with strong, predictable return on investment where the graduate’s earning potential is likely to far exceed the debt cost. The home collateral risk is more manageable when the graduate’s income can help service the debt.

When the family has significant equity and strong financial stability. A family with $400,000 in home equity using a $90,000 HELOC for college is in a fundamentally different risk position than a family with $50,000 in equity stretching to cover the same amount.

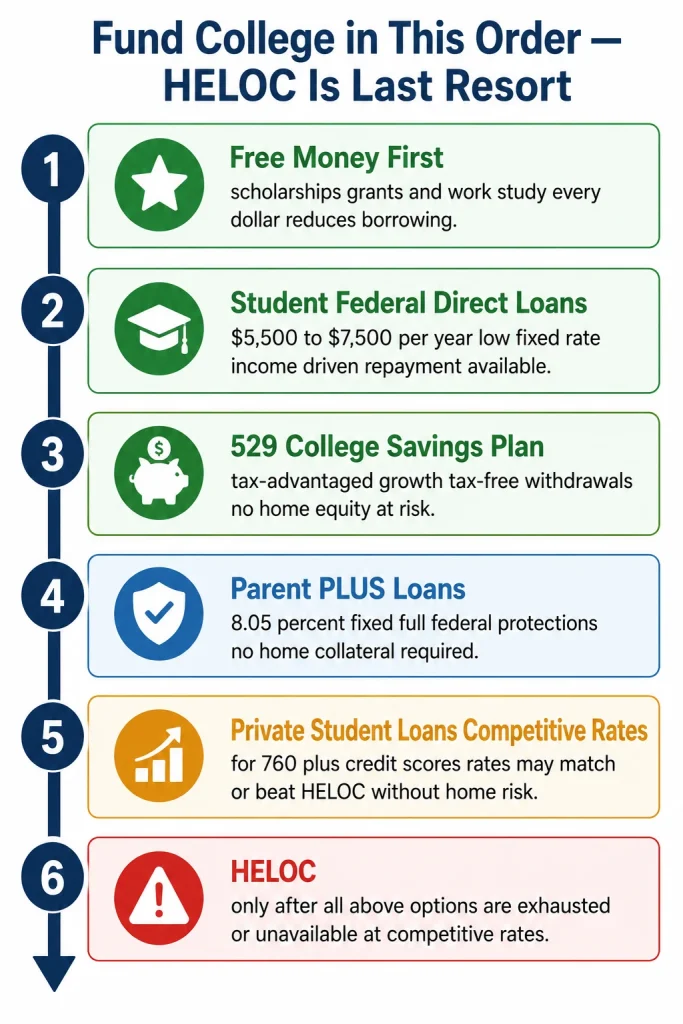

The Right Order: Exhaust These Options Before the HELOC

Before drawing a HELOC for college, work through this priority sequence:

- Free money first: Scholarships, grants, work-study. Every dollar of free money reduces the amount you need to borrow.

- Student’s federal Direct Loans: $5,500 freshman year, scaling up to $7,500 senior year for dependent students. Low fixed rates, income-driven repayment available.

- 529 college savings plan: If you have one, use it. Tax-advantaged growth, tax-free withdrawals for qualifying education expenses, no impact on your home.

- Parent PLUS Loans: 8.05% fixed in 2026, federal protections, no home collateral. Apply before considering a HELOC.

- Private student loans at competitive rates: For borrowers with excellent credit (760+), some private lenders offer rates of 7.99%–9.99% — comparable to or better than a HELOC with no home collateral.

- HELOC: Only after the above options are exhausted or unavailable at competitive rates.

A Word on FAFSA and Home Equity

One practical consideration families often overlook: home equity does not directly factor into the federal financial aid formula for most families. The FAFSA (Free Application for Federal Student Aid) does not count primary home equity as a reportable asset for most applicants.

However, taking a HELOC draw and keeping those funds in a bank account converts home equity (not counted) to cash savings (counted as an asset in the FAFSA calculation). This can reduce your student’s Expected Family Contribution (EFC) or Student Aid Index (SAI) and reduce their financial aid eligibility.

If your student is still in the financial aid calculation years, consult a financial aid advisor before drawing HELOC funds — the timing of draws relative to FAFSA filing dates can affect aid eligibility.

The Bottom Line

A HELOC can be a viable tool for college funding in specific circumstances — particularly when federal aid is exhausted and private loan alternatives are significantly more expensive. The staged draw structure matches tuition billing cycles, the rate is often competitive, and the credit line can cover costs that federal limits cannot.

But the risks are real and the trade-offs are significant. Your home is collateral. The interest is not tax deductible. Federal student loans with their income-driven repayment, forgiveness options, and borrower protections are almost always preferable to a HELOC when they are available at competitive rates.

The right answer for most families: exhaust federal aid, scholarships, and Parent PLUS Loans first. Use a HELOC only for the gap that remains — and only after honestly assessing whether the monthly repayment obligation, including the payment shock at the end of the draw period, is sustainable within your long-term financial plan.

Use our HELOC Payment Calculator to model what a HELOC draw would cost you semester by semester as the balance builds — and what the full repayment payment will look like when the draw period ends.